🏦 RBI getting Stricter with NBFCs?

🏦 RBI getting Stricter with NBFCs?

RBI is imposing rules on NBFCs. Again. What's going on?

If you're an elder sibling you'll definitely remember having endured stricter rules than your younger siblings. Don’t you think the younger siblings always get away with everything?

So far, this has also been the scenario in our banking environment. While the RBI was strict with banks, it was very lenient with the newer non-banking financial companies (NBFCs). But that's all in the past now. RBI has now decided to be a fair parent. It's formulating stricter rules for the mischievous NBFCs.

The NBFC Problem

Just two months back the RBI had introduced a framework to better regulate NBFCs. And now it has issued a new prompt corrective action (PCA) framework for them.

But why so many regulations?

Because NBFCs have suddenly gained a lot of importance. They offer housing loans, microloans and other services to customers and some even take money deposits. So, in essence, they work sort of like banks but without a banking licence.

This is exactly why they have been operating under the RBI's nose since 1964. But so far the RBI didn't think of regulating them so strictly because they simply weren't that big. It wasn't worth it to call meetings and draft rules to regulate these tiny institutions.

But things have changed. Over the last few years, banks got wary about whom to lend money and whom not to, fearing a rise in loan defaults. This coupled with RBI's lax regulations for NBFCs created a recipe for disaster.

More and more people flocked to NBFCs to get loans, causing the sector to grow super fast. From holding just 12% of the assets that banks held in 2010, they are now over 25% of the size of banks. The sector has also been growing thanks to a flood of new fintech firms offering credit cards and buy-now-pay-later services. These fintechs also come under the NBFC banner.

Okay, but why were these NBFCs giving money to those whom the banks had refused?

Simple, they were charging a higher rate of interest. They thought that this higher rate of interest would cushion them in case a few defaulted.

They took a calculated risk, but their maths was way off. Too many people defaulted and major NBFCs went under. This caused a chain reaction that ultimately impacted the entire economy.

To lend money these NBFCs had borrowed from several banks (yes, banks lend money to NBFCs!) and other institutions and now they couldn't afford to pay them back. For instance, Infrastructure Leasing & Financial Services (IL&FS), the first major NBFC to default, owed 94,000 crores to its debtors.

So, lenders faced a massive liquidity crunch and their faith in NBFCs eroded and the whole economy suffered due to this interconnectedness between banks and NBFCs.

That's when the RBI decided to step in.

Stricter Rules of NBFCs

The new framework for NBFCs is similar to the one launched for banks in 2002. It will make it easy for the RBI to determine when an NBFC is at risk and take prompt action to stop its condition from getting worse.

The framework launched in October (you can read about it here) was a preventative measure aimed at stopping NBFCs from getting in trouble. But what about the ones who actually get into trouble? For them, it has introduced a set of corrective actions. It will help RBI understand when NBFCs have gotten into trouble and correct the problem before it gets out of hand.

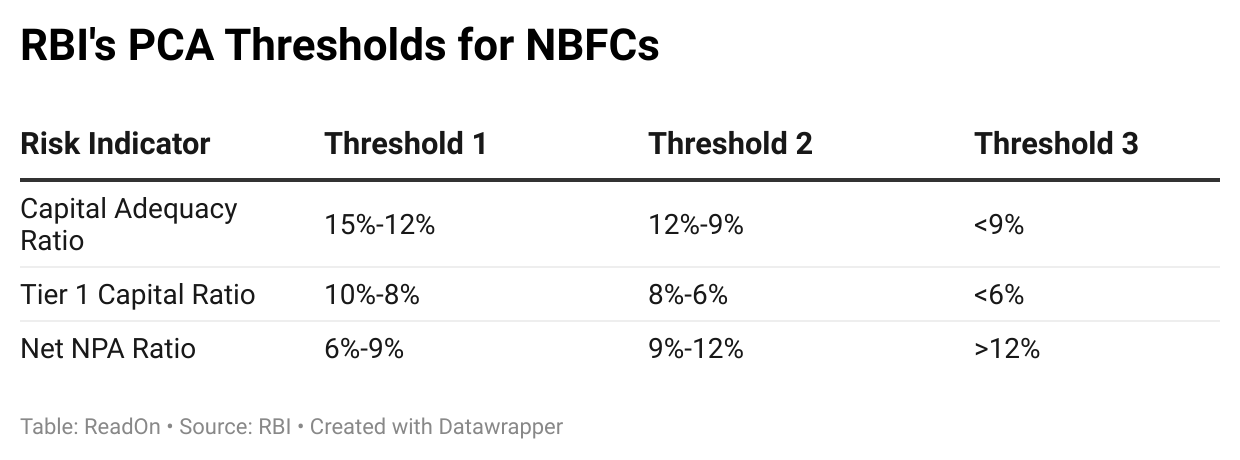

The RBI has determined different levels of risk for NBFCs and the corresponding action it will take when an NBFC crosses that risk level.

Here's a chart highlighting what the thresholds and the risk factors are:

For instance, if an NBFC reaches the first threshold then its dividend distributions will be restricted. Plus, its promoters will be asked to add new capital and reduce leverage (or risk).

When it hits threshold 2, it will be stopped from opening new branches and if it hits the final level then RBI will not allow any other expenditure other than that needed for a technological upgrade.

These new rules, which will come into force from October 2022, will only be applicable for NBFCs that take public deposits and which have an asset size of over 1,000 crores.

To meet these new restrictions, NBFCs will have to get much stricter with loans. They will no longer be able to give out loans however they please because if their non-performing assets (bad debts) cross the thresholds set by RBI their operations will be impacted. So, what will happen to people with bad credit? Where will they go for loans now?

Many of these people may now have to resort to taking loans from loan sharks or fake loan apps. This may lead to further problems.

So, are RBI's new rules justified? Or are they just restricting NBFCs?

P.S. You can read more about the RBI's NBFC framework here and here.

Share this with your friends via WhatsApp or Twitter and help them declutter news from noise! See you tomorrow :)

If you are coming here for the very first time: Don’t forget to join us on WhatsApp to get daily updates! 👇

Till 999 crORes ENJOY...

Many of these people may now have to resort to taking loans from loan sharks or fake loan apps. This may lead to further problems.

ending with this conclusion was not good, it is making this whole approach of RBI is wrong, but the reality is the steps taken by RBI is really appreciable.