India’s Missing Trillion

The name's Bonds. Corporate Bonds. And the Indian ones are struggling.

At ReadOn, we don’t just report the markets. We help you understand what truly drives them, so your next decision isn’t just informed, it’s intelligent.

When US forces struck Iran on February 28, 2026, investors reached for the old playbook. Wars mean fear. Fear means safe havens. Safe havens mean bonds. Only it didn’t work that way.

The 10-year US Treasury yield, which briefly dipped to 3.96% on reflex flight-to-safety instinct, climbed back to 4.26% within the first week of fighting. Once Iran’s threats to the Strait of Hormuz made oil disruption risks real, inflation fears overtook growth concerns, and bonds stopped being the refuge they once were. Inside the $50 trillion global bond market, equities and bonds fell together. The safe-haven halo flickered.

And yet, emerging market (EM) debt kept winning. Hard currency EM sovereign bonds returned 2.58% year-to-date through May 2026. These are bonds in emerging or developing markets that are denominated in globally stable currencies like the US dollar or the Euro. This eliminates the risks associated with the instability of the local currency of the EM. Speaking of, local currency EM bonds delivered 1.32%. Combined net inflows into hard and local currency EM bonds hit $3.3 billion in May alone, not despite geopolitical turbulence, but alongside it.

High real yields, credible monetary frameworks, and an index-driven passive flow story kept the bid alive. In a world where traditional safe havens were misbehaving, global investors found EM bonds, and they stayed.

India, one of the fastest-growing large economies in the EM universe, should be absorbing a meaningful chunk of this capital. The appetite is there. But between global interest and India’s ability to capture it sits a structural gap. India has a corporate bond market so shallow, so concentrated, and so illiquid that it struggles to serve even domestic needs. Let alone attract serious foreign money at scale.

Why is India’s bond market broken? Let’s find out.

A Market That Barely Exists

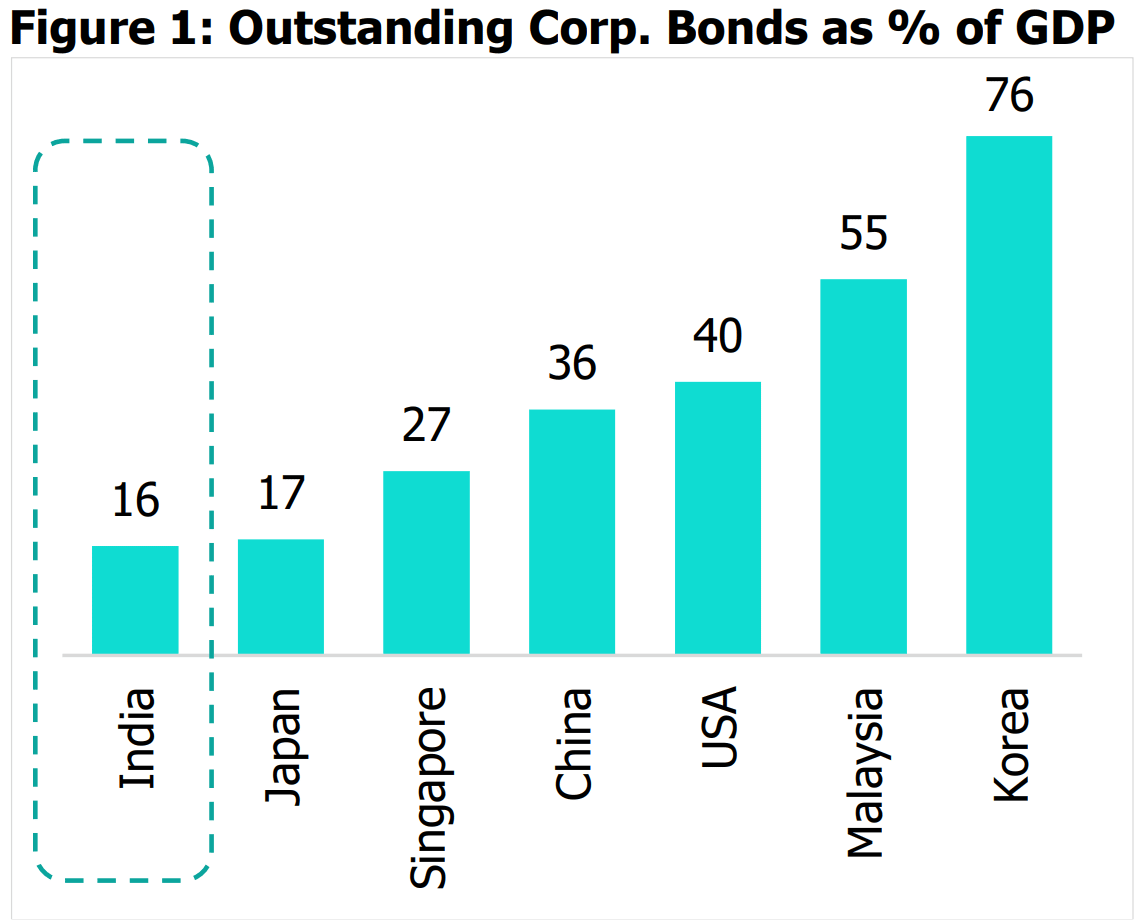

India’s corporate bond market is approximately 16% of GDP, against 36% in China and 40% in the United States. Outstanding corporate bonds total roughly ₹59 lakh crore, which sounds large until you realize corporate debt accounts for barely a fifth of India’s total debt market. The rest is government securities, or the bond market equivalent of a household that only lends to itself.

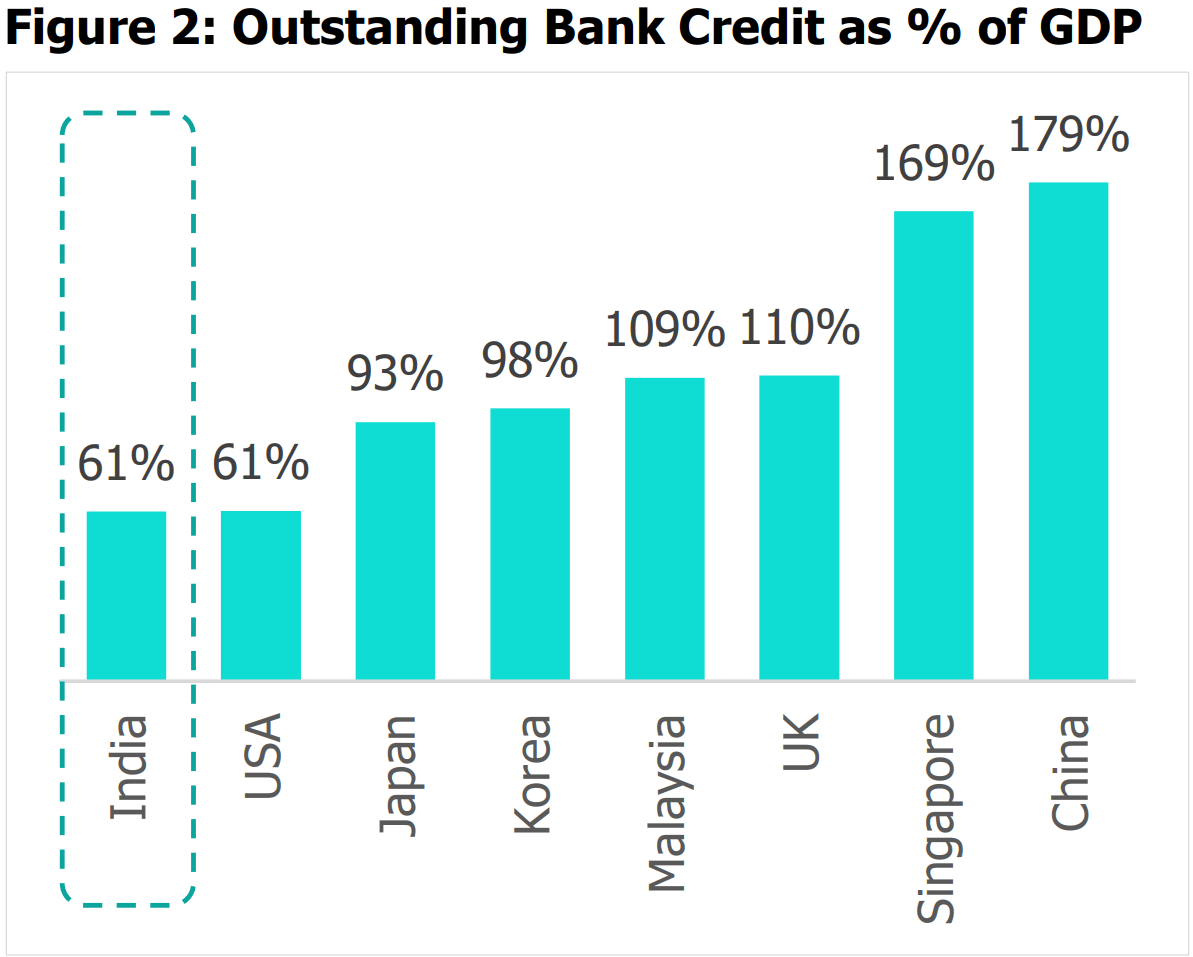

The bank credit picture doesn’t help. India’s bank credit-to-GDP ratio stands at 61%, against Japan’s 93%, Korea’s 98%, and China’s 179%. India is simultaneously under-banked and under-bonded. Banks are not filling the gap that bond markets haven’t. Growth capital for infrastructure, technology, and small businesses has limited formal pathways to flow through.

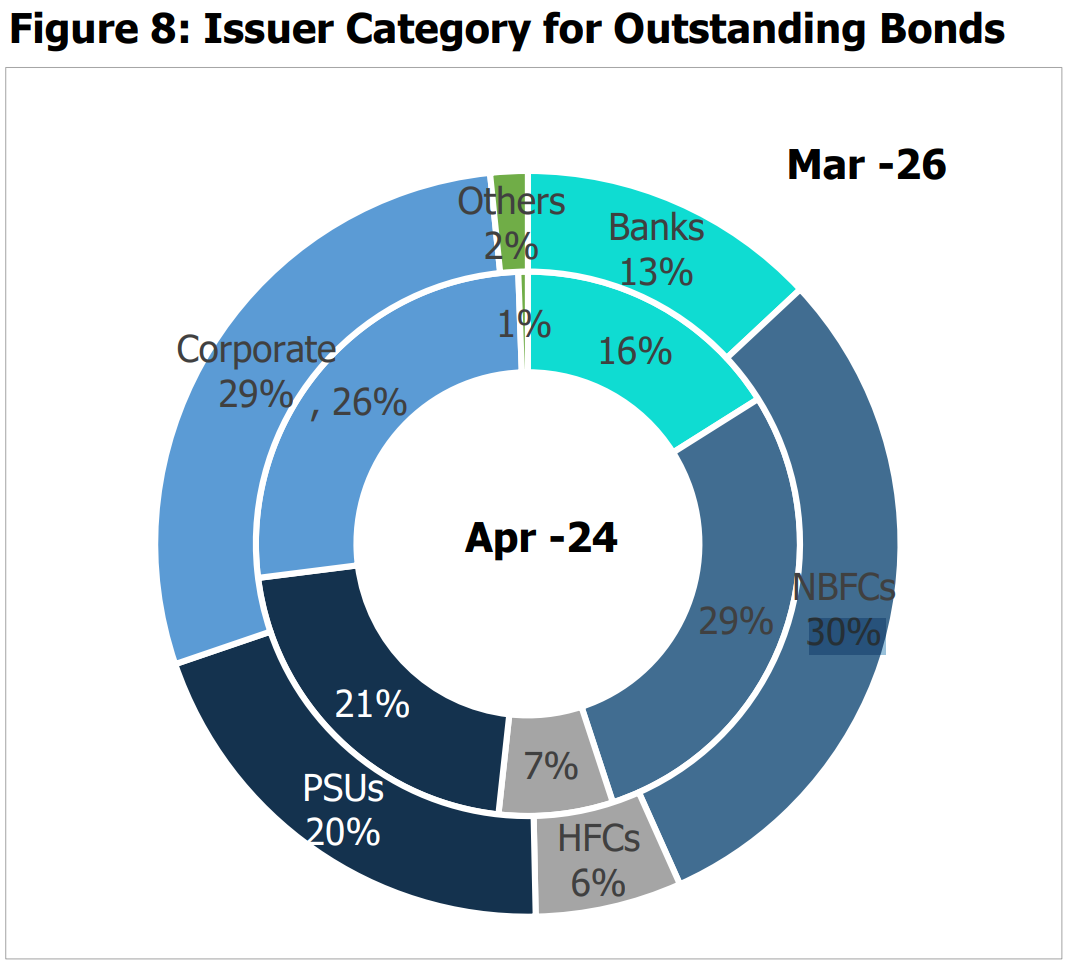

Inside the corporate bond market, the concentration is also a problem. NBFCs account for 30% of outstanding issuances, private corporates 27%, and PSUs 20%. Startups, mid-market manufacturers, infrastructure developers, or the engine rooms of India’s next growth phase are largely absent.

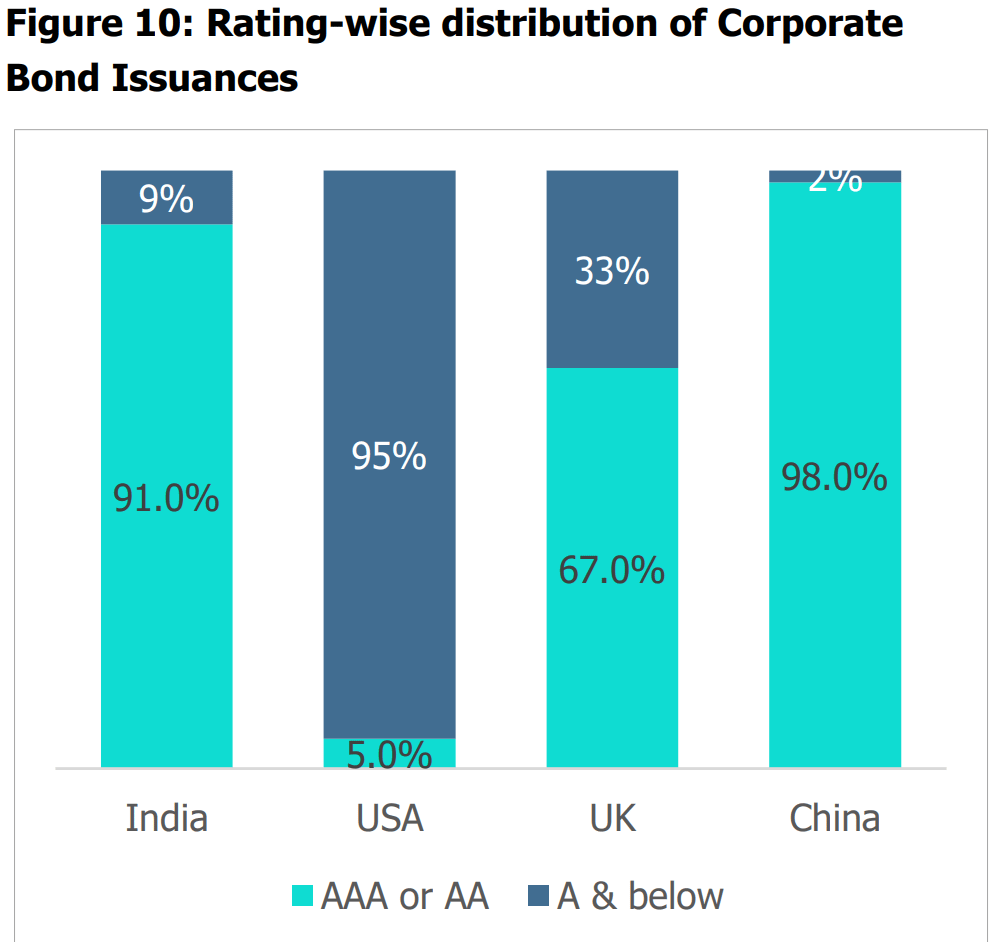

The rating distribution tells the same story: over 85% of issuances carry AAA or AA ratings, because insurance companies and pension funds are mandated to stay within that narrow band. Everything below AA goes essentially unfunded through public debt markets. Meaning an entire tier of creditworthy businesses is cut off from long-term capital.

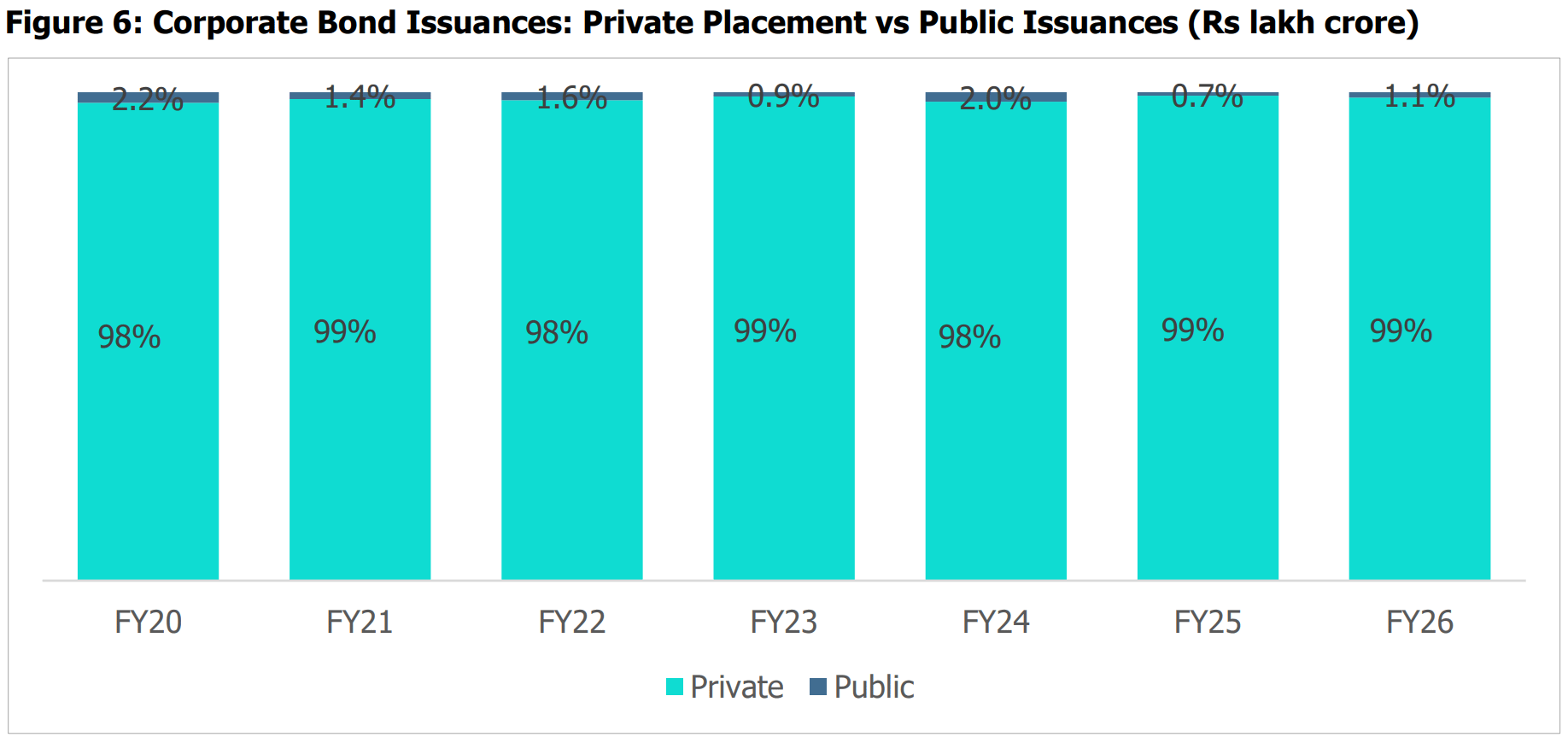

Private placements account for roughly 99% of issuances, locking out retail investors and smaller institutions almost entirely. The secondary market reflects this neglect. India’s corporate bond average daily turnover as a share of outstanding stock is 0.2%, compared to 4.7% in the US and 2.4% in the UK. What little India has built is hard to trade and costly to hold.

The FPI Puzzle

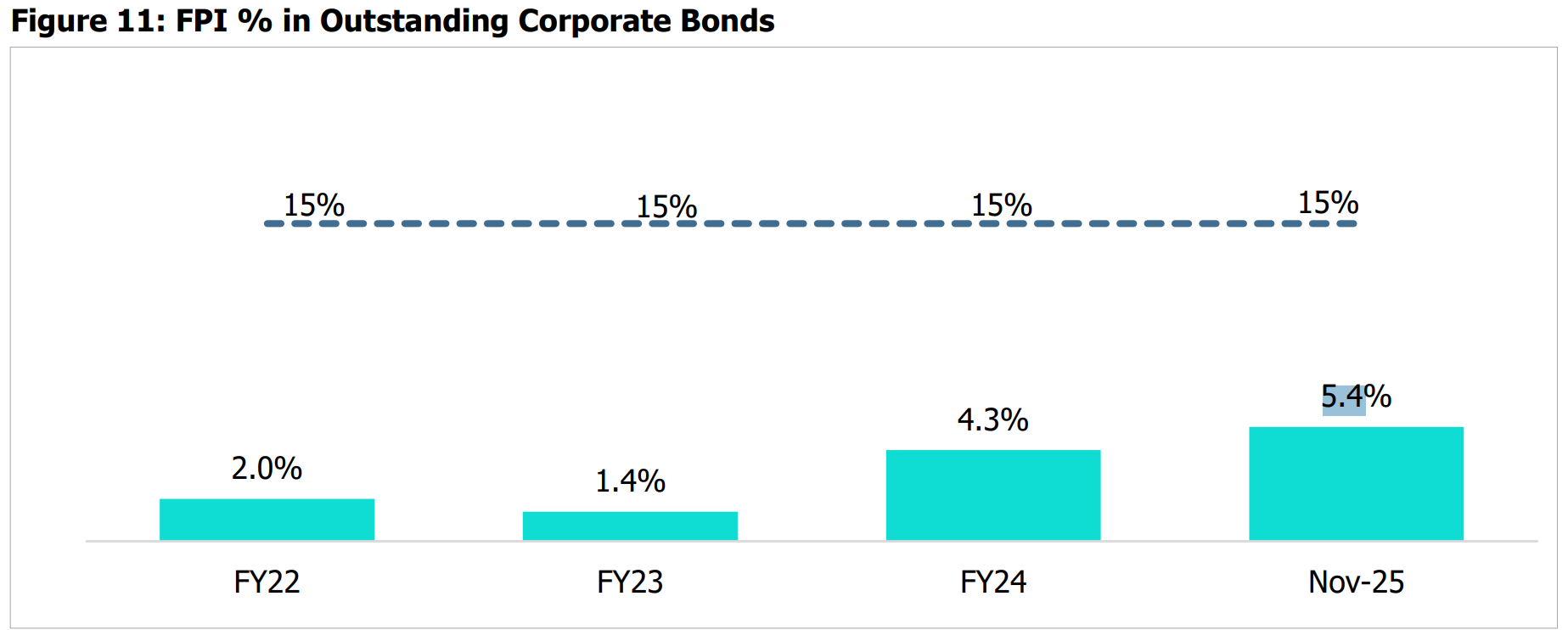

Foreign portfolio investors are permitted to hold up to 15% of India’s outstanding corporate bonds. Today, they hold just 5.4%. That gap of roughly 10 percentage points against a permissible ceiling represents tens of thousands of crores in latent foreign capital.

The regulatory conditions for change are building. In May 2025, the RBI removed the 30% concentration limit for FPIs in corporate bonds, improving portfolio flexibility. Indian government securities now sit inside JP Morgan’s GBI-EM Global Diversified Index, catalysing passive inflows exceeding $25 billion from foreign institutional investors. High real yields remain a compelling draw. The GBI-EM GD Index yield stood at 6.19% as of May 2026, keeping India firmly on the radar of any global allocator hunting for real yield.

But there’s an important distinction. Most of this FPI interest flows into government paper, or G-secs. Translating it into corporate bond demand is a different, harder problem. A foreign investor attracted to Indian rates can access a liquid, index-tracked G-sec with minimal friction. The corporate bond market offers none of that. Negligible secondary trading, complex tax treatment, and thin liquidity are hard sells. Until those change, the FPI gap in corporate bonds will stay exactly where it is.

Four Fixes That Actually Matter

India’s bond market reform agenda is not a mystery. The tools are known. What’s missing is the follow-through.

Tax rationalisation: India’s TDS framework was built for a physical trading world. In a digital ecosystem where money flows are trackable in real time, the current system creates friction that punishes smaller investors. Reducing TDS burden, enabling pre-filled tax returns for interest income, and removing adverse taxation on debt holdings would meaningfully lower the entry barrier for retail participation.

Secondary market liquidity: A bond market is only as useful as it is tradeable. Market-making incentives like lowering the cost of holding bonds in inventory would help institutional players transact more freely. Bond derivatives and interest rate swaps give market makers the tools to hedge price risk, making two-way markets viable. Today’s illiquidity premium in Indian corporate bonds reflects structural dysfunction, not credit risk. That’s a solvable problem.

Broadening the issuer base: The Economic Survey 2025-26 estimates the corporate bond market could reach ₹100-120 trillion by 2030, but getting there requires SMEs and infrastructure entities to actually access the market. Partial credit enhancements, streamlined SPV structures, and relaxed listing obligations for pure debt issuers are the mechanisms. Right now, the runway exists only for the very large and the very highly rated.

Unlocking the A-rated segment: This is the most underappreciated opportunity in Indian fixed income. A-rated bonds yield 280-330 basis points more than comparable AAA paper. CARE Ratings has recorded zero defaults in the single-A category. The credit risk is low; the yield premium is not. Allowing insurance and pension funds to put even 5-10% of their portfolios into A-rated paper would unlock a new segment that is currently overpriced purely because of artificial demand constraints.

The Takeaway

EM currencies are diverging sharply in 2026, with domestic policy credibility increasingly the differentiator between winners and laggards. US trade policy is redrawing capital flow maps. Global money is becoming more selective, not less. Countries that can finance their own growth through deep, liquid, accessible domestic markets are better positioned than those dependent on external goodwill.

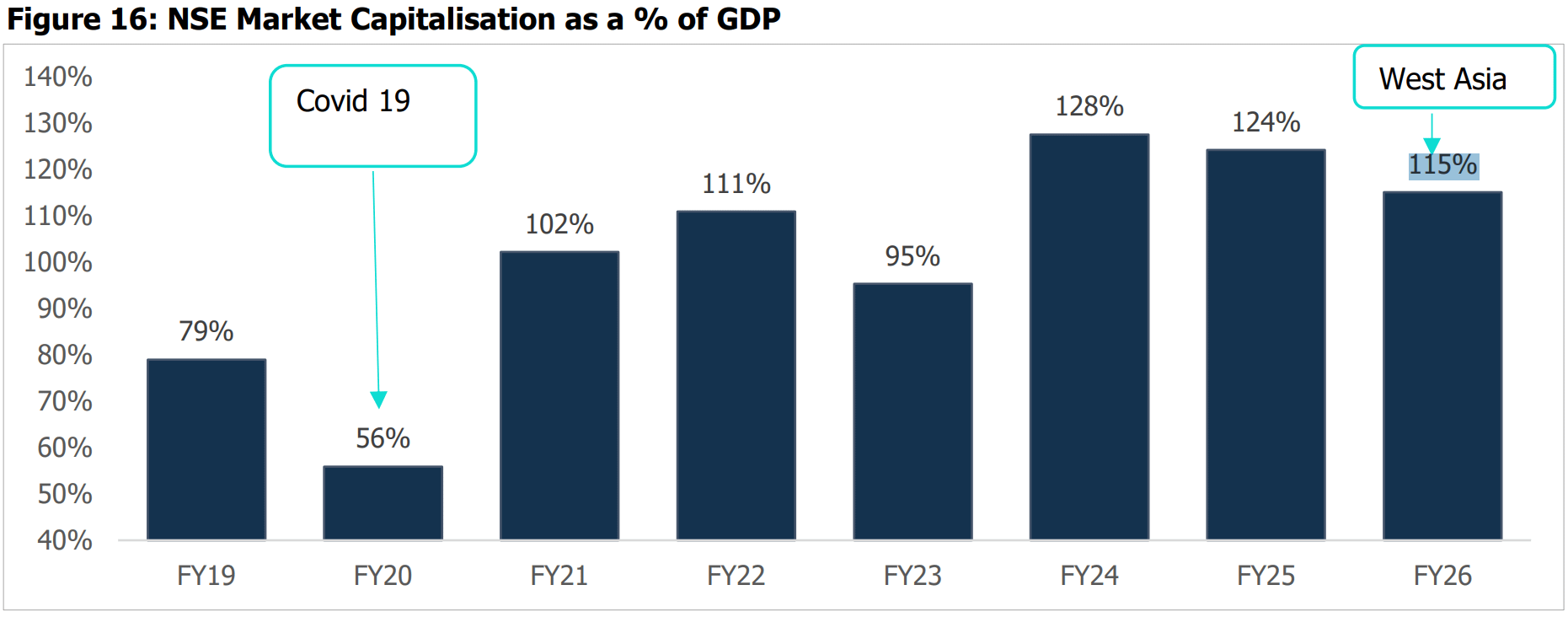

India’s equity market now sits at over 115% of GDP. That shows what sustained policy focus can do for a capital market. The corporate bond market, stuck at 16%, is the unfinished half of that story.

A well-functioning corporate bond market reduces India’s dependence on volatile FPI equity flows and an already stretched banking system. It gives India’s best companies, not just the AAA-rated giants, a genuine path to long-term capital. It builds a domestic funding base that withstands geopolitical turbulence better than any alternative.

For a country trying to finance its own future at scale, that kind of resilience is essential. And right now, it’s missing.

Until the resilience is built, ReadOn!