Personal Finance 101

Personal Finance 101

Managing your personal finances is an art. Can't master this skill yet? Read on, we're here for you :)

One of the many skills that we were not taught in school is the art of managing our money: be it for day to day expenses, planning for retirement or any other goal.

Because of our lack of adequate knowledge, we often let emotions affect our financial decisions (to know more about how emotions affect our decision making, check out this video we made).

“I just got a promotion; I deserve an expensive car!”

Aspiring for an expensive car is cool, but could it wipe away the increment that we earned? Is it a great financial decision?

If we were to keep our lifestyles in check and not inflate it as our income rises, we could lead a comfortable and secure life ahead. The future is uncertain. Nobody expected a pandemic to happen in 2020.

Rich people are rich because they make smart decisions about their money. They don’t work for money, money works for them.

As Warren Buffett rightly said, “Do not save what is left after spending, but spend what is left after saving”. Save, then spend.

Identifying a problem is the first step in solving it. Now that we have understood the problem, let’s see how we can solve it.

Your Path towards Financial Freedom

Managing your finances is no rocket science.

Below are four things that you could do every month right from the time you receive your pay-check.

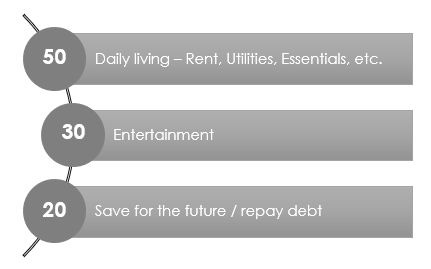

Create a Realistic Budget – The 50/30/20 rule

The best way to stick to your budget is to make one. While most of us realise the importance of making a budget, we fail to do so because we don't know how. One thing that really helped me create my budget was the 50/30/20 rule:

A monthly budget lists how much income you have coming in (inflow) compared to what's going out each month (outflow).

When you're about to make a wasteful expenditure, a budget will make you stop and think about the purchase. You realize that by spending money in one area, you won't have enough to spend or save elsewhere (opportunity cost).

Simply put, “A budget is telling your money where to go instead of wondering where it went” - Dave Ramsey.

When you create a budget, you begin to see a clear picture of how much money you have. You can identify your spending, and how much—if any—is left over.

Ideally, you'll have a surplus leftover, which you can use to save for:

Plan Your Expenses

“Too many people spend money they earned, to buy things they don’t want, to impress people that they don’t like.” – Will Rogers

After you've successfully created a basic budget, you'll have a much better understanding of where your money goes and where you can trim expenses. When I started creating budgets I realized I’m spending a big chunk of money on eating out and some subscription services / memberships I don’t even use. I realised I could use that money to increase my monthly investments.

Manage Your Debt

Your “Personal Debt” is how much money you owe to other people, banks, credit card companies, etc.

Having personal debt is not inherently a bad thing, but getting too much that you are unable to pay back in a timely manner is a huge problem (as interest on such borrowings accumulate).

Whenever you borrow money, ask yourself two basic questions:

Am I going to channelize the money from this debt towards buying assets, personal growth or expenses?

Will I be able to repay the debt along with the interest without failure?

Having said that, at some point, you may have debt - whether that is in the form of house loans, credit cards, etc. You have to learn how to manage it from day one. Understand how your debt works, what the interest rates are, and how to pay it off faster. After all, life is better when you have no debt.

Invest, Invest, INVEST!

One of the most important things in personal finance is to channelize your savings towards investments. Now you may wonder what’s the difference between saving and investing as these two words are often used interchangeably.

Hell, people use the word saving more than investing.

Saving is setting aside money you don’t spend now for emergencies or for a future purchase (20% as mentioned earlier). It’s money you want to be able to access quickly, with little or no risk.

Investing, on the other hand, is buying assets such as stocks, bonds, mutual funds or real estate with the expectation that they will make money for you while you sleep.

Following these four steps will take you closer to becoming a master of your money, instead of being a slave to it. It will take you one step closer to your financial freedom.

And, we will make sure you stay on your path to financial independence :)

Thousands of readers get our daily updates directly on WhatsApp! 👇 Join now!