The Self Tariff

India isn't losing the manufacturing race to China. It's losing it to itself.

At ReadOn, we don’t just report the markets. We help you understand what truly drives them, so your next decision isn’t just informed, it’s intelligent.

India’s plan to become the world’s factory is straightforward.

Step one: decide you want to make everything. Step two: tax the materials you need to make anything. Step three: introduce a certification system that holds those taxed materials at customs. For inputs that make it through anyway, add an anti-dumping duty.

Then launch an incentive scheme to reward the factories that survived all of the above.

This is not satire. It has been Indian trade policy since 2018, and a new paper from CSEP and IDE-JETRO has put a number on what it has cost. Mind you, the number is not small.

How India Got Here

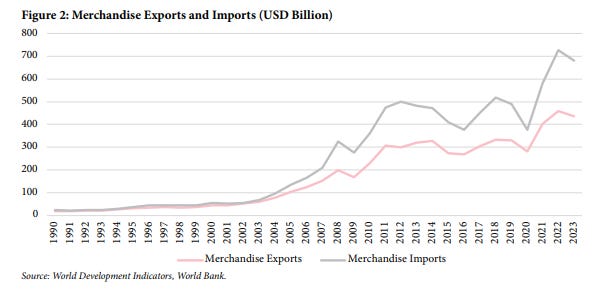

After the balance-of-payments crisis of 1991, India spent nearly three decades liberalising. Import tariffs fell from around 56% to roughly 14% by 2017. Foreign investment came in. Trade volumes expanded. The economy opened up in ways that looked, for a while, like a structural shift.

Source: Mechandise Exports and Imports

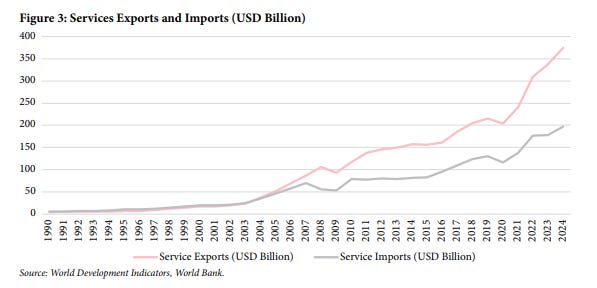

Source: Services Exports and Imports

Then something changed.

From 2018 onward, the direction reversed. Average import tariffs climbed back up to 17.6% by 2024. That headline number, though, understates what actually happened. Alongside the tariff hikes, the government deployed a separate instrument most people outside manufacturing circles have never heard of, Quality Control Orders, or QCOs. These are mandatory certification requirements under the Bureau of Indian Standards. Any product covered by a QCO must meet Indian standards certification before it can be sold or imported into the country.

In principle, QCOs are about product safety and quality. In practice, the way they have been applied tells a different story. The number of products covered by QCOs jumped from 88 in 2019 to 765 by 2024. Around half of those QCOs apply to intermediate goods, components and raw materials used in production, not finished consumer products. Anti-dumping duty initiations, which are separate again, also kept rising throughout this period, with China absorbing more than a quarter of all India’s initiations between 1995 and 2024.

The cumulative effect of all this arrived quietly, the way these things usually do. Net FDI inflows fell 38.3% between 2021 and 2024. India’s share of global merchandise exports has been stuck just above 2% for a decade. Vietnam, for context, went from 0.3% in 2001 to 1.7% in 2023, and is still climbing.

Source: Share in Global Mechandise Exports (%)

These trends do not exist in isolation. They are connected.

The Problem With Protecting Inputs

The paper’s most important contribution is a granular breakdown of exactly what India is protecting, and at what cost.

Of 3,927 product lines analysed at the HS-6 digit level, which is about as detailed as trade data gets, 92.5% carry non-zero import tariffs. The dominant tariff band, covering 54% of India’s total import value, sits between 10% and 15%. The goods sitting inside that band? Primarily intermediate and capital goods. Not luxury items. Not finished consumer products. The stuff that goes into making things.

Zoom in further and the picture gets more uncomfortable. Products facing tariffs of 10% or more that are classified as intermediate or capital goods account for USD 148 billion in imports, roughly a third of India’s entire import basket. These are goods India imports in large volumes precisely because it cannot yet produce them competitively at home. And yet they face the highest cumulative protection. In some cases, tariffs are stacked on top of QCOs, stacked on top of anti-dumping duties, three separate instruments applied to the same product simultaneously.

Plastics. Organic chemicals. Iron and steel. Aluminium. These are not obscure niche materials. They are foundational industrial inputs, and they are among the most heavily protected goods in the Indian import system.

The economic logic of what this does is not complicated. When your inputs cost more than your competitors’ inputs, your outputs cost more than your competitors’ outputs. When your outputs cost more, you cannot price competitively in export markets. The protection that was designed to build manufacturing is structurally undermining the competitiveness of manufacturing. That loop is the core finding of this paper.

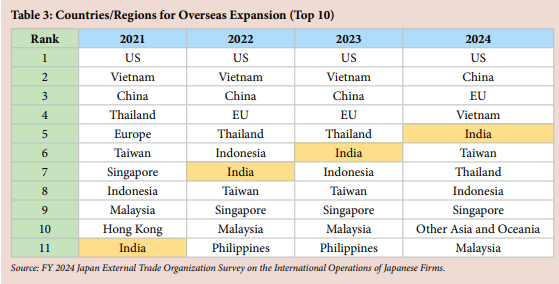

Japanese companies operating in India said as much directly. In a 2025 JETRO survey of 385 companies, the top investment-related concern was time-consuming tax procedures. The second was administrative complexity. In practice, largely the process of obtaining BIS certification under QCO requirements. Among manufacturers specifically, 71.9% reported being affected by the mandatory certification system. Of those, roughly 70% described the impact as serious or extremely severe.

Source: Countries/Regions for Overseas Expansion (Top 10)

One Japanese transport equipment manufacturer put it plainly: products subject to BIS certification are almost always held up at customs during import, causing disruptions. Steel materials, aluminium, bolts, they require the Indian Standard mark to be physically stamped, which means modifying moulds and absorbing additional cost and time burdens. This, they said, is one of the major challenges in positioning India as an export hub.

That is a foreign investor, already in India, explaining why India is hard to use as a base for global production. That feedback matters.

The China Dependency Irony

A large part of the political logic behind India’s protectionism is reducing dependence on China. The anti-dumping data makes this explicit, China is the target of more than a quarter of India’s ADD initiations. The theory is that restricting Chinese imports creates room for Indian firms to grow into the gap.

Source: Percentage of Total Anti-dumping Duty Initiations by Exporter Countries (1995-2024) (%)

The trade data has not cooperated with this theory.

India’s imports from China grew from USD 16.7 billion in 2011 to USD 127 billion in 2024. The fastest-growing import categories from China are intermediate goods and capital goods, the exact inputs that Indian manufacturing is most dependent on. The harder India has tried to reduce its China exposure through tariffs and QCOs, the deeper the structural dependency has become.

This is the trap. Imposing high tariffs on Chinese intermediate goods to protect domestic producers simultaneously raises costs for downstream manufacturers who use those inputs to make their own products. Those manufacturers become less competitive globally. The protection that was meant to build Indian industrial capacity ends up weakening the industries that are supposed to eventually replace Chinese imports with domestic production.

The paper does not mince words here. For India to genuinely become a China-plus-one destination, it needs structural reform in land, labour, R&D, regulatory quality, not reactive trade barriers that hurt Indian manufacturers more than they hurt China.

The Geopolitical Window That Opened and Closed

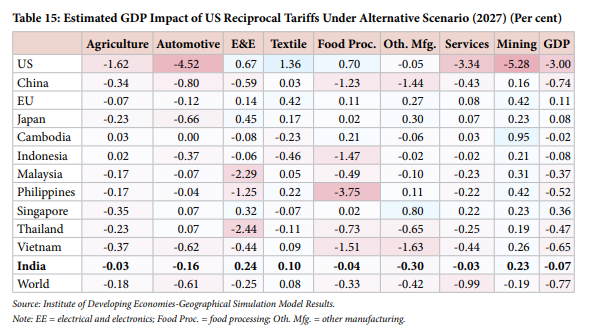

When the US announced its reciprocal tariff policy in April 2025, India briefly looked like a beneficiary.

At a 26% tariff rate, considerably lower than China’s 54%, and with US exports accounting for only 2% of India’s GDP, simulation modelling showed India absorbing a mild positive effect. The logic was trade diversion: with Chinese goods becoming more expensive in the US market, some of that demand would shift to countries facing lower tariffs. India was supposed to be one of them.

Then the bilateral negotiations played out. By late 2025, China had negotiated its effective tariff rate down to 20%. India ended up at 25%, with an additional 25% levy applied to imports of Russian crude oil, creating a composite burden of 50% in some product categories. The 28-point tariff advantage India briefly held over China became a 5-point disadvantage.

Updated simulations show India’s GDP impact from the tariff regime turning slightly negative at -0.07% by 2027. The trade diversion benefit was gone.

The lesson is one that applies well beyond this particular episode. A competitive position built on someone else’s tariff disadvantage is not a competitive position. It is a temporary window that closes the moment the other party negotiates a better deal. India needs to be competitive on its own terms, which requires addressing the cost structure that protectionism has made worse, not better.

What The Numbers Say

The paper runs a liberalisation scenario to put a GDP value on reform. The scenario is not radical reduce India’s average MFN tariff by 2 percentage points, bringing it closer to Thailand’s level, and lower non-tariff barriers modestly, moving India from a global rank of 55th to roughly 44th on trade facilitation metrics.

The result, even under the continuation of US protectionist measures, is a GDP gain of +1.55%. The sectoral breakdown is striking: automobiles gain 3.36%, textiles gain 3.23%, other manufacturing gains 2.97%, mining gains 5.17%.

This is the number that should anchor the conversation. Reducing intermediate goods tariffs, doing less, not more, generates more economic output than the current protectionist architecture. The cost of staying on the current path is not abstract. It is modelled, it is sizable, and it falls disproportionately on the manufacturing sector that the government has staked its industrial ambitions on.

What Actually Needs to Happen

The argument is not for wholesale, unilateral tariff dismantlement. It draws a distinction that has so far been absent from India’s policy conversation. It distinguishes between protection that is strategic, temporary, and tied to genuine capacity-building, and protection that is structural, persistent, and captured by domestic incumbents who benefit from insulation rather than competition.

The immediate asks are not dramatic. Stop adding new tariffs. Fix the inverted duty structures. Remove QCOs from raw materials and components that are not consumer-facing and have no plausible safety rationale.

India has a stated target of USD 1 trillion in merchandise exports by 2030. In the machinery sector alone, one of the most important bellwethers for GVC integration, actual exports are running at 26% of their modelled potential. The gap between ambition and policy architecture is not a communications problem, and it will not be solved by more PLI schemes.

The factory India wants to become is being taxed before it is built.

Until the tariff and the target agree

Readon.