PhysicsWallah’s Report card

Did the EdTech player pass or fail Q2 FY26?

At ReadOn, we don’t just report the markets. We help you understand what truly drives them, so your next decision isn’t just informed, it’s intelligent.

A few weeks ago, something unusual happened on Dalal Street. An edtech company delivered a quarterly report that actually looked good. This is a sector that most investors had written off as venture capital’s most expensive mistake.

PhysicsWallah, the company that went public in November 2025 amid considerable scepticism, just released its maiden earnings report as a listed entity. And it might have just changed the conversation around Indian edtech entirely.

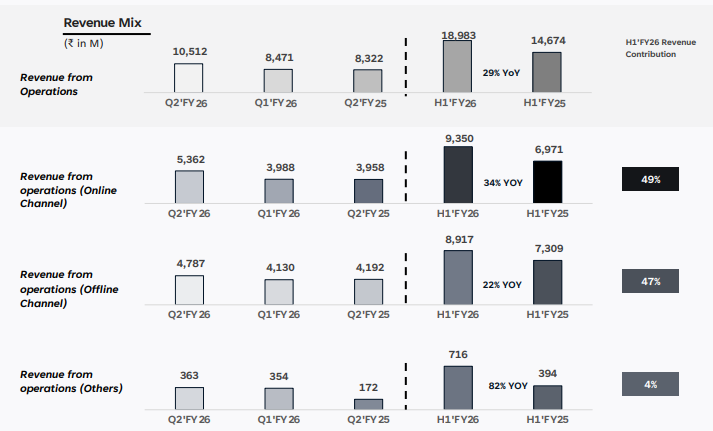

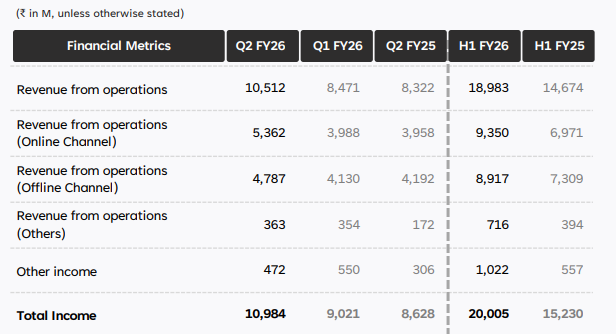

In Q2 FY26, the company posted revenue of ₹1,051 crore. This was a 26% jump from the same quarter last year. Profit after tax came in at ₹70 crore, up 70% year-on-year. The company’s operating cash flow for the first half of the fiscal year crossed ₹927 crore. That’s not venture capital money. That’s actual cash generated from teaching kids.

But wait. Isn’t this the same sector where Byju’s is drowning in lawsuits and Unacademy is a shadow of its former self? How is PhysicsWallah managing to turn a profit while its peers are fighting for survival?

The answer lies in a fundamentally different approach to building an education business.

When volume beats pricing

When most edtech companies were busy selling ₹50,000 packages to aspirational parents, PhysicsWallah went the other way. A year-long JEE or NEET preparation course on the platform costs about ₹4,000. That works out to roughly ₹10 per day — less than a cup of chai at most places.

The economics of this seem counterintuitive. How do you build a profitable business selling courses at a tenth of what competitors charge?

The secret is in volume.

In live online classes, a single teacher can teach up to a few thousand students simultaneously. Much higher than a typical classroom. The cost of that teacher gets divided across thousands of paying customers, which means the company can afford to pay faculty extremely well while still charging students a fraction of what a local tutor would cost.

This creates what management calls a “win-win-win” situation. Teachers earn more than they would at local coaching centres. Students get access to top-tier instruction for a small amount. And PhysicsWallah builds a loyal community that keeps coming back. Even after raising online course prices by about 8% this year, revenue growth exceeded 30%. This was driven entirely by volume, not pricing power.

But here’s where the story gets interesting.

The offline pivot

PhysicsWallah isn’t just an online company anymore. Almost half of its revenue now comes from physical coaching centres. That’s a dramatic shift from just two years ago, when it was almost entirely digital.

The company currently operates 314 offline centres across the country, making it one of the fastest-growing education networks in India. And unlike traditional coaching institutes that open centres based on real estate availability, PhysicsWallah uses a data-driven approach. The company tracks where its millions of online students are concentrated. When it spots a pocket of high demand, like tens of thousands of students in Patna or Indore regularly logging into the app, it knows a physical centre there would fill up quickly.

The result? About 80% of offline admissions come from students who already know the brand through online content. This keeps customer acquisition costs remarkably low and ensures that new centres hit the ground running instead of waiting years to build a reputation.

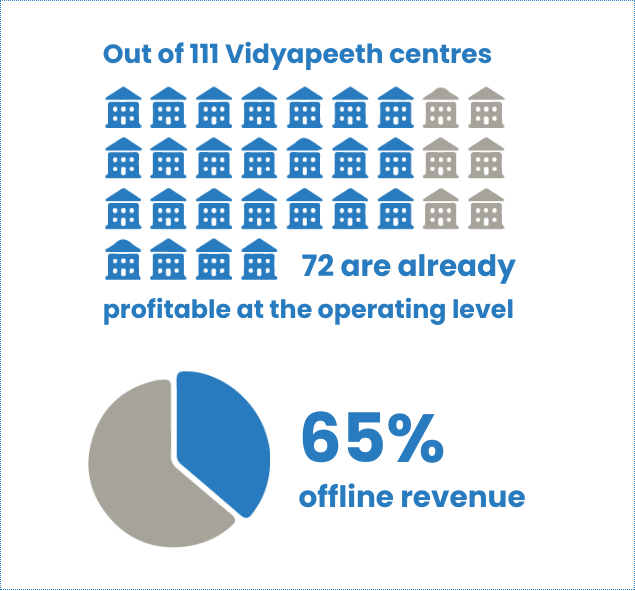

Of the 111 core Vidyapeeth centres focused on JEE and NEET preparation, 72 are already profitable at the operating level. These contribute about 65% of offline revenue. For a business that only launched physical operations three and a half years ago, that’s an impressive ramp-up. The ARPU (Average Revenue Per User) of this segment was ₹21,985 for H1FY26.

The diversification play

There’s another shift happening beneath the surface that doesn’t get enough attention.

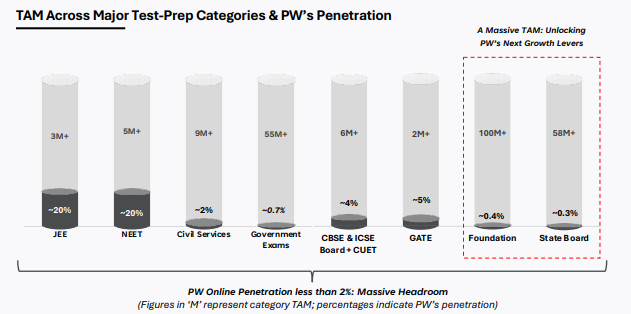

Two years ago, about half of PhysicsWallah’s students were JEE or NEET aspirants. That number has dropped to roughly 35%. The company is rapidly expanding into other exam categories like UPSC, state board exams, government job preparation, GATE, CA, and even skill-based courses.

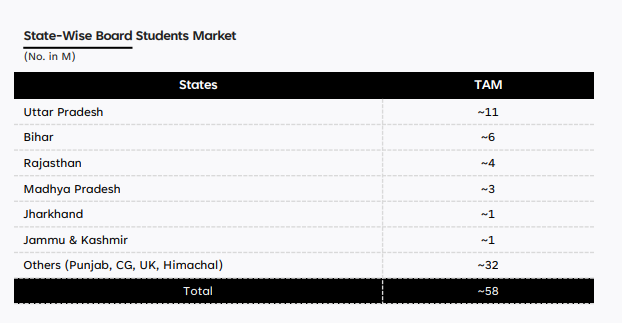

State board exam preparation has emerged as the fastest-growing segment of the online business. And the opportunity here is staggering. The Hindi-speaking states that PhysicsWallah currently serves like UP, Bihar, Rajasthan, Madhya Pradesh, Jharkhand represent about 58 million students. Local tutors for these board exams often charge ₹15,000 to ₹25,000 per year. PhysicsWallah offers similar courses at a tenth of that price.

This diversification serves two purposes. First, it reduces dependence on JEE and NEET, which gives the company access to a more diverse student base. Second, it extends the customer lifetime value. A student who joins for 9th-grade foundation courses can stay in the ecosystem through 10th boards, then JEE or NEET prep, and potentially return later for UPSC or banking exam preparation. Each individual course costs very little, but a student who stays for five or six years generates significant revenue.

The numbers that matter

Let’s talk about the metrics that should catch an investor’s eye.

The PW app sees over 35 lakh daily active users, with each student spending an average of 103 minutes per day on the platform. That’s nearly two hours of daily engagement. The DAU-to-MAU ratio (daily active users as a percentage of monthly active users) is among the highest for any consumer app in India, according to management.

On the financial side, adjusted EBITDA margins expanded from 23.5% to 25.7% year-on-year in Q2. Marketing expenses, which have killed many edtech startups, are up by 1.6% as a percentage of revenue in this quarter. But for the full year, they expect it to be around 8-9%. Down from 9.6% last year. The company’s treasury stands at ₹2,552 crore (excluding IPO proceeds), giving it ample runway for expansion.

And Q3 is shaping up to be even stronger. The test-prep business follows academic cycles, and Q3 is historically the peak revenue quarter. Management has indicated that EBITDA margins could cross 20% in the current quarter.

The road ahead

PhysicsWallah’s success raises a big question for Indian education. Was the edtech bust really about a flawed model, or just flawed execution?

According to PhysicWallah’s RHP, the test preparation market in India is worth about ₹1-1.1 lakh crore today. PhysicsWallah’s primary battlefield, the online segment, is currently worth around ₹14,000 crore but is projected to grow at 29% annually to reach ₹50,000-55,000 crore by 2030. That’s a four-fold increase in five years. And there’s more. Even within JEE and NEET, online penetration remains below 2%. PhysicsWallah has roughly 20% market share in these categories, yet claims it’s barely scratched the surface.

The company has signalled it won’t chase growth by hiking prices. “ARPU improvement has scope,” founder Alakh Pandey said on the earnings call, “but not at a dilution of the vision to make education accessible for the entire country.”

That’s an unusual thing to hear from a public company CEO under quarterly earnings pressure. But it might be exactly why PhysicsWallah has succeeded where others failed. By keeping courses affordable, it expanded the market instead of fighting for a larger slice of an existing pie. By building community through free YouTube content, it created an organic acquisition engine that doesn’t require burning cash on advertising. By using online data to guide offline expansion, it avoided the empty-classroom problem that plagues traditional coaching centres.

There are risks, of course. Teacher attrition runs at 25-30% annually, and faculty departures can take students with them. The regulatory environment for competitive exams is unpredictable. Offline expansion is capital-intensive, and new centres take nearly two years to break even.

But for now, PhysicsWallah has done something no Indian edtech company has managed before. It has shown that education can be scaled profitably without abandoning the students who can’t afford premium prices.

Only time will tell if this is a turnaround that will last, or vanish.

Until then, ReadOn!