Will Markets Fall in November?

How will changing interest rates in the US affect the Indian markets?

Isn’t it strange how announcements in the US can impact the Indian markets? One small change in policy snowballs into a mad rush of money movements across borders.

Yet again, the Fed (the US counterpart of RBI) has signalled that it will be tweaking its strategy. Wondering how it will impact the market?

Read on.

The story begins with Covid (yeah, it’s been the root cause of everything for the past 1 year). The modern world had not seen a crisis of this scale before and it threatened the entire fabric of the economy. Something had to be done, to save things from falling apart.

So, the Fed started cutting interest rates, printing money and injecting more liquidity in the market. Here’s how the interest rates fell over the last one and a half years:

But how was this move supposed to help?

It was an incentive for businesses to take loans and keep going even during the tough times. This way, the Fed ensured a steady supply of goods and services in the economy. At the same time, it also ensured that consumption demand does not nosedive.

How, you ask?

By printing more money and using it to buy more and more government bonds (giving more and more loans to the government). The government would then deploy these loans to build assets or fund welfare programs. This put money right in the hands of people. And what do people do with more money?

They spend. And so the wheel of the US economy could move effortlessly during the Covid crisis.

Now, what does this have to do with the Indian economy?

While the lower interest rates is a boon for borrowers in the US, it isn’t so great for the investors. So in the search for better investment opportunities, these investors look to invest elsewhere (emerging economies like India, China, Brazil, etc).

And, this is where India comes into the picture.

Yeah, low interest rates in the US is a boon for the Indian markets. But if the interest rate goes up, US investors won’t have any incentive to look elsewhere. And the money will move out.

But then why is the Fed deciding to increase the rates? If everyone is happy, shouldn’t we continue like this forever?

If only we could. If the interest rates continue to be low and the free cash floating around the market continues to be high, it can soon spiral into a lot of problems. Here’s how:

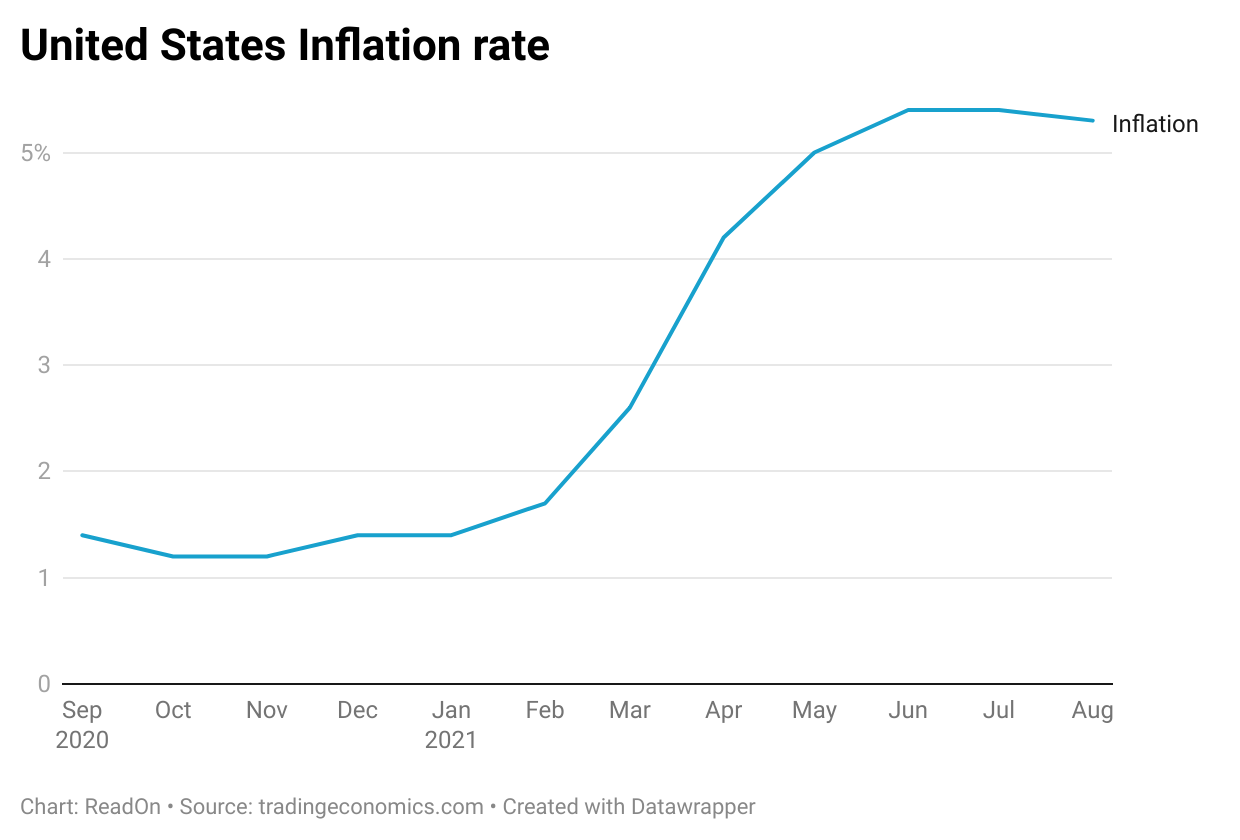

With more money at the disposal of people, their demands will also go up. But the supply of goods and services will take some time to catch up. More money chasing a lesser number of goods and services will lead to inflation.

Businesses growing at a break-neck pace will also be demanding more labor and inputs. But the supply of resources will be constrained. Again, more money chasing fewer resources will push inflation further up. Now, the economy will have more money, but that money won’t have any extra value.

That’s exactly what has happened in the U.S.

The inflation is way above the 2% target set by the Central Bank. So to rein in this inflation, the Fed has indicated that they will reduce the purchase of bonds and increase the rate of interest from November 2021. This move is called ‘tapering’.

It will be bad for India, right?

Maybe. You see, this tapering is not happening for the very first time. It has happened in the past as well.

The US economy found itself in a unique situation in 2008. Several major banks were staring at bankruptcies. Now to pull the economy out of this gloomy state, the Fed had to do something. And you know its go-to move, right?

Yes. Reducing interest rates and increasing liquidity. It kept doing so until 2013 when it felt the economy was back on track.

Now the 2013 announcement of increasing the interest rates sent shockwaves through India. Rupee fell by over 15% between late-May and late-August 2013 as foreign investments started drying up.

To save Rupee from falling further, the then RBI governor, Mr. Raghuram Rajan, introduced something called Foreign Currency Non-Resident (Bank) Deposit to lure NRIs to deposit surplus dollars in exchange for fixed interest rates and protect them from exchange risk fluctuations. It led to an inflow of $30 billion which cushioned the impact on the economy.

Would we have enough cushion this time? It's anybody's guess!

Well, what do you think will happen this time? Is the economy prepared to face a taper?

Let us know on Twitter!

Share this important update with your friends on Whatsapp or Twitter.

If you are coming here for the very first time: Don’t forget to join us on WhatsApp to get daily updates! 👇