India’s Missing Small Change

India needs change, and this is not a philosophical demand!

At ReadOn, we don’t just report the markets. We help you understand what truly drives them, so your next decision isn’t just informed, it’s intelligent.

Walk into any kirana store in India, hand over a ₹500 note for a ₹30 packet of biscuits, and brace yourself. The shopkeeper will sigh, check all three drawers under the counter, send a kid to the neighbouring stall, and eventually shrug: “Chhutta nahi hai.” No change, neither in the shopkeeper’s drawer, nor in this growing problem. It is one of the most universal micro-frustrations of Indian daily life.

But this problem is not accidental. The small notes are actually disappearing, and according to a new report by SBI Research, this is less a supply failure and more a structural shift in how India transacts. One that a Harvard economist once said couldn’t easily be done. And yet, here we are.

What Is Going On?

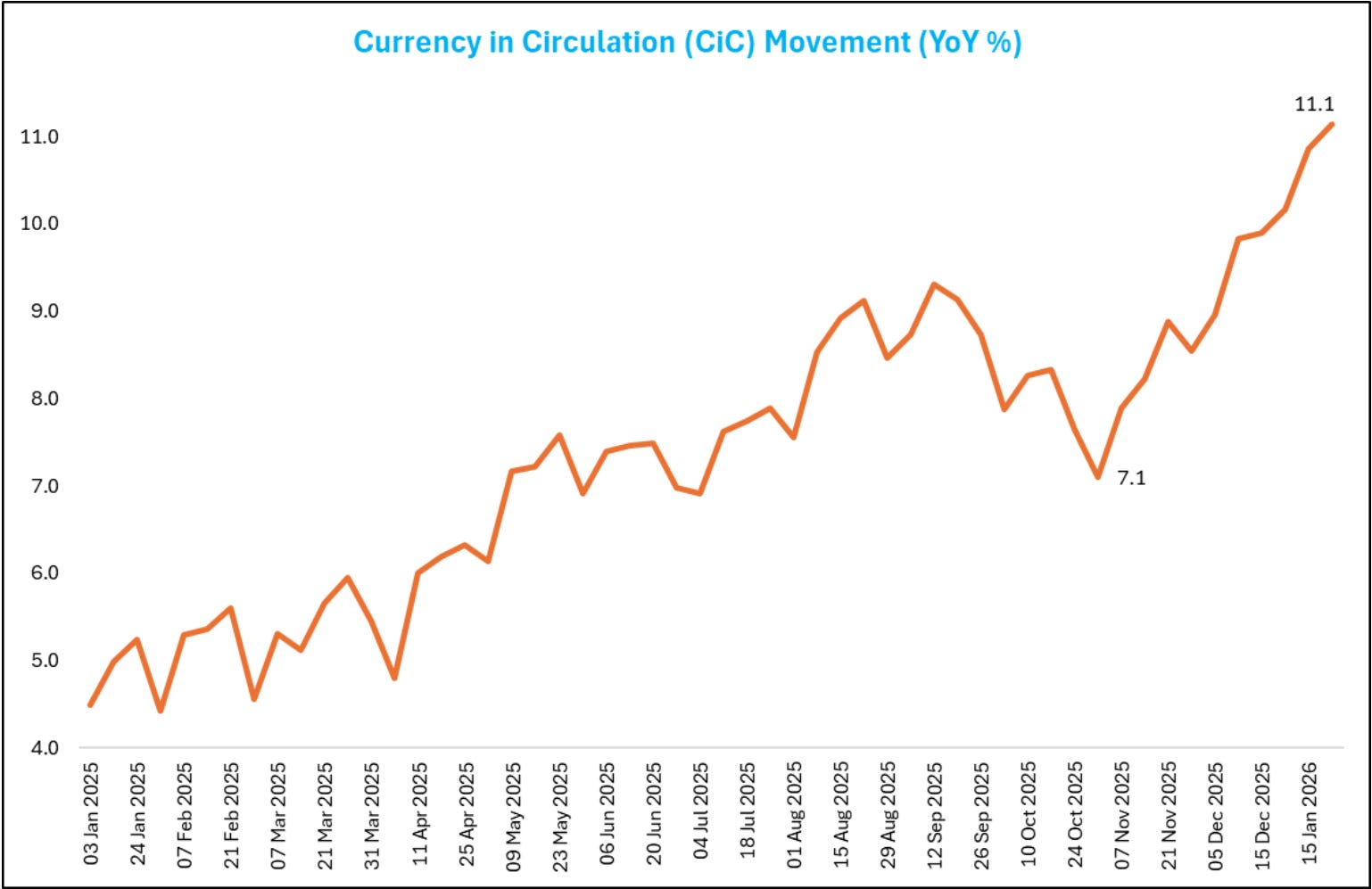

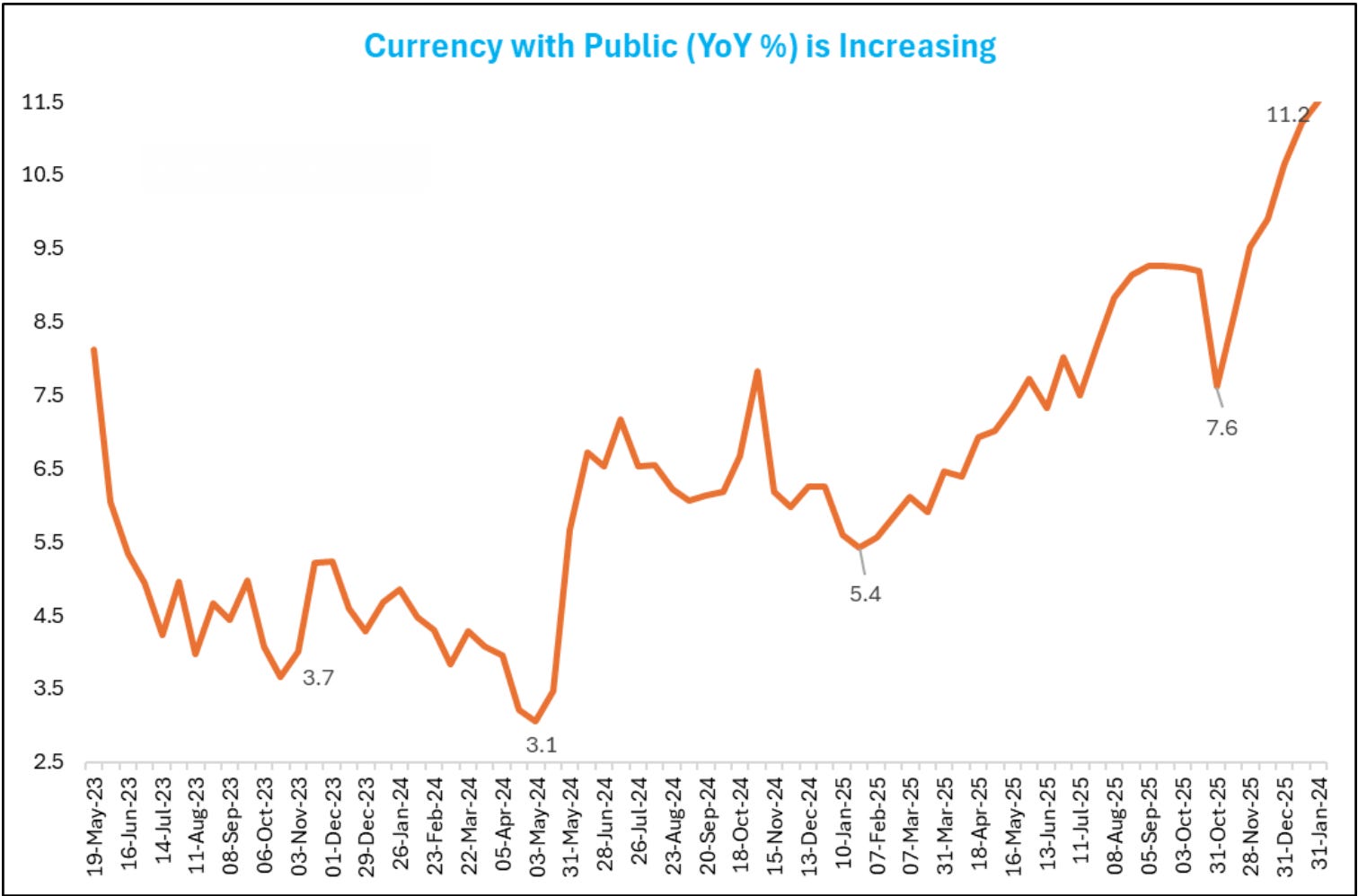

India’s total currency in circulation (CiC) hit an all-time high of approximately ₹40 lakh crore in January 2026. This was an 11.1% YoY growth, and more than double the 5.3% growth recorded the previous year. The currency sitting directly in the hands of the public, called Currency with Public, is ₹39 lakh crore and growing just as fast at 11.5% YoY.

So cash is everywhere. More cash than ever before.

And yet, India’s cash-to-GDP ratio has fallen steadily from 14.4% in FY21 to 11% in FY26. Meanwhile, UPI transactions touched an all-time high of ₹28.3 lakh crore in a single month. To put that in perspective, the entire stock of currency in the economy is ₹40 lakh crore, and UPI processes 70% of that amount every single month.

So there’s more cash in absolute terms. Less cash relative to the size of the economy. And a digital payment system that is processing staggering volumes alongside it.

Now the real question is…

How Did We Get Here?

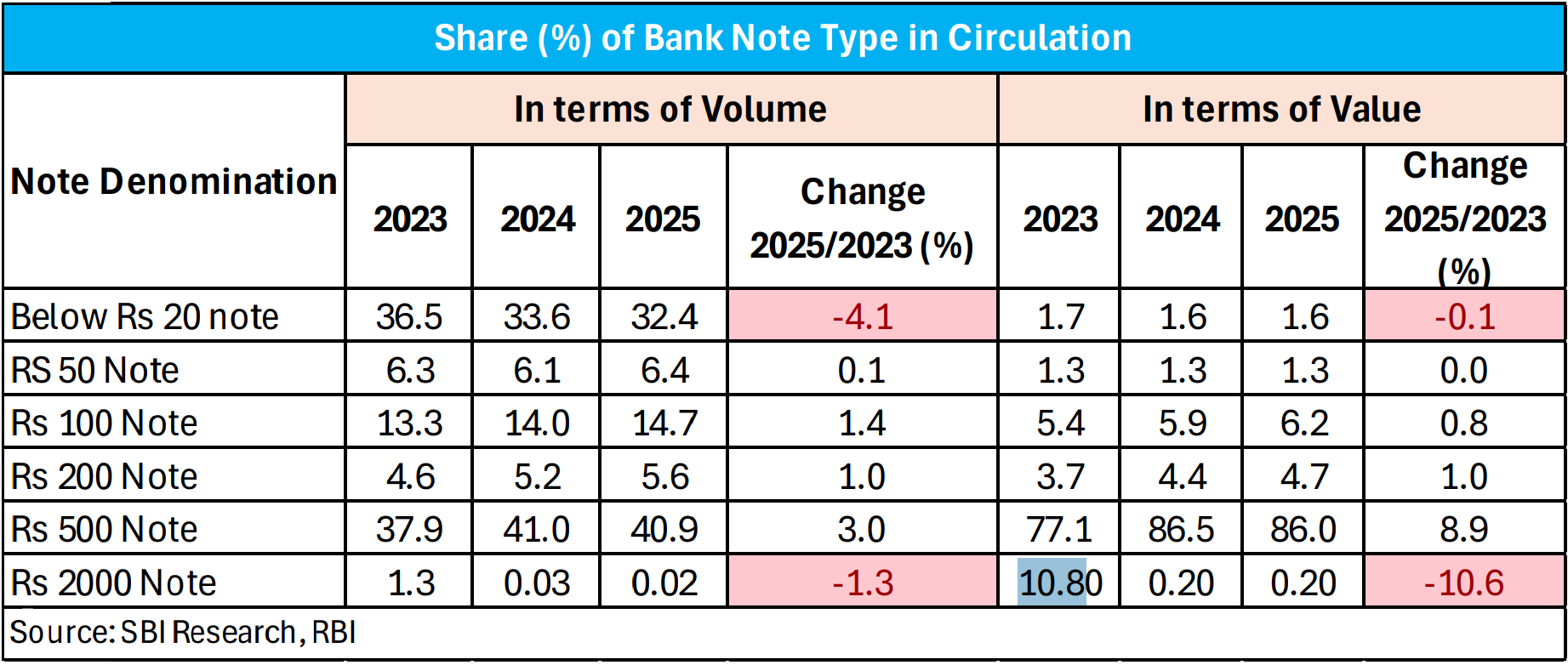

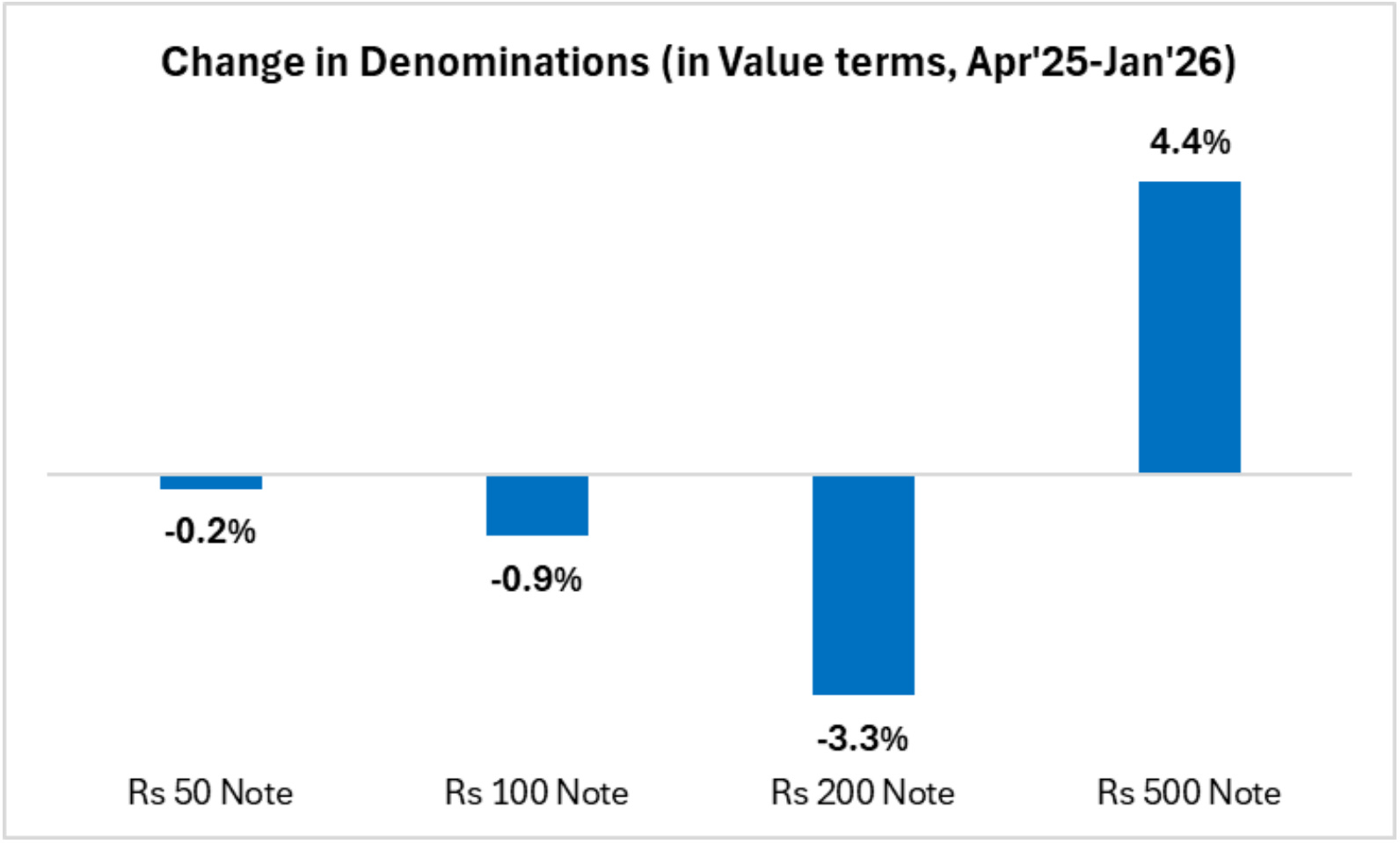

Start with the most obvious trigger. In May 2023, the RBI announced the withdrawal of the ₹2000 note. By end-March 2025, the ₹2000 note had gone from holding 10.8% of currency value to a mere 0.2%. Now, something had to fill that vacuum.

The ₹500 note stepped in. It now accounts for 86% of India’s currency in value terms, up 8.9 percentage points since 2023. In the current fiscal year (April 2025 to January 2026), SBI Research estimates the ₹500 note’s share has risen by a further 4.4%. Meanwhile, the shares of ₹50, ₹100, and ₹200 notes are all declining. Physical small change is genuinely becoming rarer. Meanwhile, bus and auto commutes to and from work are becoming an exercise in negotiating with the conductor or auto wale bhaiya.

But the ₹2000 withdrawal only explains the denomination shift. It does not fully explain why total CiC is surging. For that, SBI Research points to three other forces.

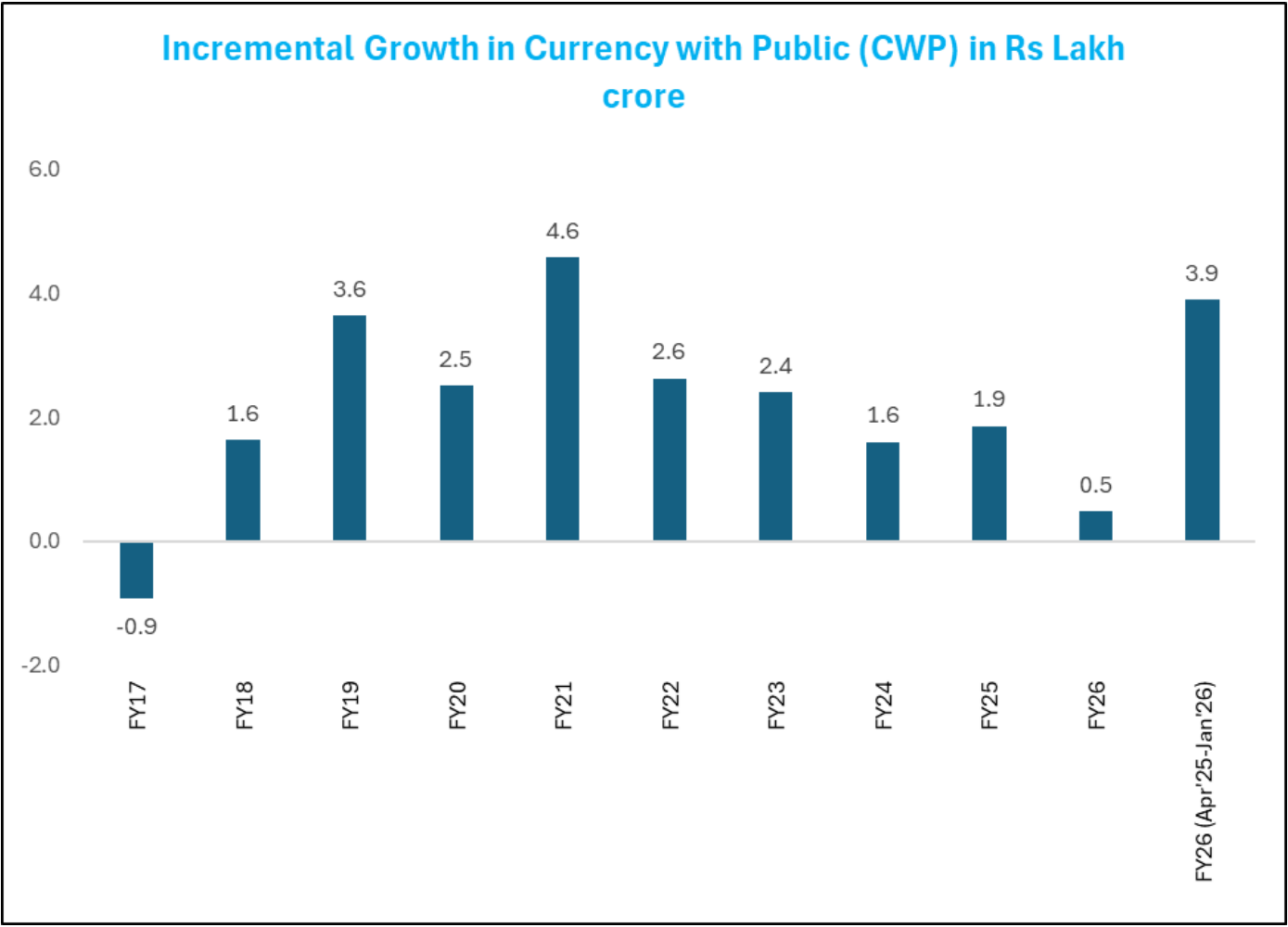

First, interest rates. When returns on deposits fall, people are less incentivised to park money in banks. Deposit growth remained sluggish this fiscal year at 10.6% as of end-January 2026. SBI’s money demand model confirms this. Demand for currency rises when interest rates fall, particularly among rural households with a preference for consumption spending.

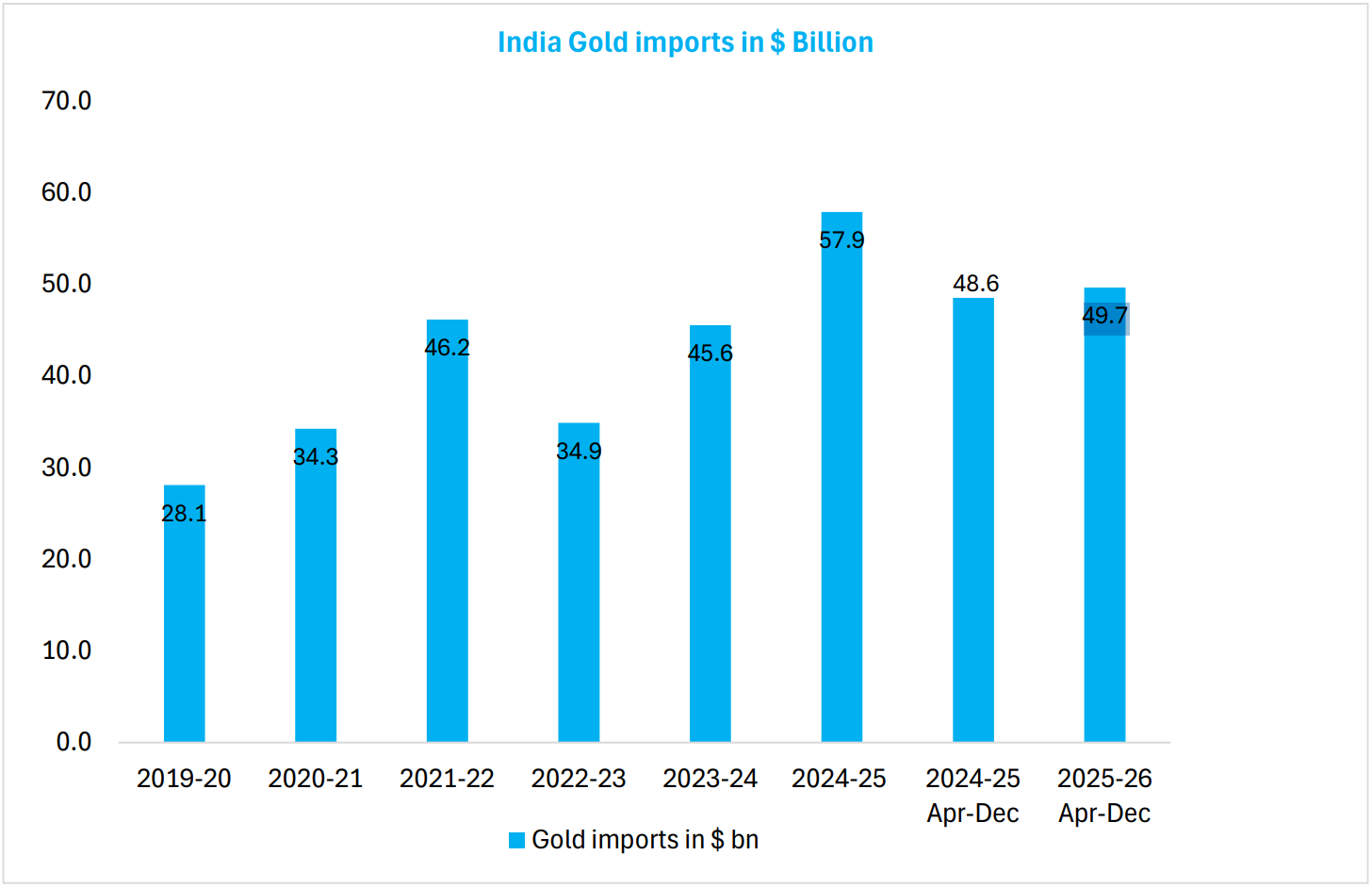

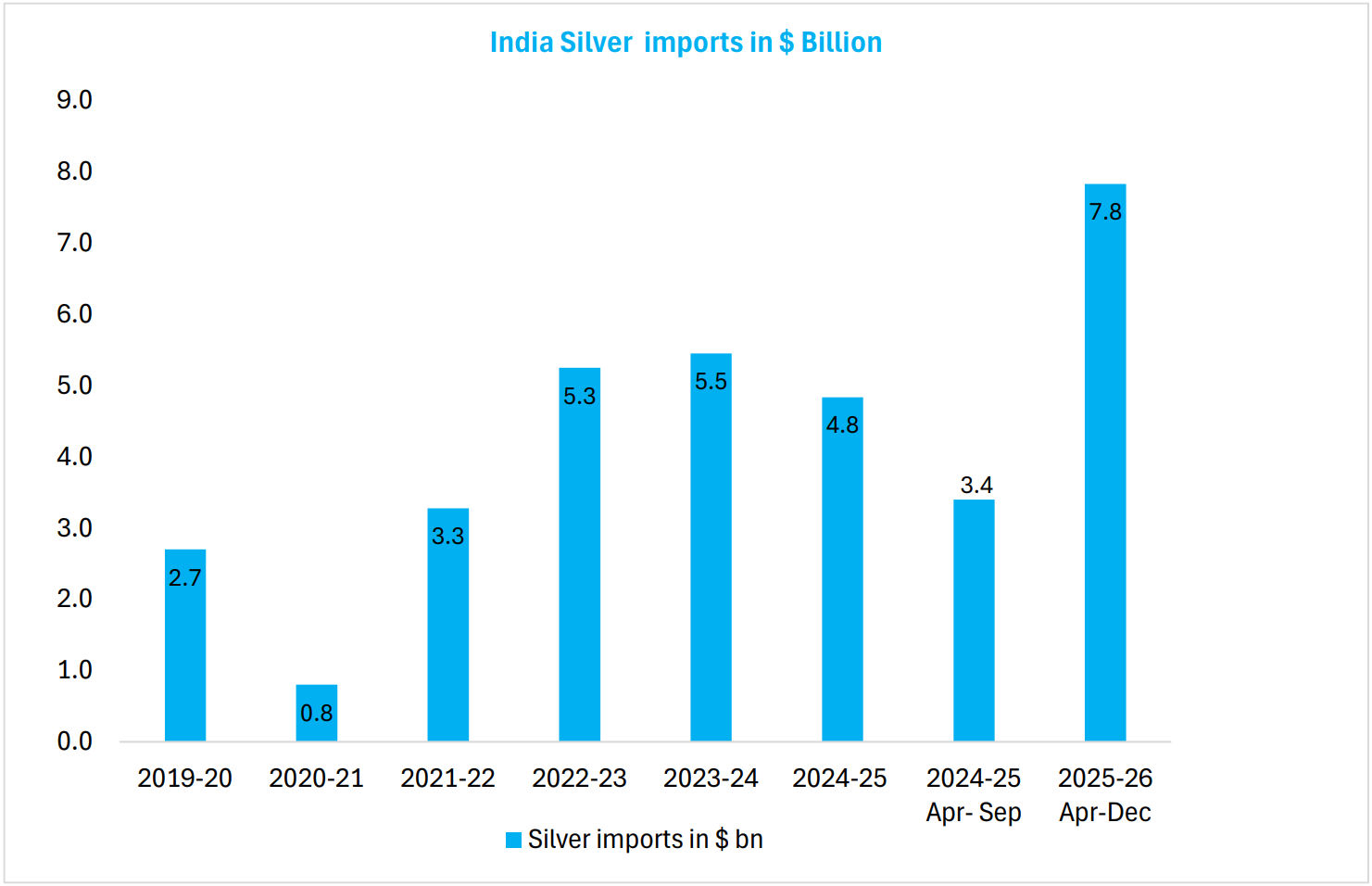

Second, precious metals. Gold imports in the first nine months of FY26 reached $49.7 billion. Silver imports surged to $7.8 billion, the highest on record. Households that had accumulated gold and silver over years have been cashing out these holdings as prices soared, converting physical assets into spending money. That cash then enters circulation. Unlike FY10-13, when rising gold imports coincided with hoarding behaviour, this time the cash seems to be flowing back into consumption. SBI calls this the “power of financialisation.”

Third, fiscal policy. Income tax cuts and GST reductions in recent months have put more money in people’s hands, boosting consumption, and with it, the demand for cash for everyday spending.

One Hiccup Worth Watching

Here is something that almost went unnoticed. In July 2025, Karnataka’s Commercial Taxes Department issued around 18,000 GST demand notices to small traders and vendors whose UPI transactions had exceeded the ₹40 lakh registration threshold between 2022 and 2025. The notices were not illegal, but they sent a powerful signal.

SBI Research tested whether this news nudged small traders back toward cash, not just in Karnataka but in other states. They used a statistical technique called Difference-in-Differences, comparing ATM withdrawal behaviour across districts with higher pre-existing cash usage against those with lower usage, before and after July 2025.

The results were shocking. In Karnataka, districts in the high-usage group saw an additional ₹37 crore in ATM withdrawals per month on average, compared to low-usage districts, after the notices were issued. Even excluding Bengaluru Urban, the effect held at ₹10 crore per district per month. Bengaluru accounts for nearly 30% of the state’s ATM withdrawals. West Bengal and Kerala also showed statistically significant effects. Bihar and Chhattisgarh did not.

The policy lesson here is simple but important. When traders fear that going digital might expose them to tax notices, they go back to cash. One state’s enforcement action rippled outward through news channels, nudging behaviour in states hundreds of kilometres away. If digital payments are made to feel threatening, people opt out. Even if the threat was created accidentally. And that is a problem, because the whole system only works if UPI keeps absorbing the volume of small transactions.

What Is Being Done?

The RBI appears to be aware of the absent ₹100 and ₹200 notes. On April 28, 2025, it directed banks to ensure that 96% of ATMs dispense ₹100 and ₹200 denomination notes by end-March 2026. This is a direct acknowledgement that the supply of small notes through ATMs needs to improve.

The directive is a reasonable response. But it comes with a complication. Currency chest data suggests the ₹500 note’s share is still rising within the system, while the shares of ₹100 and ₹200 notes are actually declining during this fiscal year. Whether the RBI’s directive translates into actual denomination availability at ATMs in time, remains to be seen.

The deeper structural response, though, is not about printing more small notes. It is about UPI replacing them.

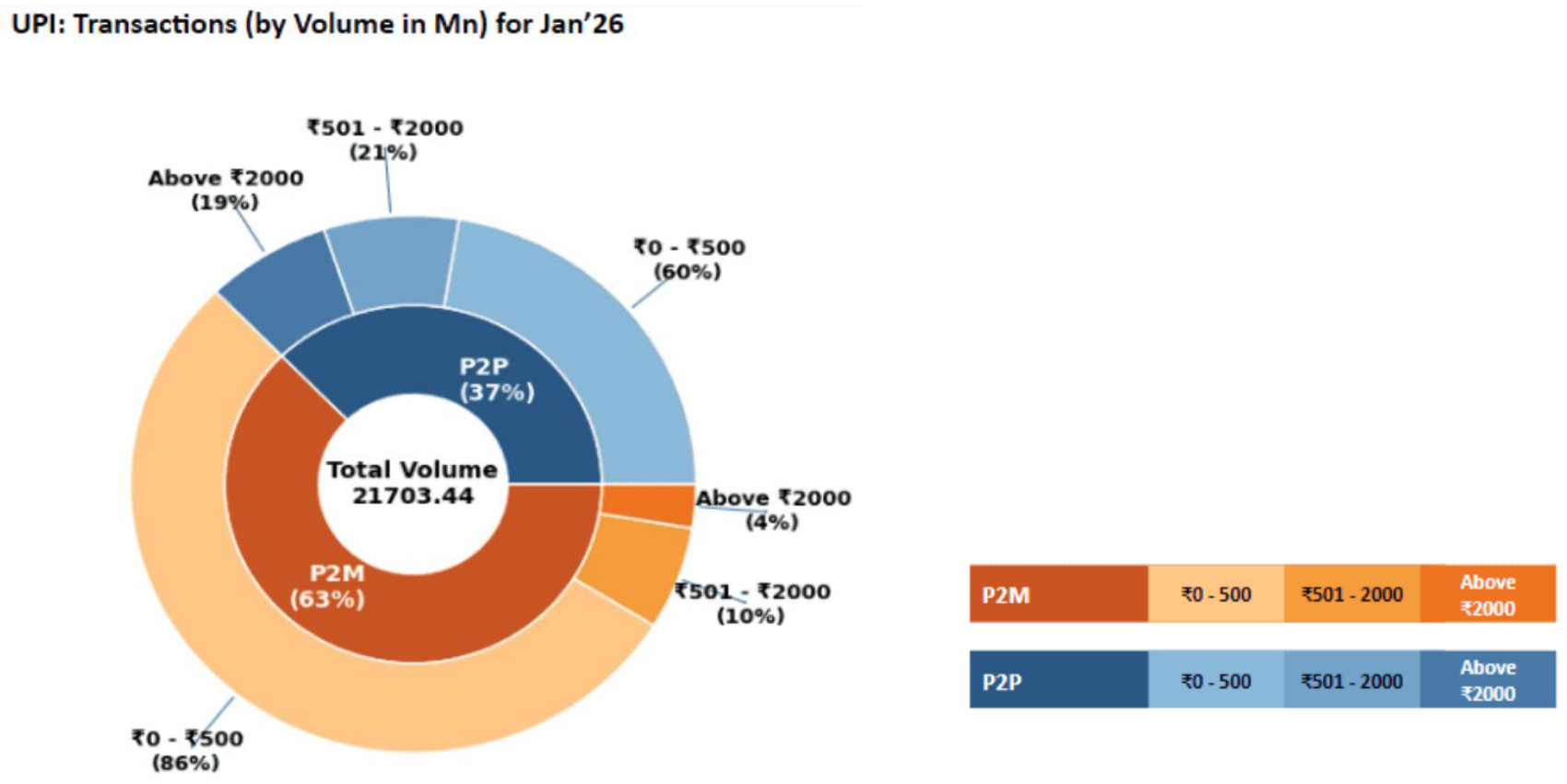

According to NPCI data, 86% of all Person-to-Merchant UPI transactions by volume are below ₹500. The chai stall, the vegetable vendor, the neighbourhood pharmacy, every transaction that once needed a ₹20, ₹50, or ₹100 note is now increasingly happening through a QR code scan. UPI has not replaced the ₹500 note yet. But it has largely replaced the need for smaller ones.

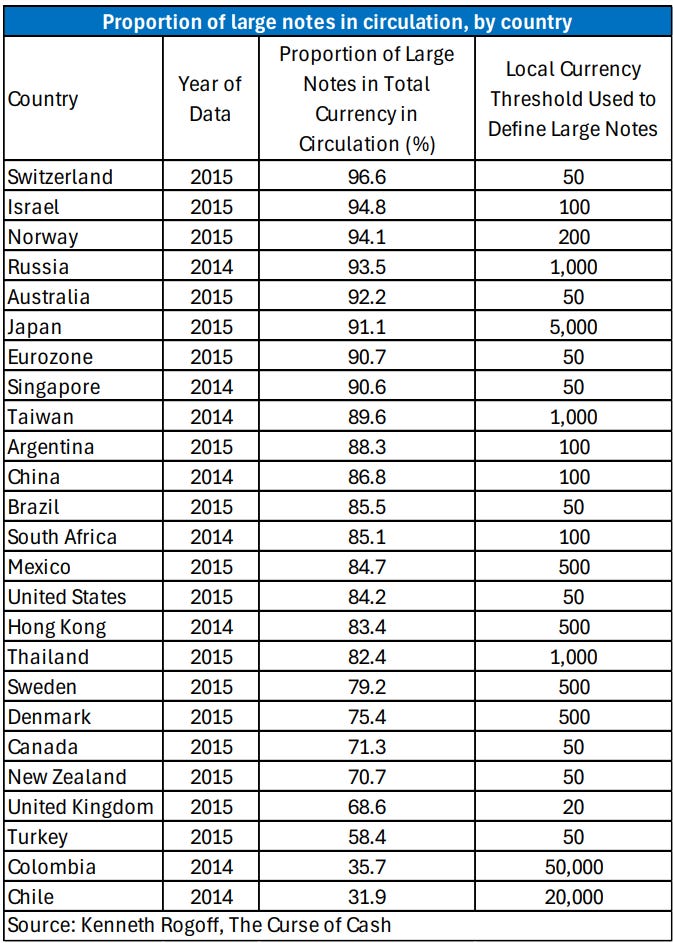

Kenneth Rogoff is a Harvard economist who wrote “The Curse of Cash” in 2016. According to Kenneth, eliminating larger denomination notes was impossible to engineer. He argued that large-denomination notes were a massive policy problem, used disproportionately to facilitate tax evasion and shadow economic activity. His data showed that in most advanced economies, large notes account for over 80% of total currency value. Eliminating them, he said, was politically and practically treacherous.

India has taken a different route. It did not eliminate the large note. It eliminated the largest one (the ₹2000), and let the ₹500 dominate. At the same time, it built a digital payments infrastructure so pervasive that 86% of spends at a merchant via UPI involves an amount under ₹500. The cash-to-GDP ratio has kept falling even as total cash in the system keeps rising. The economy is growing and transacting more, but increasingly doing so digitally rather than in notes.

The Takeaway

India has not solved the problem of cash. But it may have solved a version of it that no other country has managed. It made large-denomination notes less economically relevant without banning them. It did so by giving ordinary citizens a fast, free, and near-universal digital alternative for the very transactions those notes once served.

The risk is that this arrangement is fragile. The Karnataka episode showed how quickly confidence in digital payments can erode when regulatory actions are perceived as surveillance. SBI Research’s conclusion deserves to be read by policymakers as clearly as it was written.

“Never disincentivise digital payments.”

The chhutta problem will persist for a while. But it is increasingly a problem of ATM configuration, not of economic design. And that, honestly, is a much easier thing to fix.

Until that happens, ReadOn!