🤔 Indian Banks Going to the Moon?

🤔 Indian Banks Going to the Moon?

Banks are having a field day. But how long can the good times continue?

Banks are currently having a field day, or rather a field month!

Most banks have registered phenomenal profits in Q3 of 2021 and are now witnessing a rally in their share prices.

But what has caused this growth and will it continue?

Let's take a closer look.

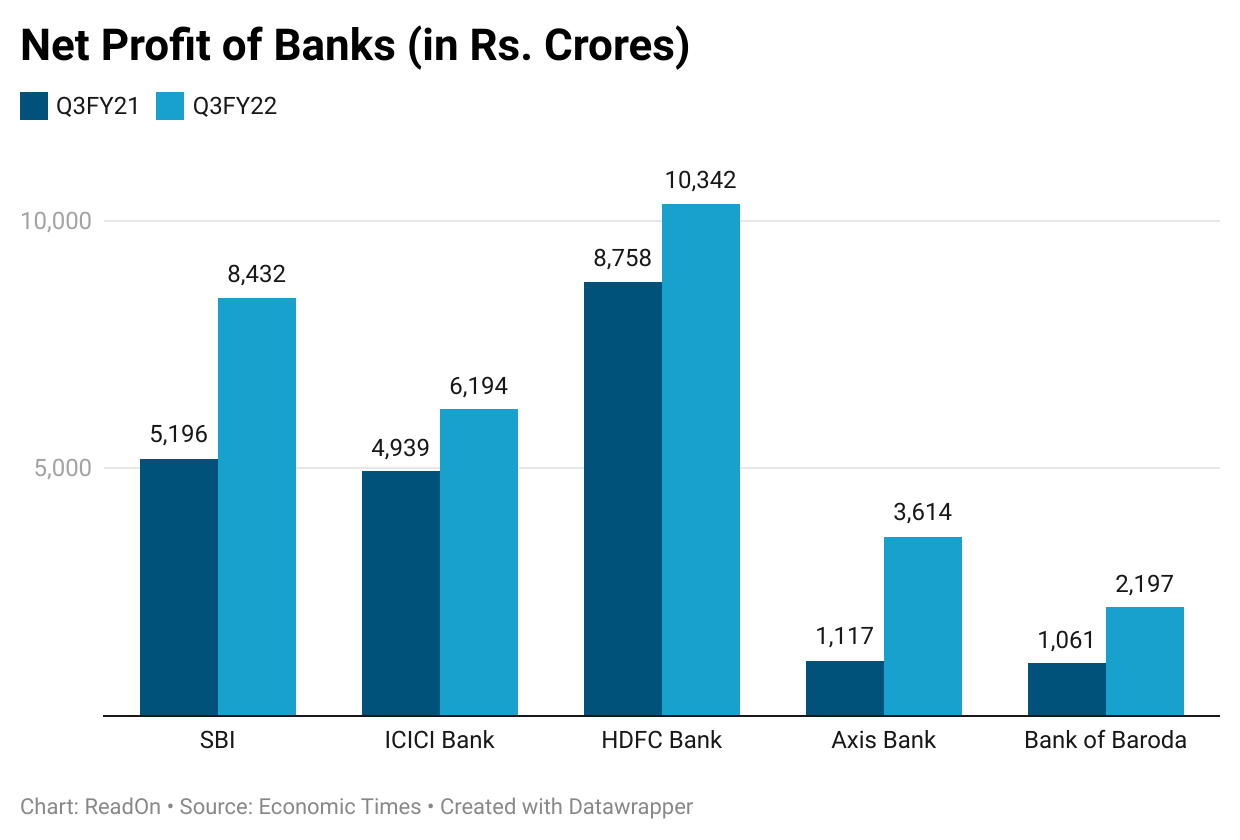

Bank Earnings Call

Several banks, both public and private, have managed to make double-digit growth in profits this year.

But we're focusing specifically on one of India's most trusted and the most meme-worthy banks today as it recently posted its earnings report: The State Bank of India.

And trust us, its numbers are no joke.

The bank saw a profit of Rs. 8,431.9 crores, which is a 62% increase from last year. Not only is this way above experts' estimates, it is also the bank's highest-ever profit on record. This caused the bank's shares to reach their 52-week high when the results were announced.

The real question however is how did SBI go about recording the highest-ever profit?

Because of an increase in demand for loans: which grew by 8.5%.

Plus, deposits have also increased by 8.83% from last year probably because people are no longer hoarding their wealth at home due to fear of Covid.

A decline in non-performing assets has also helped the bank a lot. It's gross NPA ratio declined slightly from 4.77% to 4.5%.

But this could be due to the RBI's moratorium (an option for the borrowers to defer the payment of a loan for a specified period) on loan payments. You see, because of the financial difficulties brought on by Covid, the RBI had asked many banks to restructure loan payments, allowing lenders to delay many loan payments till December 31, 2021.

Now lower NPAs are not the only reason for high share prices. SBI has decided to sell off NPAs worth Rs. 406 crores to asset recovering companies or NBFCs who are interested in recovering these loans from the lenders.

It has also restructured loans worth Rs. 32,895 crores, which account for 1.2% of its loan book. This means that the bank has renegotiated terms of loans that could potentially become bad debts. These loans will now be payable in the later quarters. This could also explain a decline in its NPA ratios.

Despite all the restructuring, provisions against bad loans increased to ₹3,096 crores, up 35% from last year.

But the bank claims it is well protected against risks. However, this may not be entirely true.

The Future of the Banking Sector

The bank's performance in the upcoming quarter depends on a lot of ifs and buts.

The first major roadblock in the bank's continued success next quarter is its own balance sheet. You see, the bank has restructured a massive loan amount. It hopes that by delaying the loan repayment date, it will be able to stop these loans from turning into non-performing assets.

And SBI is not the only bank to follow this strategy. Several banks have restructured major loan amounts under the RBI's Covid resolution framework. For instance, ICICI Bank has restructured Rs. 9,684 crores worth of loans.

So, their performance in the upcoming quarters will depend majorly on the performance of these restructured loans. If the banks are able to recover them then the party continues. If not, they're in for a disaster.

And this is not the only unknown factor that will impact banks' performance.

The RBI is considering raising interest rates to control inflation. This could decrease the growth in loans that has helped the banks perform so well this quarter.

Plus, this could also push more people to invest in government bonds, decreasing the amount deposited in bank accounts and fixed deposits.

But it's not all doom and despair for SBI and the banking sector.

On the plus side, the bank is set to get a lot more business from major companies as the government has decided to boost infrastructure development.

Also, with the formation of a "bad bank", many banks including SBI will be able to minimise losses from non-performing assets, as the bad bank will buy these NPAs from them.

So, you see the future of the banking sector is kind of up in the air right now. But still, a lot could go wrong.

Tell us what you think the future holds for this sector.

It’s time to begin the journey of creating long-term wealth! Become a ReadOn Club Member to discuss high growth potential startups, crypto projects and stocks with other finance enthusiasts. And so much more! Check it out 👇🏻

Share this with your friends via WhatsApp or Twitter and help them become financially smarter! See you tomorrow :)

You can also listen to our stories because the Revolution ReadOn podcast is live!! Here: you can catch it on Spotify, Apple Podcast or Amazon Music, Google Podcasts, Gaana and Jio Saavn.

If you are coming here for the very first time: Don’t forget to join us on WhatsApp to get daily updates! 👇