Private Credit's Global Struggle

Defaults are rising. People clearly aren't giving credit where it's due!

At ReadOn, we don’t just report the markets. We help you understand what truly drives them, so your next decision isn’t just informed, it’s intelligent.

In April 2026, US private credit defaults touched a record 6%, up from 5.8% a year earlier, according to Fitch Ratings. The same week, the Financial Stability Board (the global body that watches for the next 2008), warned that a $2 trillion industry has become the AI boom’s biggest financier, and that a “sharp correction” in AI valuations could trigger sizeable losses across the system.

That’s an odd combination. Private credit is bigger than it’s ever been. And it’s also more stressed than it’s been in years. Both things are true at once, and that tension is the story.

For over a decade, private credit, or non-bank lenders giving loans directly to companies that banks won’t touch, has been one of finance’s secret success stories. It ballooned from roughly $2 trillion in 2020 to $3 trillion by early 2025, and Morgan Stanley now projects it’ll touch roughly $5 trillion by 2029, even as the AUM growth itself starts crossing $2 trillion in 2026 against rising redemptions, fund closures, and bankruptcies. Pension funds loved it. Retail investors piled in. Their share of the market went from near zero to 13% over ten years, per the FSB. Everyone got comfortable.

Now the comfort is wearing thin. Disbursals are slowing, defaults are climbing, and across multiple major economies, the cracks are showing up in remarkably similar places.

Where the Cracks Are Showing

The United States is ground zero. Beyond that headline 6% default rate, Fitch found that private-credit-backed corporates recorded a 9.2% default rate through 2025. Proskauer’s Private Credit Default Index, which tracks nearly 700 loans worth $189 billion, showed defaults jumping from 1.84% to 2.73% in just two quarters. And the range of “how bad could this get” estimates is wide enough to be unsettling. Morgan Stanley says defaults could approach 8% in a weaker economy, while UBS has floated a worst-case scenario of 14-15%, per the same report.

What makes 2026 different from past stress episodes is how the defaults are showing up. According to Moody’s, roughly 65% of 2025’s private credit defaults weren’t outright bankruptcies. They were “distressed exchanges,” where lenders renegotiate terms instead of forcing a default on paper. Fitch puts the number even higher for the 12 months to March 2026, where 94% of all private credit downgrades were distressed exchanges. In plain English, a lot of “performing” loans are performing because lenders are pretending they are, not because borrowers can actually pay.

There’s also a maturity wall. Roughly $162 billion in private credit debt needs refinancing in 2026, at rates far higher than when it was originally written. Smaller borrowers are getting hit hardest. Companies with EBITDA under $25 million logged a 15.8% default rate in 2025.

Europe, meanwhile, is having the opposite growth problem but the same risk problem. Fundraising hit a record $66 billion in the first nine months of 2025, according to S&P Global, as investors who’d overloaded on US direct lending started diversifying geographically. But the same report notes the “true” default rate (once you count distressed exchanges) had already crept to around 5% through the first nine months of 2025, even as headline numbers stayed comfortably under 2%. The growth is real. So is the rot underneath it.

The UK has its own concentration problem. The top five asset managers now control more than half of all gross assets in UK-managed private credit funds, per the FSB’s findings. Globally, just five large groups account for roughly a third of all private credit loan commitments. When an asset class concentrates this much, a stumble by one or two giants becomes everyone’s problem.

What’s Actually Driving This?

Strip away the geography, and three threads run through almost every market.

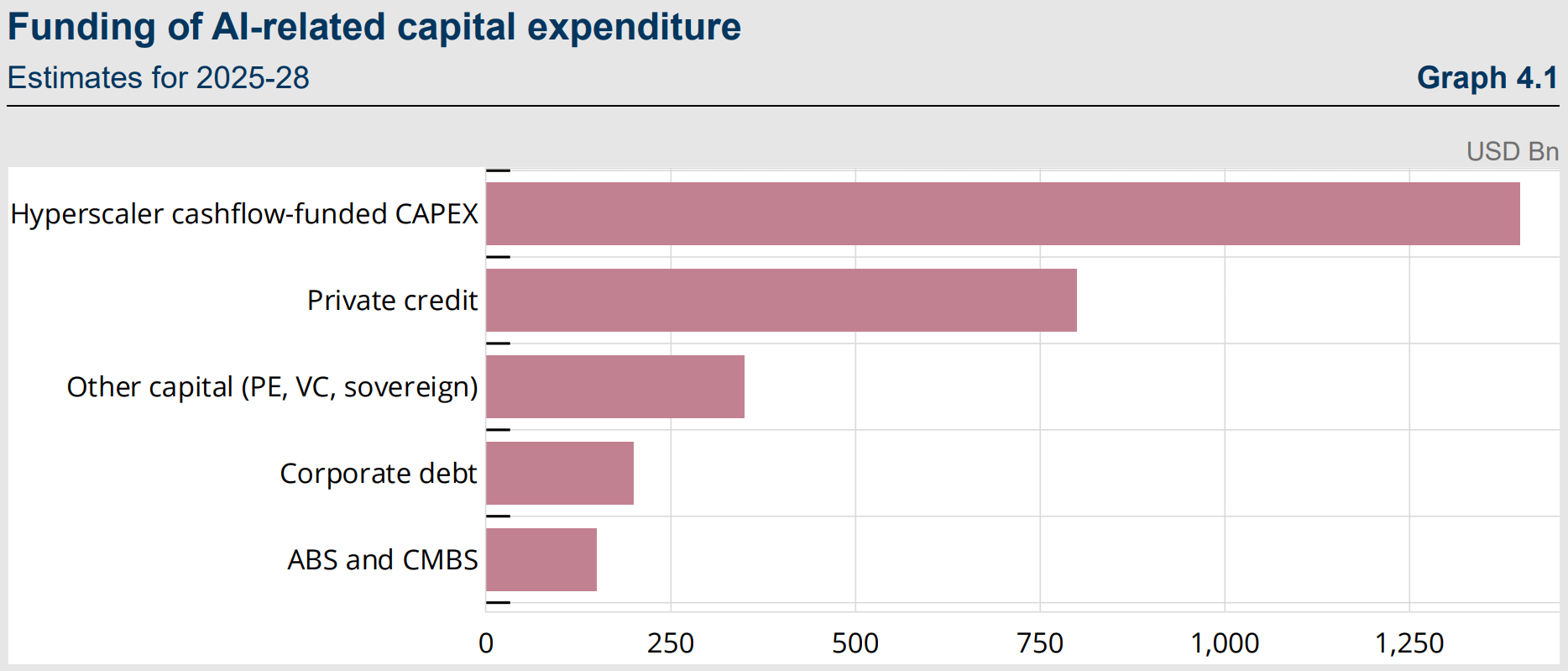

Thread one: AI is now the industry’s biggest single exposure. AI-related deals went from an average 17% share of private credit deal-flow over the previous five years to 33-34% in 2025. Private credit will need to fund roughly $800 billion of the projected $2.9 trillion in global AI infrastructure spending through 2028. That’s a huge bet on data centres, GPUs, and the assumption that AI revenue eventually catches up to AI capex. If electricity supply for data centres falls short, or AI demand doesn’t materialise as fast as projected, a large chunk of the industry’s recent growth becomes its biggest liability, almost overnight.

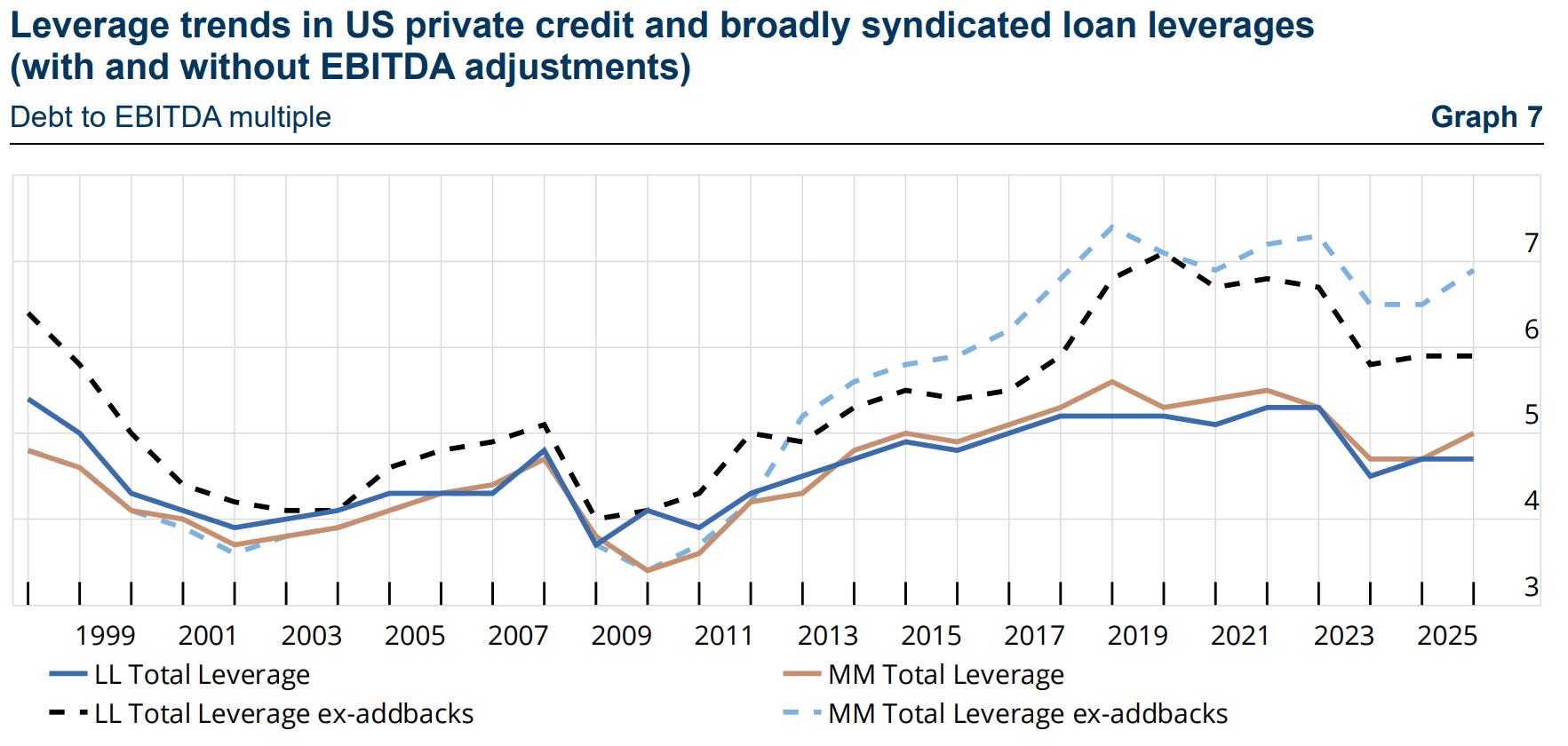

Thread two: leverage that was always higher than it looked. Typical private credit borrowers run debt-to-EBITDA ratios of 5-6x — and closer to 7x once you strip out the optimistic “adjustments” companies make to their EBITDA figures. About 6.4% of loans now carry “bad PIK” structures”, where borrowers pay interest with more debt instead of cash. More than one in ten loans held by private credit funds have already been marked down by 50% or more.

Thread three: this is the first real downturn the industry has faced at its current size. Private credit’s growth happened almost entirely during a benign period with low defaults, abundant capital, banks retreating from lending due to tighter regulation. As BofA’s Neha Khoda put it, it’s “the lowest quality asset class across our leveraged finance universe”, and US banks have lent nearly $300 billion directly to private credit providers. The FSB separately estimates direct bank exposure to private credit funds at $270-500 billion. So even if private credit itself doesn’t blow up, banks are wired into it deeply enough that they’d feel it.

And India?

Here’s where the story diverges, at least for now. India’s private credit market deployed roughly $9 billion in H1 2025, up 53% year-on-year. Total AIF commitments crossed ₹15.05 lakh crore (~$170 billion) by September 2025, and domestic funds now account for 64% of deal value. That’s a market that’s genuinely indigenising rather than relying on foreign capital.

But the banking and NBFC side tells a more cautious story, and that’s the side feeding much of this credit. India Ratings expects overall bank credit growth to land at 13-13.5% in FY26, but notes this masks a sharp slowdown in NBFC and retail lending — credit growth had already cooled from 19.4% in April 2024 to 9.9% by April 2025. NBFC AUM growth itself is projected to moderate to around 18.5% in FY26, as lenders tighten underwriting on unsecured loans.

The RBI has also moved pre-emptively. New rules effective January 2026 cap any bank’s investment in a single AIF scheme at 10% of that scheme’s corpus, explicitly to keep banking-sector exposure to private credit from quietly building up the way it has in the US. India’s private credit market is still tiny relative to its economy at about 0.6% of GDP, versus a much larger share in the US, which is precisely why regulators have room to act early rather than late.

The Takeaway

Private credit’s pitch was always simple: higher yields, in exchange for taking risks banks wouldn’t. For a decade, that trade paid off because nothing went wrong. Now something is going wrong, not catastrophically, but persistently, across the US, Europe, and the UK, and increasingly tied to one shared bet: that AI infrastructure spending will generate the cash flows needed to repay the debt funding it.

India isn’t immune to any of this. Its private credit market is growing precisely because global capital is looking for diversification, and Indian NBFCs are seeing the same underwriting caution that’s playing out everywhere else. But its smaller scale, tighter regulatory guardrails, and the RBI’s early intervention on bank-AIF exposure mean the lesson from the US and Europe (that opacity plus leverage plus concentration eventually gets tested) is one India still has time to learn from, rather than relearn the hard way.

Until next time, ReadOn!