LIC: Saving the Government Since 1956

What is insurance? How do insurance companies make money? And, how big is our favourite life insurance company?

As a kid, I remember feeling intrigued by advertisements like “Zindagi k sath bhi, zindagi k baad bhi.”

Once I asked my dad about how life insurance works. I couldn’t understand their cryptic talk of ‘pay Rs. 5,000 premium every year for 40 years, and get Rs. 1 crore when you die.’

My dad just smiled and said, “You are too young to worry about all this. Go, play with your sister.”

My 12-YO know-it-all self thought - “Why do I need money after I die? And why are they giving so much, when I have paid only Rs. 2,00,000 during my lifetime? How stupid are these companies? They don’t make money. Pakka.”

Turns out, I was stupid.

Decoding Insurance

“If ‘risk’ is like a lump of smouldering coal that may spark a fire at any moment, insurance is civilization's fire extinguisher.” - Someone, somewhere.

There are a lot of things one can ‘insure.’ Fire, health, an important person (keyman) for a company, throat (for singers), face, etc.

Whatever needs protection can and will be protected. Derisked. Cushioned.

But, why insure your life? Life doesn’t stop when we depart, does it? It goes on. And we live on, in the hearts of people that love us, no?

While that is a super romantic and novel thing to believe, there’s also a practical angle to consider.

Say someone who is the sole wage earner in a family passes away.

Untimely.

Without adequate savings.

How would the family survive such a catastrophe? Also, this is something that could happen to any family, right?

Hence, it makes sense to cover this risk. But how?

Catastrophe doesn’t strike at once for all families in usual circumstances.

So, what if all families could agree upon, from an early stage, to pay some money separately to a ‘protector’? And, only those who were unfortunate would get a predetermined amount paid by this ‘protector’?

Let’s all suffer a little so that no one suffers a lot?

In the times of mafia-lords, the ‘Family’ took care of the expenses of those deceased. Insurance companies do exactly that.

“Zindagi k sath bhi, zindagi k baad bhi.”

You pay a regular premium for the benefit of getting covered if you die an untimely death. It’s basically protection money.

And, instead of small groups managing the money, there are insurance companies that take care of this. At a national scale.

As per a report by Bloomberg Quint, 75% of India’s population does not have life insurance cover (that is more than the entire population of Europe). Just saying.

The next logical question is: “How does an insurance company make money?”

Insurance companies make money by betting on risk - the risk that you won’t die before your time.

It is all a game of probability. The more the number of people signing up for a policy, the wider the spread of the risk (everyone won’t drop dead at the same time - unless it is a natural calamity, which the insurance policies comfortably don’t cover).

A profitable insurance company collects more cash (premium) than it pays out.

It writes a lot of insurance contracts with a lot of customers who pay them a premium to get covered.

Now, the insurance company gets a lot of money every month, but payouts are not that high. So, with the excess cash available, what does it do?

It invests that cash (in stock markets, bonds of government and companies, and sometimes in start-ups too).

From this excess cash invested, it gets an income. Income from Investments.

Thus, we arrive at two major sources of income for an insurance company:

Underwriting premium that you pay monthly, quarterly, annually (reduced by the amount it pays out on claims)

Income that it generates from its investments

Example - Let’s say LIC earned Rs.10,000 from the premiums paid by the customers for their policies in a year. Also, the company paid Rs. 6,000 to settle claims of the deceased in the same year. This means that on the underwriting side, LIC earned a profit of Rs.4,000 (10,000-6,000).

Make no mistake, the entire underwriting mechanism ensures that a potential customer actually pays enough to cover the risk of you (or me, or anyone else) dying (they use consumer data like health, age, annual income, gender, credit history, etc).

The math always works in their favour (our actuarial science friends make sure of that).

Life Insurance Corporation

Now that we understand how insurance companies make money, let’s dive deeper into that one company that’s synonymous with insurance in India.

So much so, that my dad doesn’t say “Buy an insurance policy.”

He says, “LIC le le beta.”

LIC is an Indian state-owned insurance group and investment corporation founded on September 1, 1956, and owned by the Government of India.

LIC's mission is “to ensure and enhance the quality of life of people through financial security by providing products and services of aspired attributes with competitive returns and by rendering resources for economic development.”

And LIC doesn’t just enhance our 'quality of life'.

Every once in a while, it saves the Government's neck too.

The Dark Knight.

LIC is the government's silent, watchful protector.

It is not the corporation that the government deserves, but the one that the government needs.

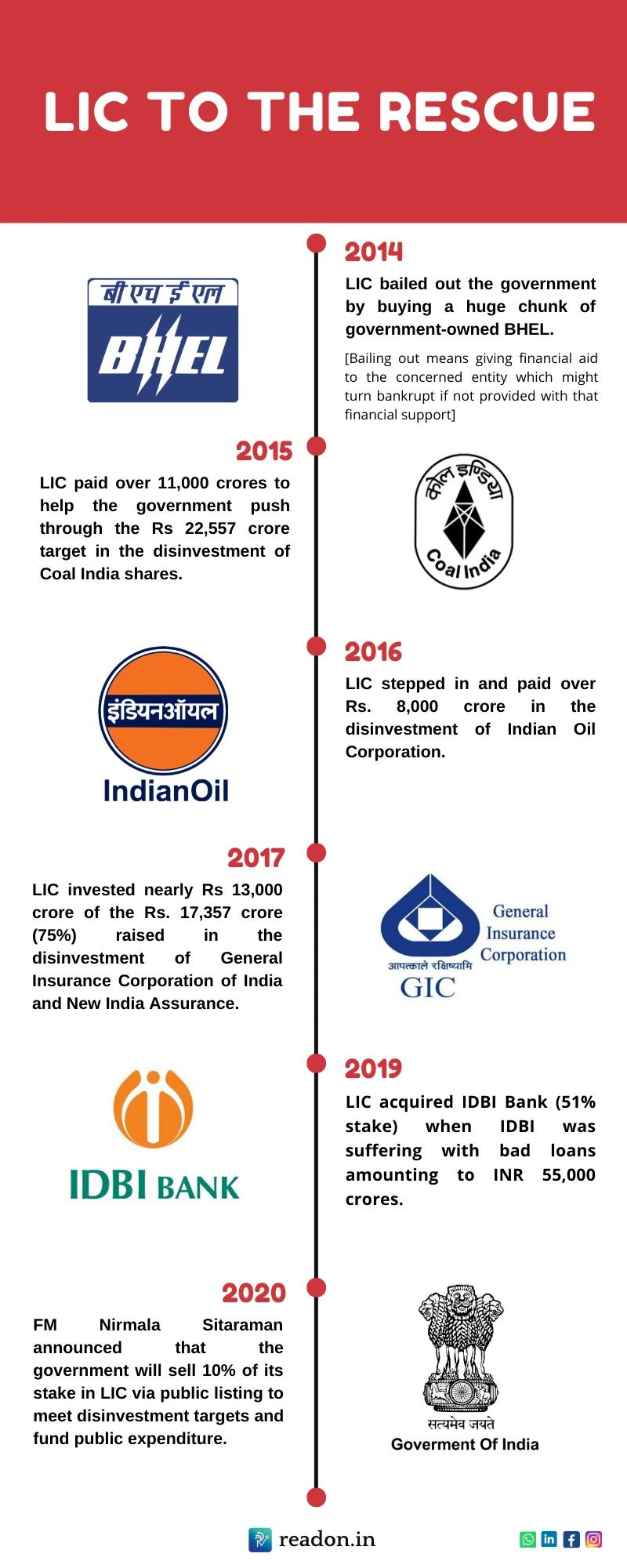

Time and again, LIC has been called upon by the government to save an ailing bank or meet a disinvestment target (disinvestment means selling off shares in a company that the government owns to raise funds that can be used to finance its expenses):

LIC saves the day. Always.

"LIC: Government ke sath bhi, government ke baad bhi."

Obviously, when something is so big, it is bound to attract some controversy.

In April 2017, a Public Interest Litigation (PIL) was filed against LIC regarding its investment in tobacco firms by Tata Trusts and the doctors of Tata Memorial Hospital.

[PIL is basically a legal action taken by a person for the benefit of society at large]

The PIL stated that it makes no sense for the government, which is tackling health issues arising out of tobacco consumption, to directly or indirectly hold stakes in ITC or any tobacco companies.

LIC (with five Insurance Companies and Specified Undertaking of the Unit Trust of India or SUUTI), holds a 32% stake in ITC Ltd.

On one hand, they protect you in case of an untimely death. On the other, they earn from selling a product that may cause you to die untimely.

Hypocrisy much?

LIC defended itself by highlighting that their main aim is to see that returns are maximized with minimum risk and that it adheres to all its underlying policies and acts.

Right (eye-roll).

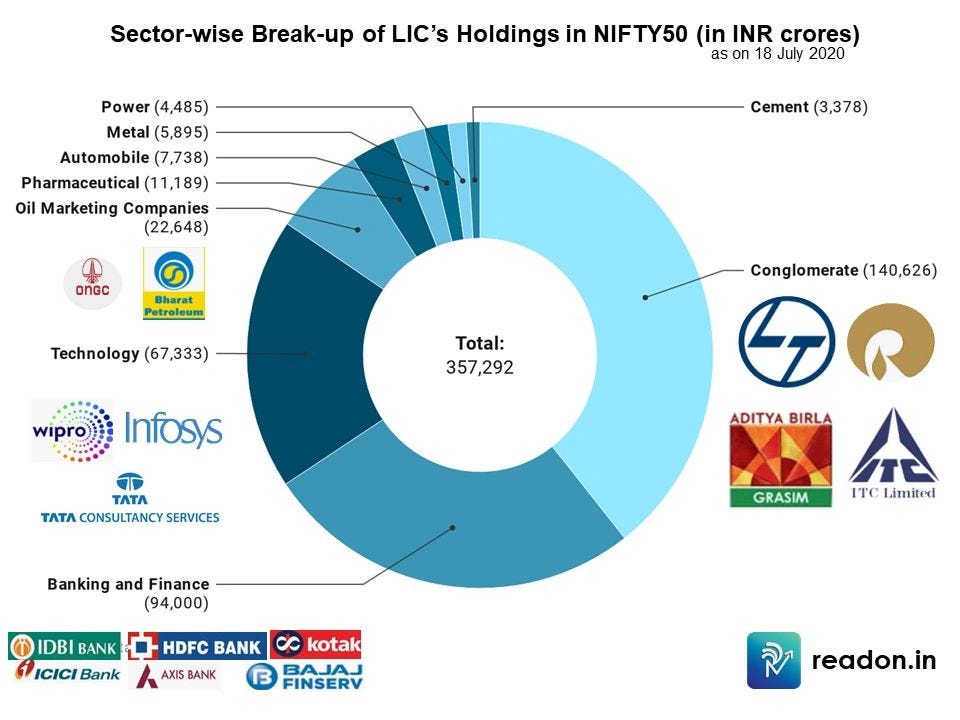

Now, LIC sounds like this huge company. How big is it, precisely?

Of the 50 companies that make up the Nifty50 index, LIC owns shares in 26. The current market value (as on 18 July 2020) of LIC's investments in these companies amounts to INR 3.57 lakh crores.

That's huge.

Just by the virtue of this valuation, it would become the 5th largest company on the bourses:

Here's a sector-wise break up of its holding in Nifty 50 companies:

It is so big that it has its own Act, LIC Act 1956. The Act contains certain preferential provisions for payment of dividend to government and sovereign guarantee.

Given the current pressure on the government to spend more and boost economic activity in the country, it is looking to sell off some stake in its crown jewel.

Business Today expects LIC to be valued at around INR 13-15L crores (which will make it the most valuable company in India, beating Reliance Industries Limited, which is currently valued at INR 12L crores). A 10% stake sale, therefore, will give the government enough fodder to feed the dying economy.

To sum it up, LIC is the prodigal kid that parents (the government) can rely on. It also takes care of the siblings (banks, other government companies) and doesn’t let anyone fail.

And now, it is time for the kid to graduate (get listed).

After the public issue, will the incoming shareholders raise their voice against draining out of LIC’s resources by the government? Will amendments be made in the Act that unduly favours the government? Or will they be side-stepped, and things will stay the same?

Only time will tell.

Till then, be a good kid, and help out your parents and siblings (I will try too :P).

Take care. ReadOn.

Thousands of readers get our daily updates directly on WhatsApp! 👇 Join now!

Behind The Scenes

Mukund and Vedant, your researchers for this piece, cried tears of blood while reading LIC's annual report, which is primarily in Hindi. There are English subtitles to the document, but the readability is super pathetic. Salute to their relentless efforts to bring this piece out for you!