The Dawn of FinTech

The Dawn of FinTech

FinTech is one of the most disruptive changes in banking history Read on.

“Change will not come if we wait for some other person, or if we wait for some other time. We are the ones we've been waiting for. We are the change that we seek.”

― Barack Obama

Sit back and grab some popcorn as we take you through one of the most disruptive changes in banking history.

Let’s time travel to 2008.

One moment you are chilling and having a cuppa at your nearest Starbucks, the next moment you find yourself amidst the worst crisis to hit the United States’ economy since the Great Depression of 1929.

What exactly happened and why? Let me tell you a story.

In the early 2000s, investors in the US and abroad started scouring for low risk-high return investments and began tossing their cash at the US housing market. They found a new investment avenue that promised higher returns than other safer bonds - Mortgage-Backed Securities (MBS).

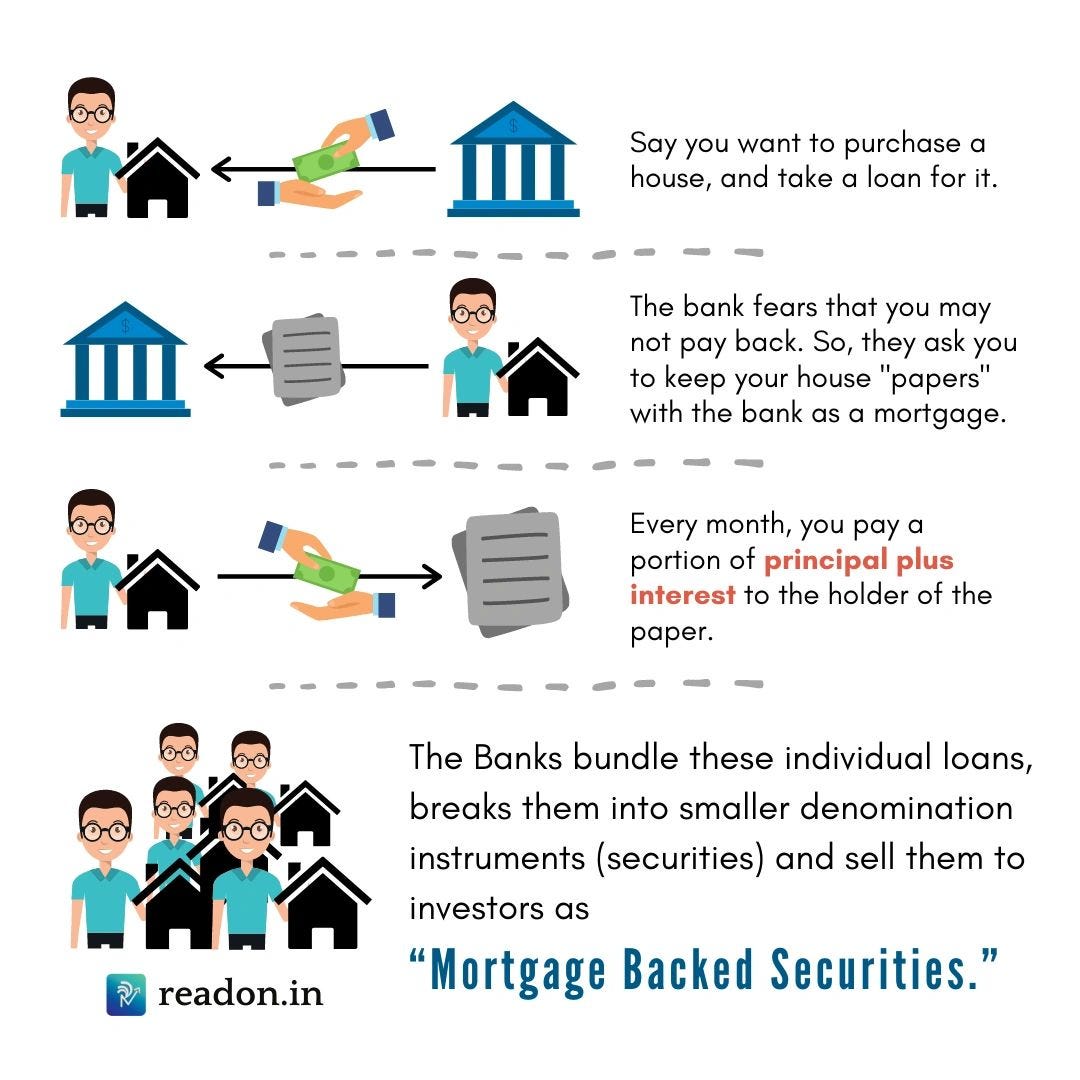

Wait a sec. What? What are Mortgage-Backed Securities?

Here.

The basic plot of the crisis was simple. These large financial institutions bought thousands of individual mortgages, bundled these papers together and sold shares of that large pool to small investors. These seemed to be really safe bets.

Credit rating agencies (institutions that assess a borrower’s ability to repay the debt) such as S&P and Moody’s gave them a triple-A rating, which assured the people that these were good investments.

During the early 2000s, the housing industry saw a boom. Prices were rising. The greedy ones became frantic and wanted to buy more and more of these securities. The lenders thought, even if the borrower defaults (instance wherein the borrower quits paying), they could always sell the asset (the houses) and get their money back.

Lenders did their best to help create more of such securities, for which they needed people to take more loans. They loosened their stringent standards and lent loans to people with poor creditworthiness, known as subprime mortgages. Some extended loans to about 125% of the home value!

So, basically, the foundation was poor. How, you ask?

The credit rating agencies kept showing historical data, which did not reflect the true state of the underlying assets (houses) that backed these bonds. In reality, these investments were becoming riskier every day.

Trusting the credit rating agencies, smaller investors poured more money into this risky quicksand - the US housing market.

This crisis led to a bubble - a rapid increase in prices driven by human greed and irrational buying decisions.

In reality, one could not afford to pay for these houses, creating a shortage of demand and excess supply. As prices fell, some borrowers dreaded mortgage payments exponentially more than what their home was actually worth.

Thus, the housing market bubble burst and the economy crashed. Merrill Lynch forecasted in January of 2008 that housing prices would fall about 15% and would experience a further 10% drop in 2009. The common belief that prices of real estate could only increase was shattered. The big financial institutions stopped buying subprime mortgages and frantic lenders were stuck with bad loans.

"No one can see a bubble. That's what makes it a bubble." This line from The Big Short (2015) perfectly illustrates the calm before the storm of the most hard-hitting financial crises in the United States.

Had you been hit by this situation, you would have lost years and years of hard-earned savings and retirement assets. This also had a domino effect on unemployment; by late 2009, about 5% or 15 million Americans did not have a job.

This was known as the American Housing Bubble of 2008, which brought to light the vulnerabilities in banking operations and resulted in the loss of trust of customers.

For several decades, these brick-and-mortar banks had no true competition, no one to challenge their methods. This gave them the power to monopolise financial services and charge high commissions.

But these were not the only problems.

The incumbent banking models were designed around the products and not humans. Their products were very standardized, expanding the gap between modern customer expectations and the bank’s offerings. To illustrate, money transfers between accounts or usage of checks were tedious and cumbersome processes. Additionally, the traditional banks were also slow to respond to the digitisation of services.

These shortcomings instilled a sense of anger in customers towards the financial system. Plus, they wanted services to be delivered at the click of a button.

The time had come to revolutionize the banking landscape.

From the ashes of the old banking system, a phoenix emerged.

In order to encourage competition and invite new entrants, governments in many countries started making post-crisis regulatory reforms in policies (like reducing minimum capital requirements, providing temporary restricted licensing, and so on). Furthermore, there was a paradigm shift in consumer mentality, which provided a field to new entrants to offer faster, better and more competitive services.

This stimulated the entry of many startups alongside the traditional banks offering core banking solutions with innovations in Application Programming Interface (APIs), Artificial Intelligence (AI), Analytics and Machine Learning (ML).

These new organisations came to be known as FinTechs.

In simple words, FinTech = Finance + Technology. This confluence of two worlds is enabling companies to use technology to provide financial services efficiently, easily and universally.

For a finance and tech enthusiast, could there BE any better combination?

The first wave of FinTech revolution started in early 2009 and lasted until the end of 2019. Wave 1.0 was predominantly experienced in the US, Europe and China while India and other Asian countries were in the stage of infrastructure development. According to a report by KPMG, venture capitalist funding for Fin-Tech rose from $50.8 billion in 2017 to $111.8 billion in 2018. A whopping 120% jump.

Fintech companies recognised that Gen-Z needed hassle-free services with minimum effort. Gradually, in 8-10 years, people got comfortable with sharing their card details on a payment gateway for online transactions, using online services for buying and selling and using phone numbers for small day-to-day transactions. Thanks to UPI, the Indian payments landscape was transformed completely.

This is where New Banks have found an opportunity and are beginning to step up. Adding value to what a traditional bank is already offering.

Hence, began the era of FinTech 2.0, where customized banking services brought in the concept of One to One Banking or Personalized Banking.

So, who is this new king in the North? Will it challenge the status quo?

Stay tuned for more.

Brought to you by Adhya and Shruti, who are now our go-to people for anything related to FinTech. Balancing college and a job, they have burnt their midnight phone batteries to deeply research this piece and present it to you.

Thousands of readers get our daily updates directly on WhatsApp! 👇 Join now!