🏛 The Evolution: Fintech Regulations

🏛 The Evolution: Fintech Regulations

The FinTech sector has caused major upheaval in the world. And the government is ready to do some damage control.

We are living in a world where anything and everything is just a click away. From standing in huge queues at the bank or at the insurance office, we have definitely come a long long way

How did this change happen? Through FinTech, of course.

But with great power comes great responsibility.

And FinTechs have all the power, but little responsibility.

The Growth of FinTech

FinTech has leveraged technology to make everything money super easy and convenient. Starting from banking, insurance, trading, and personal finance management, this sector has now grown to include neobanks, buy now pay later services and a lot more.

The market cap of India's FinTech sector right now is $31 billion and it is expected to grow to a whopping $84 billion by 2025. In fact, India is one of the fastest growing FinTech markets in the world.

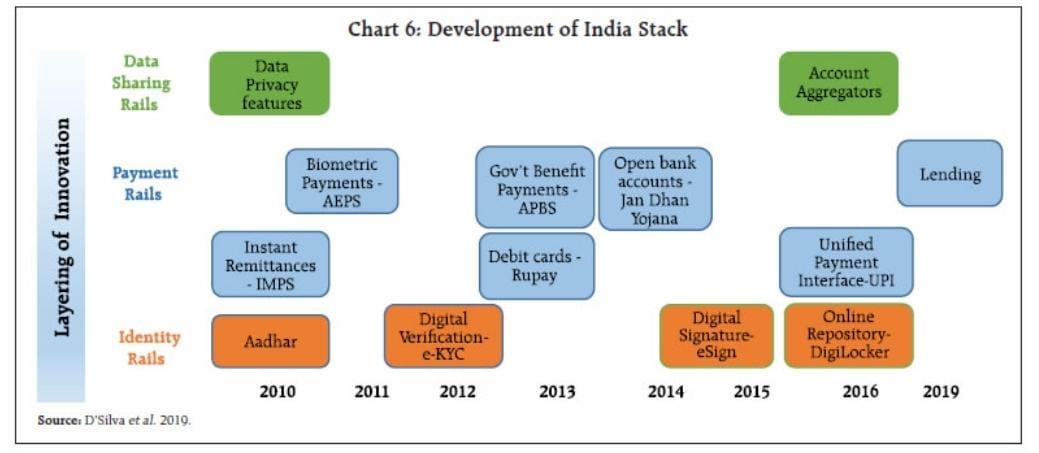

This growth has been fuelled by cheap internet rates, smartphones and demonetisation. But it has only been made possible because of IndiaStack, a unified platform that was built to make paper-less, cash-less, and presence-less transactions easier. (You can read more about this groundbreaking innovation here).

Everything looks fine, until you realize that this sector is majorly unregulated.

The Need For Regulation

You see, the government has rules and regulations for banks, insurance agents and all the entities that have a physical presence.

Now when things started moving to the digital world, regulations started becoming haywire. How would the government now regulate these new breeds of companies?

But before we go there, why is regulation even needed?

Because, unregulated companies pose a lot of risk to the consumers, to the community, and sometimes the entire economy.

So, the RBI, SEBI, and other government organizations are constantly monitoring, reviewing, and updating old rules to make sure we're not impacted by the actions of some bad players.

And so in 2007, the Payment and Settlement Systems Act was passed. This is the main law that governs payments regulation in India. It states that no payment system can be initiated in India without the RBI's approval.

Soon laws related to P2P lending, NBFCs and other sectors started cropping up.

But the FinTech sector has kept growing and evolving faster than the government could keep up. Many sectors are still unregulated. There are no rules governing digital loan apps or buy-now-pay-later schemes.

However, a change is coming.

After many people fell prey to loan sharks on loan apps, the government decided to create new regulations for the loan app sector as well. It has created a working group that firmly believes that "What is not legal in the physical world cannot be considered legal only because it is happening online."

This recommendation, which could soon become a law, will impact buy-now-pay-later (BNPL) companies. These companies are all the rage right now as they allow you to buy things that you can't currently afford. (You can check out the BNPL business model over here).

Technically, what these companies are doing is offering you loans. But they are unregulated. So, with the new laws they may no longer be able to do so. Not without getting an RBI registration.

This will allow the RBI to keep an eye on them and ensure that they don't snare innocent people in their traps.

Do you think regulating the FinTech sector will help the people? Or is the government just stifling innovation?

Share this via WhatsApp or Twitter with your friends and help them declutter news from noise! See you tomorrow :)

If you are coming here for the very first time: Don’t forget to join us on WhatsApp to get daily updates! 👇