The Resource Curse

Some of India's states are extremely mineral-rich. Then why does none of this translates to actual wealth for the residents of these states?

At ReadOn, we don’t just report the markets. We help you understand what truly drives them, so your next decision isn’t just informed, it’s intelligent.

Across history, battles have been fought over gold, oil, salt, copper, and coal. Minerals have shaped borders, toppled governments, financed wars, and built empires. In today’s world, they matter even more. They power electricity grids, forge steel for infrastructure, form the backbone of manufacturing, enable the energy transition, and sit inside every device from a phone to a jet engine.

One might assume, then, that the regions supplying this backbone of development would be the first to benefit from it. That the districts producing India’s iron ore, coal, bauxite and limestone would be prosperous, well-serviced, and economically dynamic.

But the reality could not be more different.

India’s most mineral-rich states: Jharkhand, Odisha, Chhattisgarh, and pockets of Madhya Pradesh and Rajasthan, consistently appear at the bottom of national rankings on per-capita income, human development, health access, and infrastructure. They remain some of the poorest and most underdeveloped parts of the country, even as their minerals feed the factories, power plants and construction sites driving growth elsewhere.

This contradiction sits at the heart of India’s economy…quite literally. Look closely, and it is the landlocked mineral states that lag, while the coastal ones surge ahead. As Aravind Adiga wrote in The White Tiger:

“Please understand, Your Excellency, that India is two countries: an India of Light, and an India of Darkness. The ocean brings light to my country… Every place on the map of India near the ocean is well-off. But the river brings darkness.”

So how can the states that produce the raw materials of development remain the least developed? Why does mineral abundance correlate with low household consumption, volatile growth, and weak structural transformation?

To answer these questions, we need to examine the economic structure of India’s mineral regions, and the way mineral value flows, or fails to flow, into the lives of the people who live above these resources.

The Pattern Has Been Hiding in Plain Sight

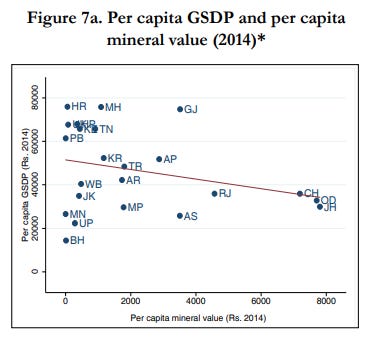

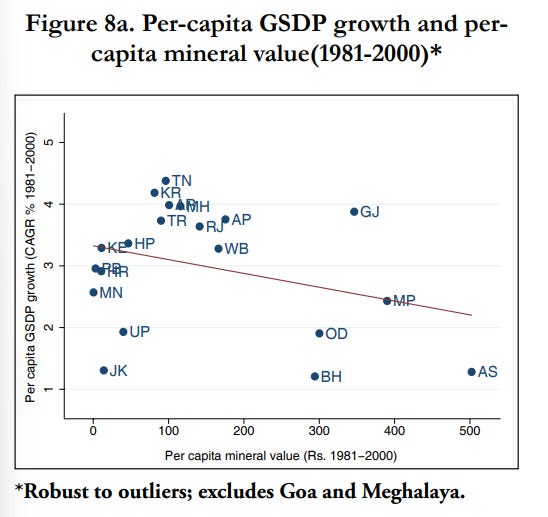

This is not a new observation. The Economic Survey 2016-17 was one of the first official documents to map this paradox across India’s states, and its findings were clear. When it plotted states by per-capita mineral value against per-capita GSDP, the pattern that emerged was almost perfectly negative.

The richer the land was in minerals, the poorer the people living on it tended to be.

Odisha, Jharkhand and Chhattisgarh, home to some of the world’s richest deposits of iron ore, coal and bauxite, clustered in the bottom-right quadrant: high mineral abundance, low average incomes.

Nearly a decade later, the story remains unchanged. Updated 2023-24 state income data puts Odisha at ₹1.82 lakh per capita, Chhattisgarh at ₹1.47 lakh, and Jharkhand at ₹1.05 lakh, all well below India’s average of ₹2.5 lakh, and far behind coastal states like Gujarat at ₹2.97 lakh and Tamil Nadu at ₹2.70 lakh.

Income is only one lens. Household well-being tells an even starker story.

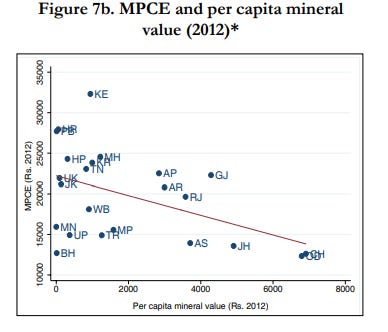

The Survey’s second plot, monthly per-capita consumption expenditure versus mineral abundance, sloped downward as well.

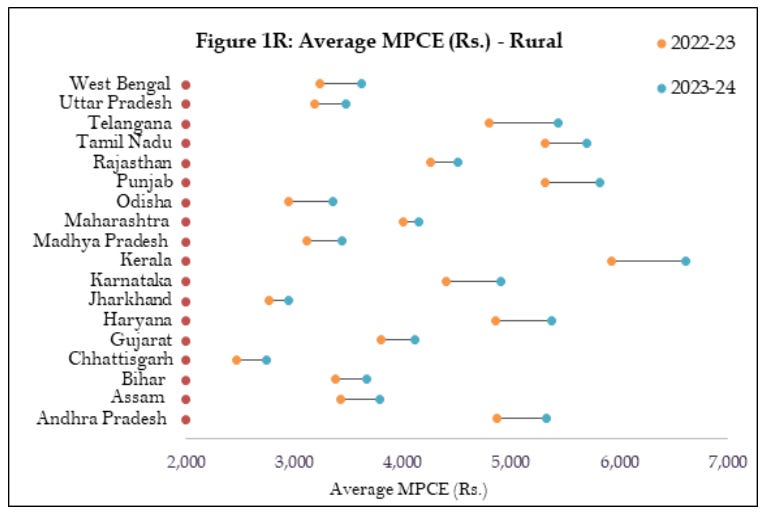

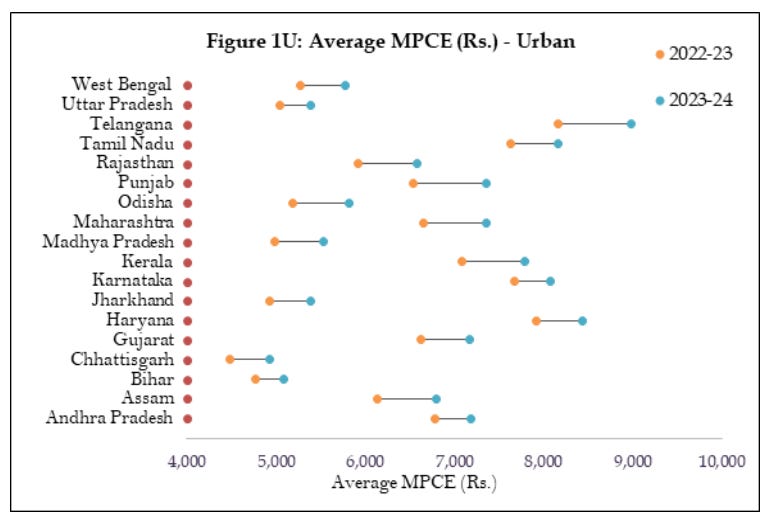

Mineral-rich states didn’t just earn less; they consumed less. The latest NSO consumption survey (2022-23) reinforces this. States that dominate India’s mining output continue to report some of the lowest household consumption levels in the country.

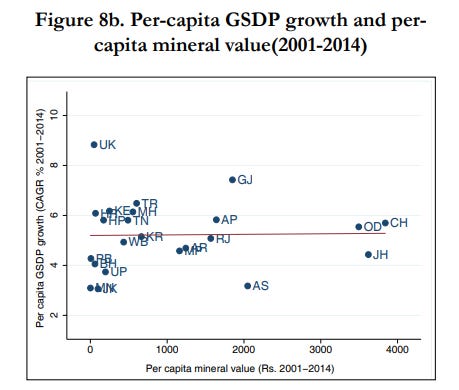

The puzzle deepens when we examine long-term growth. Between 1981 and 2000, decades of reforms, liberalization, and rising national GDP, India’s mineral-rich states actually grew slower than mineral-poor ones.

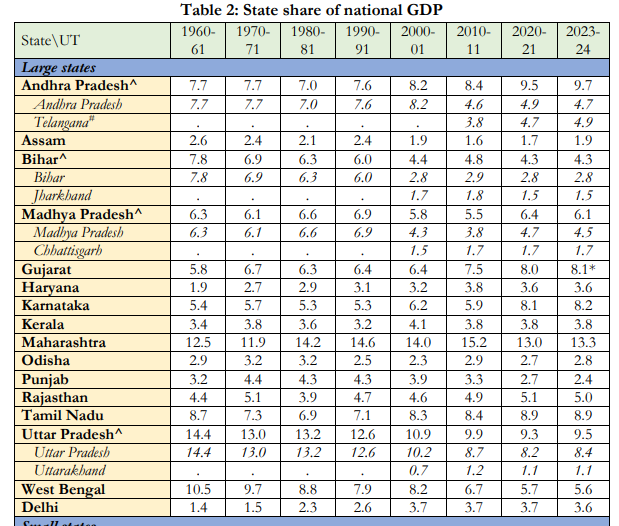

Commodity price cycles, governance frictions, and limited diversification kept them from catching up. After 2000, the gap narrowed, but never reversed. Between FY01 and FY23, Gujarat’s share of India’s GDP rose from 6.4% to 8.1%, while Chhattisgarh’s contribution has remained largely flat at 1.7% since the state’s creation.

Taken together, the data paints a consistent picture. Mineral abundance in India correlates with lower income, lower consumption, and slower structural transformation.

Which brings us to the central question. What is it about the structure of mineral economies that keeps them from turning geological wealth into human prosperity?

Mining as an Enclave, Not an Engine

In theory, minerals should function like any other productive asset: creating jobs, stimulating industry, and raising incomes. In practice, mining behaves very differently.

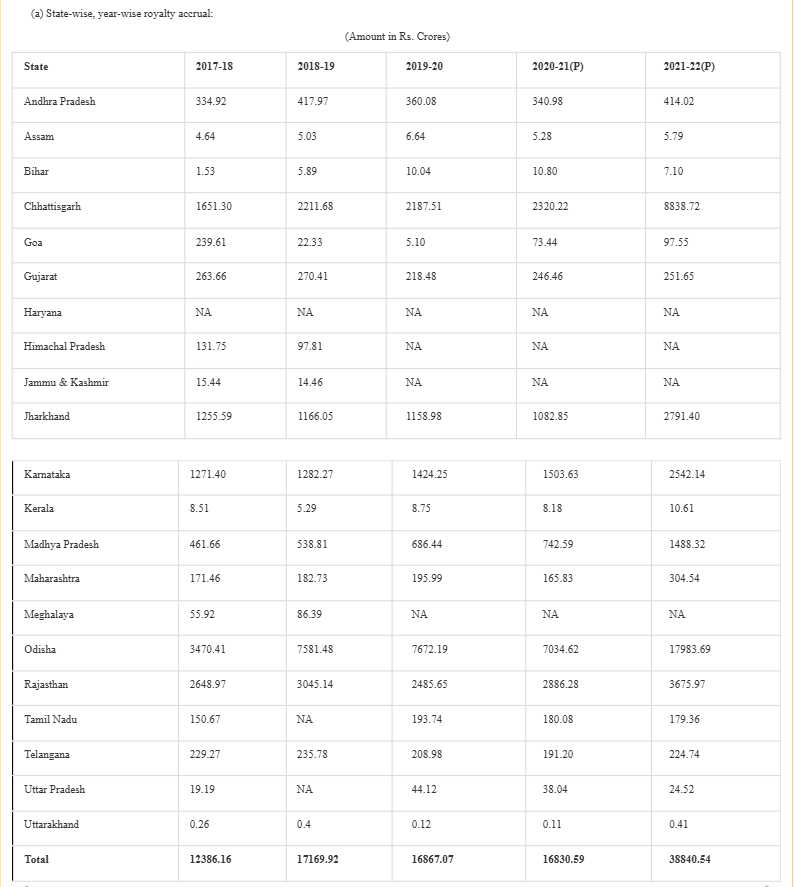

If mineral-rich states are not visibly wealthier, it’s not because mining generates no money. It does. In fact, it generates a lot. States earn through royalty payments (the biggest stream, charged per tonne of ore extracted), auction premiums (introduced post-2015, often 100-150% of benchmark price), dead rent (fixed annual lease fees), and District Mineral Foundations (10-30% of royalty earmarked for local welfare).

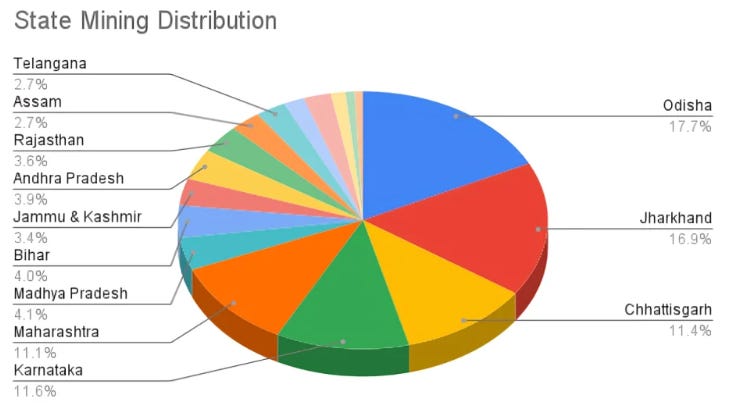

For instance, Odisha accounts for 46% of India’s total royalty revenue, Chhattisgarh accounts for 22%, Jharkhand for around 7%.

But these inflows, though large, are administrative revenues, not the product of diversified economic activity. Royalties are not like taxes on income or production. They don’t reflect rising wages, expanding industries, or broad-based development. They merely reflect how much mineral left the ground, not how much value stayed behind.

The way this money enters the state economy, and the way it moves thereafter, limits its power to create growth.

The Revenue That Doesn’t Multiply

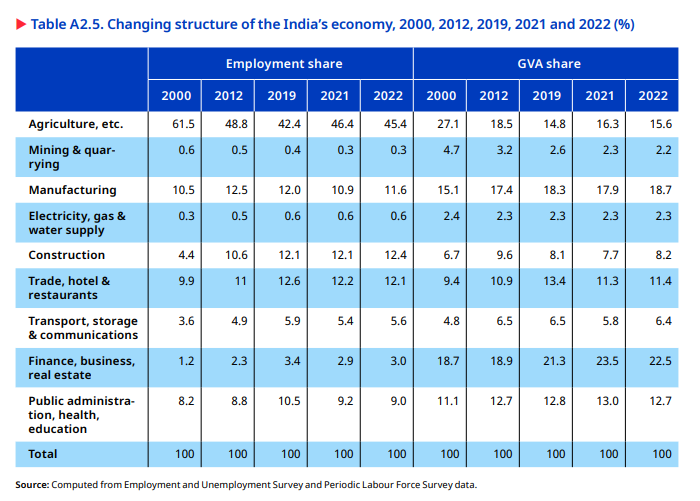

India’s mineral output has grown dramatically. Iron ore production increased from 129 million tonnes in 2014-15 to 258 million tonnes in 2022-23. Limestone output grew from 295 million tonnes to 406 million tonnes over the same period. Yet the mining sector’s gross value added has been stuck at around 2% of national GDP for over a decade.

Employment tells an even more revealing story. According to PLFS data (2022), mining employs just 0.3% of India’s workforce, down from 0.6% in 2000. Compare this with the electricity, gas and water supply sector, also capital-intensive, contributing 2.3% to GVA (almost identical to mining’s 2.2%). Yet electricity employs 0.6% of workers, double that of mining.

More strikingly, while electricity’s employment share has doubled from 0.3% in 2000 to 0.6% in 2022, mining has gone the opposite direction: both its GDP share and its employment share have declined simultaneously.

Two sectors with equally small GDP contributions have taken opposite developmental paths. One gradually absorbs more workers; the other sheds them. For mineral-rich states that rely heavily on mining, this becomes a structural trap. The dominant activity in their regional economy is the one generating less value and fewer jobs every year.

Jharkhand illustrates this with brutal clarity. The state derives 17% of its revenue receipts (₹19,300 crore) from non-tax sources. Of this, mining royalties: ₹15,550 crore, account for nearly 80%. Yet, despite this fiscal dependence on minerals, the mining sector in Jharkhand directly employs only around 20,000 workers.

Compare this with a manufacturing cluster. Every factory generates jobs, supports MSMEs, stimulates construction, increases transport demand, encourages urbanization, and raises local consumption. Mining misses most of this. The supply chain is short, capital-intensive, and geographically isolated. Equipment, machinery, and expertise are often imported from outside the state. So even when royalties rise, local markets don’t boom, urban cores don’t expand, skill levels don’t rise, and household incomes remain flat.

District Mineral Foundations (DMFs) were created in 2015 to ensure that mining-affected communities benefit directly from mineral wealth. By mid-2025, they had collected over ₹1.09 lakh crore, with Odisha holding ₹31,323 crore, Chhattisgarh ₹15,402 crore, and Jharkhand ₹13,791 crore. Yet only 40–50% of this money has been used. Even in 2020, Odisha still had ₹6,707 crore unspent, Jharkhand ₹2,772 crore, and Chhattisgarh ₹1,622 crore.

District-level data reveals why.

Keonjhar in Odisha spent only 46% of its ₹11,541 crore DMF corpus, much of it on low-priority construction.

Korba in Chhattisgarh used ₹607 crore of ₹1,320 crore, directing nearly half to urban amenities rather than mining-affected villages.

This reflects a deeper structural problem: mining generates revenue faster than institutions can meaningfully deploy it, creating governments that appear fiscally rich while citizens remain poor.

Volatility is also a problem. Mining behaves like a windfall, not a stable income. Odisha’s non-tax revenue rose by ₹34,850 crore in FY22 due to high iron ore prices, only to contract sharply the next year. Mining contributes 10% of Odisha’s GVA and 90% of its own non-tax revenue, making it highly vulnerable to commodity cycles. The state created a Budget Stabilisation Fund in 2023, but the need for such a buffer highlights the existing challenge. Long-term development cannot rest on revenue that swings so dramatically.

The Hidden Bill

If mining created broad prosperity, its trade-offs might feel justified. But in India’s mineral districts, local costs routinely exceed local gains, producing a deep development deficit.

Environmental damage affects rural livelihoods. ICAR research shows open-cast coal mines reduce agricultural yields by 10-15%; groundwater extraction has pushed parts of Chhattisgarh, Rajasthan and Odisha into “over-exploited” zones; forest loss removes fuel, fodder and income sources. These are permanent economic losses for farming and tribal households.

Mining clusters are also among India’s most polluted, contributing to higher rates of respiratory illness, TB and silicosis, conditions that reduce productivity and deepen poverty.

Social indicators reflect the same neglect. More than 60 million people have been displaced by development projects such as dams, mining and infrastructure since independence. Child stunting still looms at 40% in Keonjhar and West Singhbhum; in West Singhbhum, 96 per 1,000 children die before age five.

Why Coastal Mineral States Prosper

If inland mineral states struggle, the contrast with coastal ones is striking. Gujarat, Maharashtra, Tamil Nadu, and Andhra Pradesh are resource-rich but rank at the top on income and development. Their economies are larger, more diversified, more urbanized, more resilient.

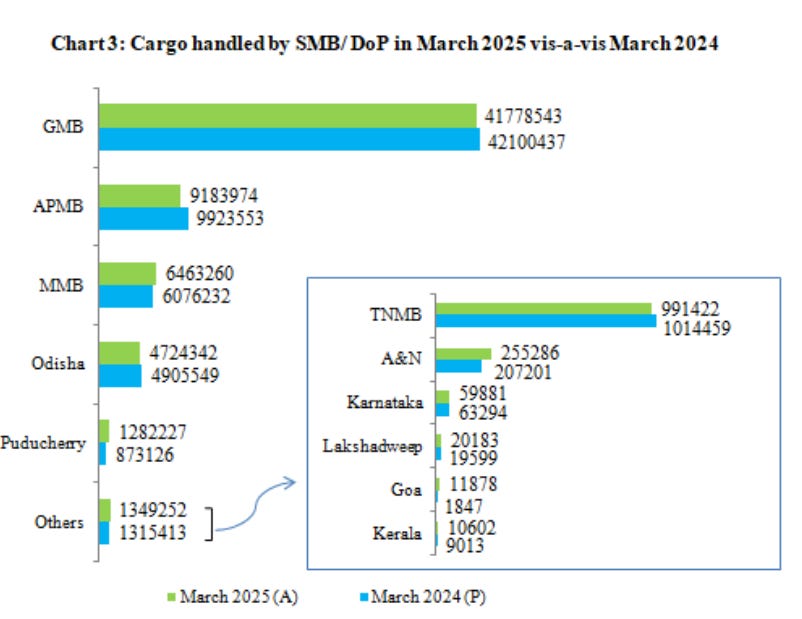

Coastal states have direct access to global markets. Ports reduce export costs and attract industries unrelated to minerals: automobiles, petrochemicals, electronics, textiles, pharmaceuticals, logistics & shipbuilding. Gujarat’s ports handled 41.78 million tonnes in 2024-25 (64% of India’s non-major port traffic).

Maharashtra’s Jawaharlal Nehru Port anchors massive industrial clusters. Tamil Nadu’s Chennai and Tuticorin fuel major manufacturing ecosystems.

While inland states stayed dependent on extraction and basic metal processing, coastal states built layered economies. Take a look at the difference in Gross State Value Added (GSVA) between coastal and inland regions.

Industry contributes 49.3%, services contribute 34.7% to Gujarat’s GSVA. For Tamil Nadu, it’s 53% services with large manufacturing. Maharashtra has 59% services with strong financial and industrial clusters. Contrast with Chhattisgarh that has 62.6% agriculture workforce, and 7.6% manufacturing. Jharkhand has 49.3% workers in agriculture, and 8.9% in manufacturing. Coastal economies pull labor into higher-productivity sectors; inland states push labor out of agriculture but have nowhere to absorb it productively.

Urbanization amplifies this. Maharashtra and Tamil Nadu are 54% urban, Gujarat is 48.7% urban. Chhattisgarh manages 27%, Jharkhand has less. Urbanization creates jobs, consumption markets, service economies, things mining-dependent economies lack.

Coastal states sit at major national corridors, Delhi-Mumbai Industrial Corridor, Sagarmala, East Coast Economic Corridor, Chennai-Bangalore-Mumbai axes. These channel investment and infrastructure into coastal belts. Jharkhand and Chhattisgarh rely on long, expensive rail routes to reach ports, making exports costlier and industrialization slower.

Even Odisha, though coastal, illustrates how mineral dependence constrains growth. Despite port access, the state derives large revenue from mining, and that coastal advantage remains concentrated rather than broadly distributed.

The Bottom Line

Across India’s mineral belt, the economic paradox mirrors a social one. For decades, families in Jharkhand, Chhattisgarh and Odisha surrendered land for mines, plants and corridors hoping for a better future. Compensation arrived once; the mines stayed forever. Modern mining is mechanized, hiring contractors and specialists from outside. The promised jobs didn’t come, and the loss of land, their only lasting economic asset, left them more vulnerable.

Their dissatisfaction surfaces again and again through quotes like these:

“Our grandparents gave their land for mining. Our children still have no work.”

It’s not ideology that fuels protests in these regions. It’s lived memory. Communities watched minerals leave, revenue flow to distant treasuries, while villages remain underserved: schools understaffed, health centers distant, water sources polluted, opportunities scarce. Value extracted from the land rarely becomes value created in their lives.

This experience isn’t uniquely Indian.

Regions relying on mineral extraction like copper towns of Zambia, oil belts of Nigeria, diamond fields of Sierra Leone, coal regions of Appalachia, exhibit similar patterns. High resource output, low local prosperity. When economies depend on what comes out of the ground rather than what people build above it, growth becomes narrow, volatile, exclusionary.

But exceptions exist. Chile, Botswana, Australia escaped the resource trap not because they had more minerals, but because they had institutions to convert mineral rents into long-term public investment like education, health, infrastructure, sovereign wealth funds. They treated mineral booms not as windfalls to spend, but as opportunities to strengthen capabilities of citizens who would power diversified economies.

India’s mineral-rich states stand at a similar crossroads. They have revenue but no mechanisms to turn it into broad prosperity yet. DMF funds remain underutilized. Revenues swing with commodity cycles. Mining creates fiscal surpluses but very few jobs. Environmental and social costs borne locally, deteriorating farmland, polluted air, displacement, health burdens, erode foundations of long-term development.

The lesson is clear. Resource wealth becomes a blessing only when converted into human wealth. Minerals don’t develop economies. People do.