The Global Aluminium Crunch

AluMINium is hitting its price MAXimum!!

At ReadOn, we don’t just report the markets. We help you understand what truly drives them, so your next decision isn’t just informed, it’s intelligent.

On June 8, 2026, LME aluminium traded at $3,594 per tonne. A year earlier, the same tonne cost roughly $2,480. That is a 44.89% price increase over twelve months, and global demand did not slow down for a single quarter of it.

According to a CRISIL report, this price rise could increase revenues for players in India’s wires and cables industry by ~30%, as manufacturers should be able to pass on the rise in prices of key raw materials.

Aluminium’s isn’t the kind of price story that gets reversed by a mild recession. According to Alcoa’s projections, global aluminium consumption is growing at a 2.3% CAGR through 2035, driven by EVs needing lighter frames, solar panels needing aluminium mounts, and power grids expanding faster than ever. The IEA confirms that clean energy transitions will structurally lift demand for decades.

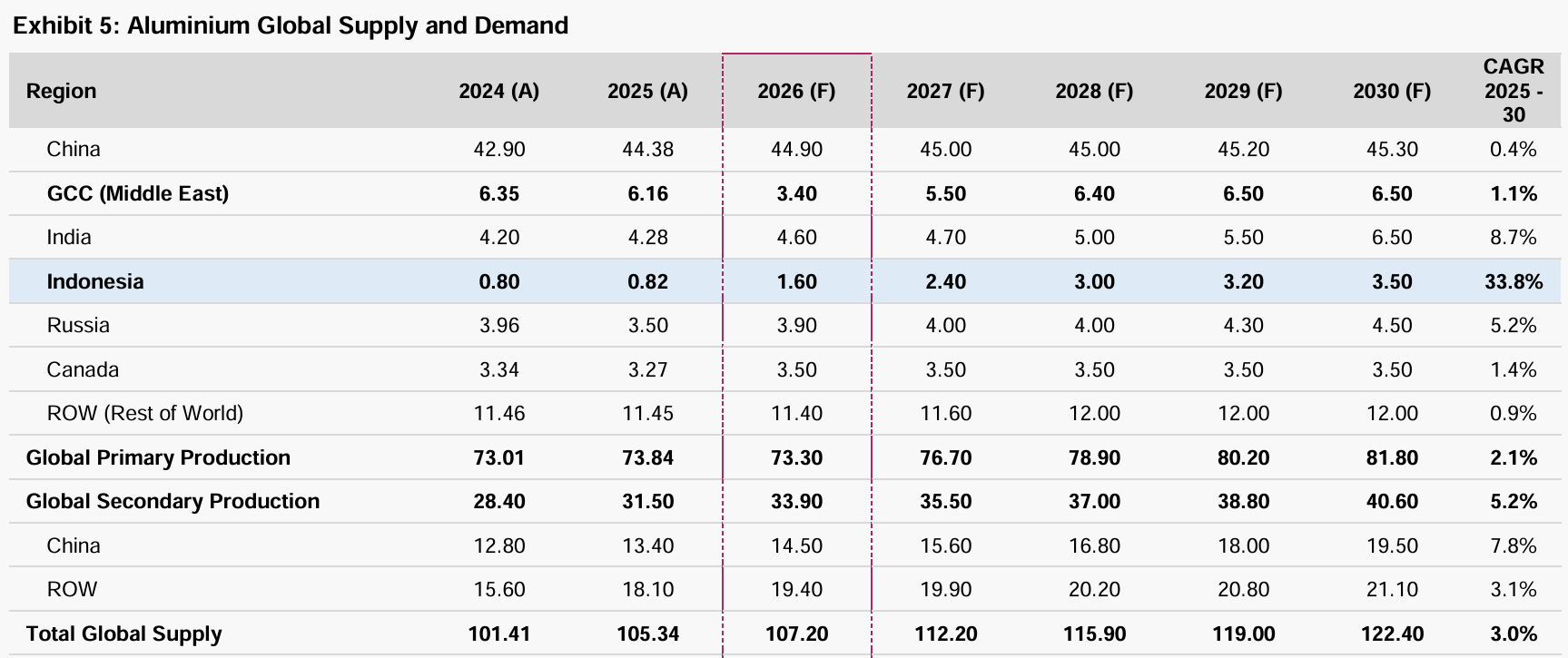

The Axis Securities June 2026 sector report puts global primary aluminium demand at 74.3 million tonnes (MT) in 2025, rising toward 82 MT by 2030. It also forecasts a 1.2 MT primary deficit in 2026 in a market that was balanced just two years ago.

P.S. For all you Diet Coke lovers, (I don’t know what’s wrong with you. Originals’s way better), this aluminium shortage is also the reason Diet Coke production in India hit a speed bump. The shortage of the metal is making it difficult to package and sell the can exclusive beverage.

What makes this crunch unusual is what is not causing it. The earth hasn’t run out of bauxite. There is no smelting technology barrier. The shortage is almost entirely man-made: a product of trade policy, warfare, and the brutal physics of electricity.

Two Reasons the World Doesn’t Have Enough

The first is a ceiling China built for itself.

China produces roughly 60% of the world’s primary aluminium. Since 2017, Beijing has imposed a hard 45 MT annual ceiling on primary smelting capacity. It was a deliberate industrial policy designed to curb energy overconsumption and prevent rampant capacity addition. For years the cap felt theoretical. China reliably produced well below it. In 2025, production reached 44.38 MT and hit the ceiling.

This matters because it removes the single most important buffer the global market ever had. Whenever aluminium ran short, because of a war, a drought affecting hydro plants, an unexpected demand spike, China simply smelted more. That mechanism is structurally gone. Axis Securities projects China’s output plateauing at around 45.3 MT by 2030, a 0.4% CAGR in a market requiring 2% annual growth.

The second driver is war.

The Gulf Cooperation Council is a surprisingly large aluminium producer. The UAE, Bahrain, and Qatar together produced 6.16 MT in 2025, approximately 9% of global primary output. The region built this capacity specifically to monetise cheap natural gas. Smelters like Emirates Global Aluminium (EGA) in Abu Dhabi and Alba in Bahrain became world-class operations. They were low-cost, export-oriented, and strategically placed at the mouth of the Strait of Hormuz.

In early 2026, conflict hit. Direct attacks struck EGA and Alba, and the Strait of Hormuz, the chokepoint through which virtually all GCC aluminium exports flow, was blockaded. Combined with the shutdown of South 32’s Mozambique smelter and disruptions in Iceland, Axis Securities estimates roughly 3.3 MT of global output was effectively removed from the market in 2026. The GCC’s forecast production drops from 6.16 MT in 2025 to just 3.4 MT in 2026.

ING’s commodities team warned in March 2026 that a severe disruption scenario could briefly push prices above $4,000/t. On June 2, aluminium touched $3,850. China has tried to plug the gap. May exports surged 16% year-on-year to 630,000 tonnes, one of the strongest monthly performances in years. It still wasn’t enough. The global deficit persists.

Indonesia: The Release Valve That Isn’t Quite Open

In the middle of all this, Indonesia has become the most closely watched supply story in commodities.

The archipelago sits on large bauxite reserves and has attracted Chinese-backed smelter projects across North Kalimantan, Sulawesi, and West Kalimantan. The total pipeline targets a nameplate capacity of 14.9 MT by 2030, which would make Indonesia one of the top producers on earth. Axis Securities estimates 1,230 ktpa of new Indonesian capacity coming online in 2026 alone.

But 14.9 MT is almost certainly a fantasy. Fastmarkets’ base case for Indonesian output by 2030 is 3.4–3.5 MT. The constraint isn’t capital, and it isn’t ore. It’s electricity.

Aluminium smelting consumes roughly 14-15 MWh per tonne of metal produced. Scaling to 14.9 MT would require approximately 24 GW of dedicated power capacity. Indonesia’s entire national grid in 2025 stood at 107.5 GW. Achieving the target would devour roughly 22% of the country’s total electricity capacity just for aluminium smelters.

There’s a longer-term trap buried here too. Almost every project in the pipeline runs on captive coal power. The EU’s Carbon Border Adjustment Mechanism (CBAM), which entered its definitive phase in 2026, will progressively impose costs of $150–$230/t on high-carbon aluminium entering European markets by 2028–2030. Indonesian coal-based metal will feel that headwind directly.

Indonesia’s state miner PT Inalum has already urged the government to impose a moratorium on new alumina and aluminium facility licenses, worried the sector is headed for a nickel-style overcapacity crash, where Indonesia’s aggressive expansion of Chinese-backed mining and smelter operations created a massive global nickel oversupply. The government has not yet acted. Projects are proceeding, and Indonesia’s production will likely grow meaningfully, from 0.82 MT in 2025 to perhaps 3.5 MT by 2030. But that is not a solution. It’s more of a temporary relief valve.

India: Well-Positioned, and About to Get Bigger

India is the world’s second-largest primary aluminium producer outside China, contributing roughly 6% of global primary supply. Output reached 4.28 MT in 2025. Axis Securities projects it climbing to 6.5 MT by 2030 (an 8.7% CAGR), faster than any other major producing nation.

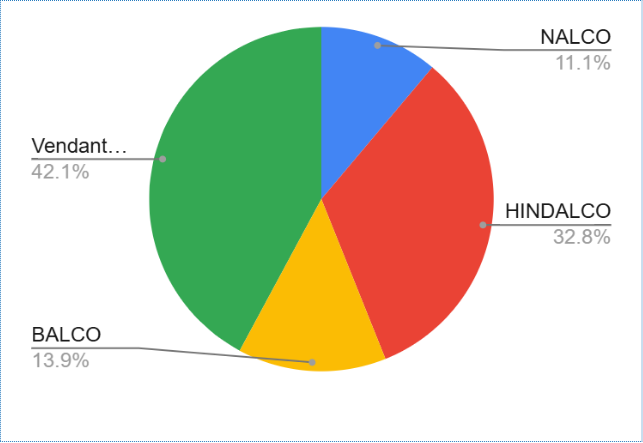

Three companies drive almost all of it. Hindalco Industries, NALCO and Vedanta account for ~90% of India’s 4.6 MT capacity. Hindalco Industries (Aditya Birla Group) sits in the first quartile of the global cost curve at $1,500–$1,720/t integrated cost, its EBITDA per tonne reached $1,572 in 2025. Expansion plans include 180 ktpa of new capacity at Aditya Aluminium in Odisha by FY28 (Phase I) and 193 ktpa more by FY29 (Phase II). NALCO, the government-owned producer, is adding 500 ktpa at Angul, Odisha by 2030. Vedanta is building a greenfield 1,000 ktpa smelter at Dhenkanal, Odisha, commissioning in phases through 2029.

The strategic differentiator going forward is energy. India’s Big Four (Hindalco, NALCO, Vedanta, and BALCO) have collectively committed to a $5 billion investment in 20 GW of renewable energy capacity by 2030. As CBAM progressively taxes coal-heavy metal at European borders, green-certified Indian aluminium could command a meaningful premium, a trade route Indonesia’s coal-powered capacity cannot access.

The Takeaway

This crunch is, at its core, a story about where cheap, well-located supply used to come from, and what happens when it stops. Chinese smelters under a government cap. Gulf smelters under fire. Indonesian smelters starved of electricity. The world’s aluminium cost floor has permanently shifted from ~$1,600/t in 2014 to $2,053/t today, and Axis Securities believes prices will not retreat below $2,500/t again.

There’s a new force accelerating that shift. AI data centres are now outbidding aluminium smelters for baseload power, willing to pay $115/MWh against the $40/MWh threshold at which smelting stays viable. Every $10/MWh rise in electricity adds $125–$150/t to production costs.

The question for investors isn’t whether aluminium prices stay elevated. The structural case for that is solid. It’s which producers sit low on the cost curve, with clean enough energy credentials, to prosper in a market where the surplus years are firmly behind us.

Until next time, ReadOn!