🤝 The Mega Merger: HDFC Twins

India's biggest housing finance company and its biggest private sector bank are joining hands. Here's why everyone is so excited about this merger.

The holy union of HDFC Bank and its parent HDFC Ltd is making headlines. Investors are going gaga.

But why is this merger such a big deal?

ReadOn to find out!

The Nitty Gritties

Before we get into the why of the merger, let's take a look at the details.

The merger is a $40bn deal between HDFC Ltd, a housing finance company, and HDFC Bank, India's largest private sector bank.

After they merge, their combined net worth will be $185bn.

Investors will get 42 shares of HDFC Bank for every 25 shares of HDFC Ltd.

Since the bank is absorbing its parent, HDFC Ltd.'s 25.8% stake in the company will be dissolved.

Now that the details are clear, let's come to why the two entities are merging.

The Reasons

The first and the simplest reason: The merged entity will have a balance sheet of Rs. 17.87 lakh crores.

This large balance sheet is the need of the hour right now. Why?

Because India is going to see a massive increase in infrastructure spending as the government wants to revamp our old and broken infrastructure. Plus, the demand for retail loans and housing loans is also rising and is set to continue rising as the economy is now slowly opening up.

The bigger balance sheet will help HDFC Bank meet this demand and prevent customers from slipping away to competitors.

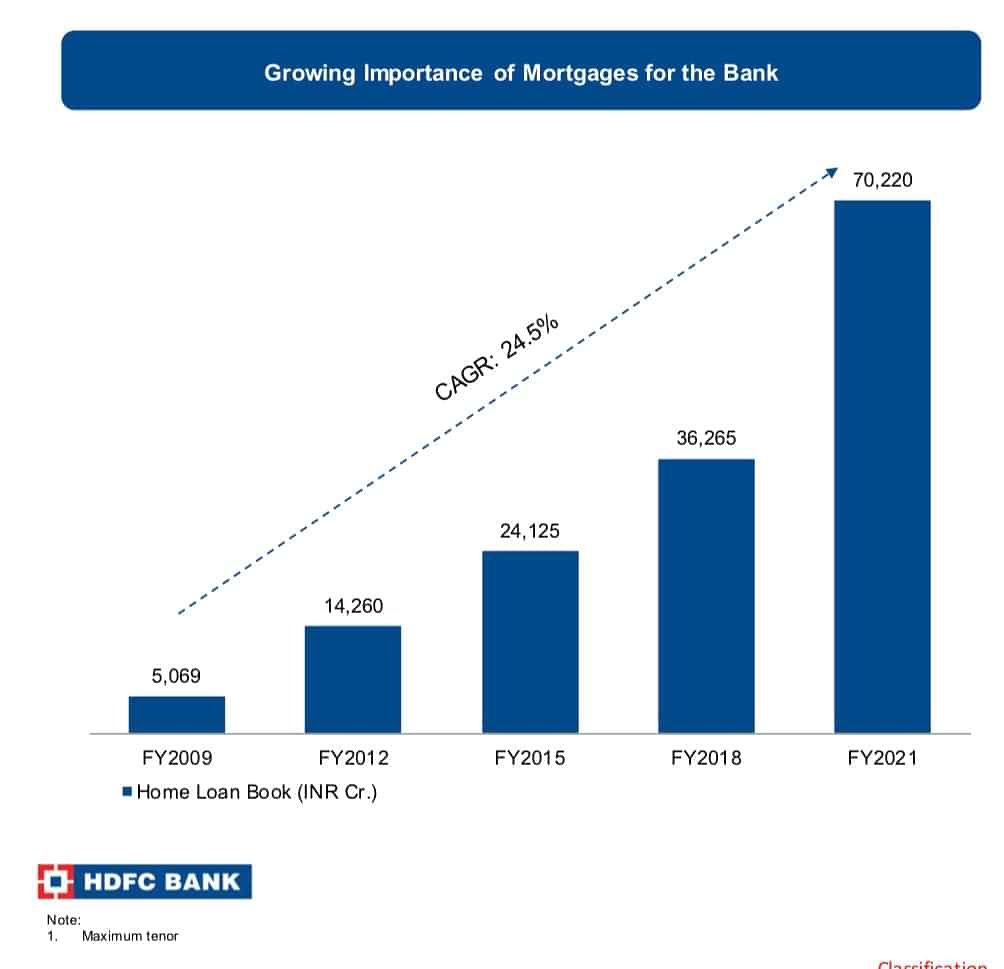

Plus, HDFC Ltd's home loan customers do not stick around for their entire lifetime. As soon as they pay off their loans, they no longer have any business to conduct with HDFC Ltd. But if the two companies merge, these customers could be persuaded to create a bank account with HDFC for ease of operation, converting temporary customers into full-time customers.

Moreover, the merger will put the company much ahead of its competitors without wasting much time, effort or money. The merged entity will be twice the size of ICICI bank, which is the third-largest bank in India after HDFC Bank. Its market share will also increase to 15% from 11%.

And the biggest benefit is that the merged entity will be able to get funding for cheaper.

You see, HDFC Ltd. is a non-banking finance company. So, basically, it only deals with loans and not savings accounts and fixed deposits like banks.

To get the money to give others a loan, it has to first borrow from banks.

So, where banks can get funds for 5%-6% (they have to pay the interest rate on savings accounts and FDs), they give this money to NBFCs at a higher interest rate.

Therefore, the cost of raising money for NBFCs is much higher depending on the interest rates that banks give them (usually around 7.5%).

In times of crisis, like when NBFCs like IL&FS failed, the interest amount for NBFCs went up to 9%!

So, borrowing costs for the merged entity will now go down.

And there could not be a better time for this merger. So far, even though NBFCs had higher borrowing costs, they chose not to merge with banks or even become banks because they got preferential treatment from the RBI.

Yeah, the RBI had much more lenient rules for NBFCs than it did for banks.

However, after a lot of NBFC-related financial debacles, the RBI is now finally getting stricter with them (you can read about this in detail here and here).

So HDFC decided to cash in on the benefits of becoming a bank.

However, the merger still needs to get approval from several regulators, a process that will take 12-18 months.

What’s interesting is that HDFC's large balance sheet could also haunt competitors, forcing them to merge in order to better compete with this giant.

Advantages to the Economy

This will benefit our economy hugely. Right now, we don't have any banks that can match giants like JP Morgan (balance sheet = $3.8 trillion).

And the smaller banks that we do have often struggle for survival and even collapse due to loan defaults.

If we do have some large banks, they could extend more credit to our credit-starved economy.

Plus, with a larger balance sheet, these banks will have to give more loans to the agriculture sector and for affordable housing solutions.

Umm, why?

Because these sectors come under priority sector lending. Banks have to lend 40% of their adjusted net bank credit to these priority sectors to ensure their growth.

So, you see. The merger is a win-win for everyone.

Do you think we will be seeing more mergers in this sector?

Share this with your friends via WhatsApp or Twitter and help them declutter news from noise! See you tomorrow :)

You can also listen to our stories because the Revolution ReadOn podcast is live!! Here: you can catch it on Spotify, Apple Podcast or Amazon Music, Google Podcasts, Gaana and Jio Saavn.

If you are coming here for the very first time: Don’t forget to join us on WhatsApp to get daily updates! 👇