Private Equity Needs a Doctor

This is sick (in a good and bad way)!

At ReadOn, we don’t just report the markets. We help you understand what truly drives them, so your next decision isn’t just informed, it’s intelligent.

Seven of the world’s most powerful private equity firms are in a bidding war. The prize? A 25% stake in Cloudnine Hospitals, India’s largest maternity and paediatric chain. KKR, TPG Capital, Warburg Pincus, Advent International, CVC Capital Partners, Permira, and domestic fund Kedaara Capital are all competing for a slice of a company that posted ₹2,000 crore in revenue and ₹300 crore in EBITDA in FY26, at a valuation of ₹10,000 crore. Allegro Capital is running the sale. Initial bids are due in the first week of July.

That’s not normal deal activity, but a signal about how comprehensively global capital has repositioned India’s healthcare sector within its investment hierarchy.

Private equity’s infatuation with Indian hospitals has deepened markedly since 2020. Between 2022 and 2024, India’s healthcare sector logged over $30 billion in total M&A and PE transactions. Hospitals alone attracted $4.96 billion in PE inflows, accounting for nearly 40% of all deal value, and in 2024 alone, that figure swelled to $6 billion, a 24% jump year-on-year. The deals have not been timid. Blackstone now holds roughly 80% of KIMS Kerala and 73% of Care Hospitals. Temasek holds around 59% of Manipal hospitals. In March 2026, Manipal filed for a $1.17 billion IPO. The ownership map of Indian healthcare is being comprehensively redrawn.

But what’s the prognosis on PEs investing in Indian hospitals? Let’s find out!

Before PE Arrived, There Were Doctors

For most of India’s post-independence history, hospitals were built and run by the doctors who practised in them. A senior cardiologist in Pune or a gynaecologist in Bengaluru would pool personal savings, take a bank loan, buy a plot, and build a facility around their clinical reputation and referral network. Quality depended entirely on the founding physician’s skills. Scale depended on how much more they could borrow, how many hours they could spare from patients, and how much administrative chaos they could tolerate. Most hospitals stayed small. Most stayed local.

The limitations were baked in. A doctor-promoter running a 50-bed facility in Coimbatore was simultaneously a clinician, HR manager, supply chain head, and real estate developer. Capital was the permanent bottleneck. Good medical outcomes did not automatically translate into institutional growth, and banks were reluctant to lend at scale to what were essentially single-founder businesses tied to one doctor’s reputation.

What broke the mold was Covid-19. The pandemic made two things undeniable, India’s healthcare capacity was dangerously insufficient, and hospitals, unlike retail or hospitality, maintained cash flows through economic shocks. PE funds took serious notice.

The Sahyadri Hospitals story is the clearest illustration of the switch. The Pune chain’s founders sold to Everstone in 2019 for ~₹1,000 crore. Within a year, Everstone exited, selling to Ontario Teachers’ Pension Plan for ~₹2,500 crore. By 2025, Temasek-backed Manipal acquired the chain at ~₹6,400 crore. Three ownership changes in six years, each at dramatically higher valuations. That compounding, achieved through geographic expansion, operational standardization, brand building, and bed additions, is exactly what PE capital is engineered for. So while the doctor-promoter model solved for access, it was PE that solved for scale.

The Investment Case Is Hard to Argue With

Source: imarc

The structural logic for investing in Indian hospitals is difficult to dismiss. The market reached $193 billion in 2025 and is projected to more than double to $364 billion by 2034 at a 7.3% CAGR. That trajectory is powered by constant undersupply. India has just 1.3 hospital beds per 1,000 people, against the WHO-recommended 3. This translates into a shortfall of 2.4 million beds. There’s no need to manufacture demand in this sector yet, there’s still sufficient organic demand waiting to be met.

Then there’s the insurance shift. Ayushman Bharat and parallel state schemes have dramatically expanded formal coverage. Rural insurance penetration reached 47.4% in 2025, actually outpacing urban levels. For hospitals, insured patients mean predictable, guaranteed payment streams that aren’t dependent on a family’s savings account. That change in revenue quality explains why investors are paying 20x to 30x EBITDA for quality hospital assets.

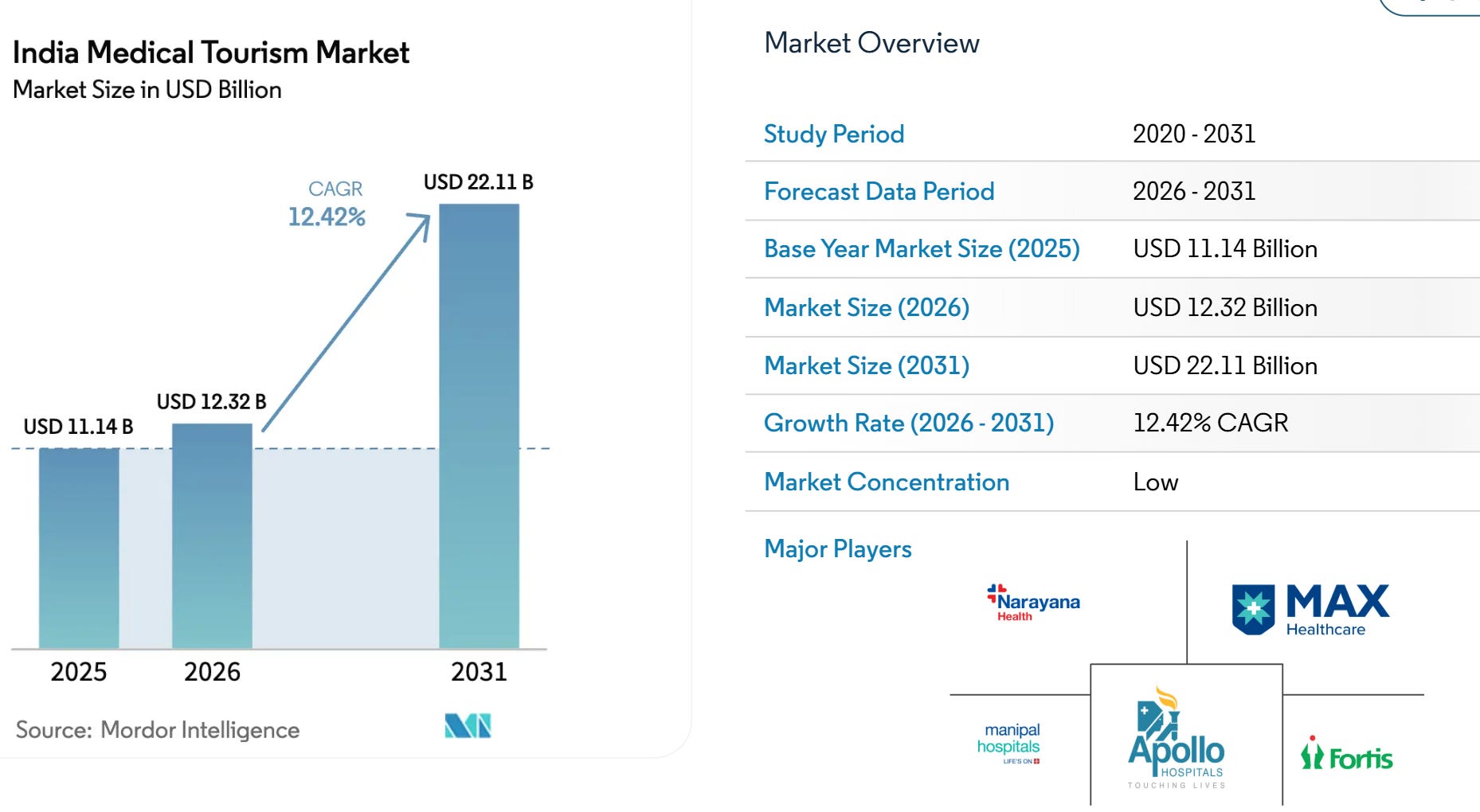

Source: modorintelligence

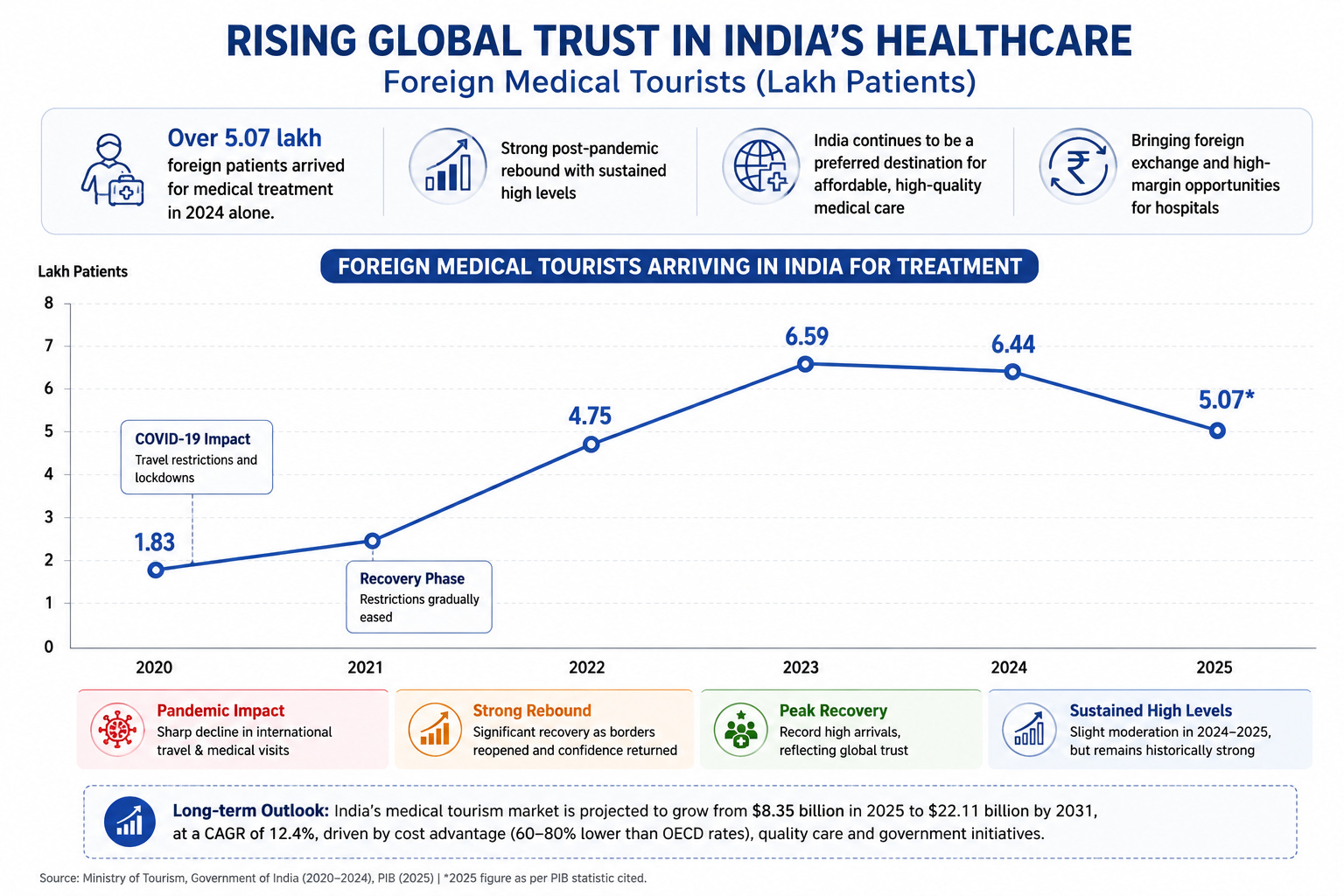

And then there’s medical tourism. India’s medical tourism market was valued at $8.35 billion in 2025 and is projected to nearly triple to $22.11 billion by 2031, growing at a 12.4% annual rate. The reason for this success? Procedures in India cost 60–80% less than OECD rates. A bypass surgery that runs $100,000 in the United States starts at $5,000 here. Over 5.07 lakh foreign patients arrived for medical treatment in 2024 alone, and the numbers are rising. For a PE-backed hospital chain, these are premium-paying, high-margin patients who bring foreign exchange directly into the revenue line.

Source: Ministry of Tourism, Government of India (2020-2024), PIB (2025)

The Question Nobody Wants to Answer

PE funds exist to generate returns, typically targeting a tripling of invested capital on exit. That imperative can sit very uneasily with the purpose of a hospital.

India’s out-of-pocket health expenditure, or what ordinary families pay directly from their own pockets, still accounts for roughly 37% of total health spending. Down from nearly 70% two decades ago, yes. But still high enough to make every serious illness a potential financial catastrophe. Around 400 million Indians remain without meaningful insurance. An estimated 7% of the population is pushed below the poverty line by medical costs each year. India’s overall insurance penetration sits at 3.7% of GDP. That’s roughly half the global average, and even insured patients find that reimbursements often fall short of what is actually billed.

The United States is the cautionary tale here. PE entered American healthcare aggressively through the 2000s and 2010s. Research consistently found that PE-owned hospitals charge higher prices, increase procedure volumes, and engage in more aggressive billing than their non-PE counterparts, with clinicians facing pressure to maximise “revenue per patient.” Debt-loaded acquisitions have led, in some cases, to rural service cuts and even hospital closures, leaving patients in medical deserts. The endpoint? Medical bills are the leading cause of personal bankruptcy in the US, accounting for 66.5% of all filings.

India isn’t there. But the vulnerabilities are structurally present. Hospital assets now trade at 20x–30x EBITDA, which means PE firms need sustained margin expansion to justify those entry prices on exit. When that pressure is applied inside a hospital, it tends to appear as higher room tariffs, upsold diagnostics, and bills that quietly creep beyond insurance caps. The middle-income patient without comprehensive coverage absorbs the difference.

The affordability question carries one more dimension that rarely surfaces in deal memos. India’s medical tourism proposition, with over $8 billion in annual foreign exchange, rests entirely on cost arbitrage with the developed world. If private hospital pricing drifts upward under return pressure, that advantage erodes. The patient who would have flown from Nairobi or Dhaka to Chennai will simply choose Bangkok instead. India’s medical tourism windfall does not survive in a world where Indian hospitals price like American ones.

The Takeaway

The Cloudnine bidding war is a genuine vote of confidence in Indian healthcare’s future. Seven global funds see real tailwinds in demographics, bed shortages, insurance expansion, a growing middle class, and a medical tourism industry still in its early innings. The capital will help Cloudnine expand its network, modernize facilities, and reach more patients. That is an optimistic reading, and it is not wrong.

The harder question is what gets optimized once the exit clock starts ticking. In a software company, that typically means cutting R&D or delaying hires. In a hospital, the answer doesn’t show up in a quarterly filing, but at the billing counter, at 2 AM, when someone’s family is deciding what they can and cannot afford.

Until next time, ReadOn!