India’s Missing Monsoon

Rains are just the first domino.

At ReadOn, we don’t just report the markets. We help you understand what truly drives them, so your next decision isn’t just informed, it’s intelligent.

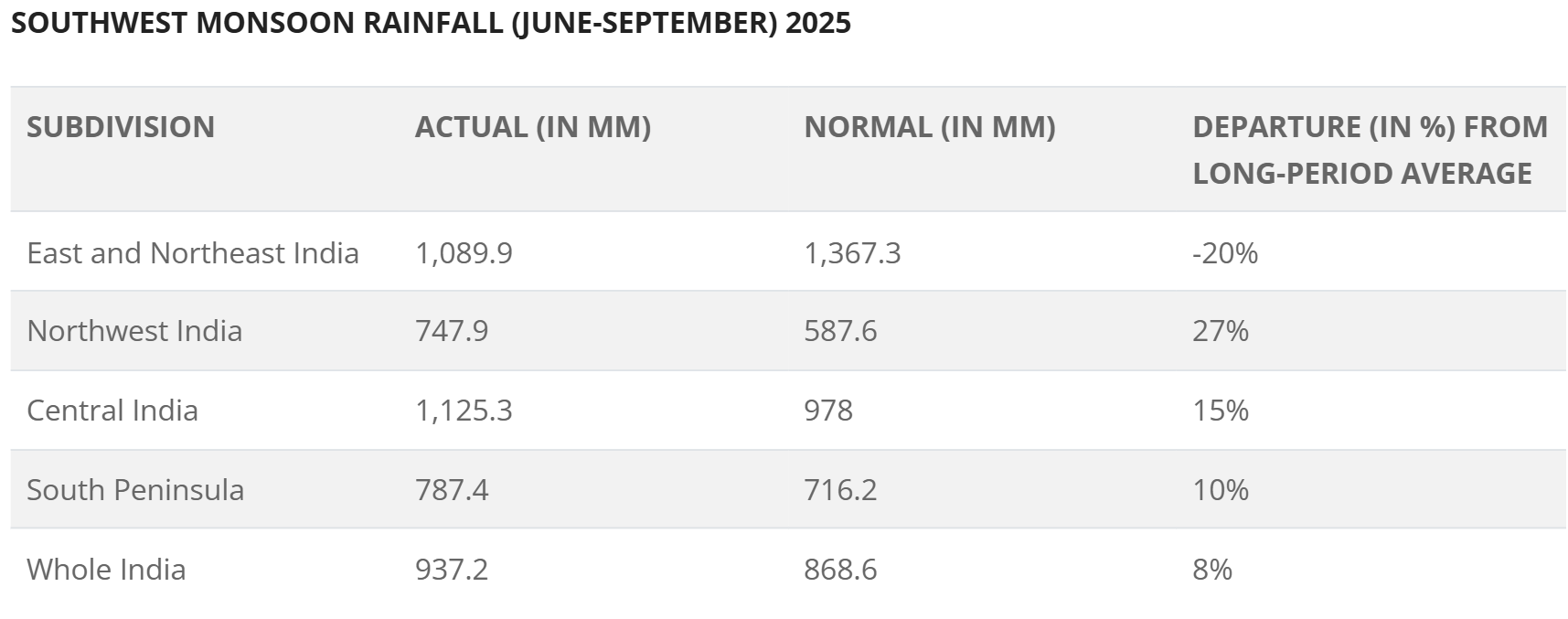

In 2025, India received 937.2 millimetres of rain between June and September. That’s the fifth-highest monsoon tally since 2001, and roughly 8% above what fifty years of data call “normal.” For an economy where close to half the farmland still depends on rainfall rather than canals or borewells, that’s about as good as news gets.

Source: Farming Cosmos

Agriculture certainly thought so. The kharif harvest that followed produced a record 173.33 million tonnes of foodgrain, with rice and maize both hitting all-time highs and most regions reporting healthy crop growth despite a few pockets of excess rain. Agricultural GVA grew 3.6% in the first half of FY26, up from 2.7% a year earlier. That’s a jump the government’s own Economic Survey credited directly to the favourable rains. The good cheer didn’t stop at the farm gate either. Rural FMCG volumes grew 8.4% against 4.6% in cities through April–June, making it the sixth straight quarter rural India outran urban, while tractors, two-wheelers, and rural passenger vehicles all sold faster in the countryside than in town through the sowing season.

Source: Careratings

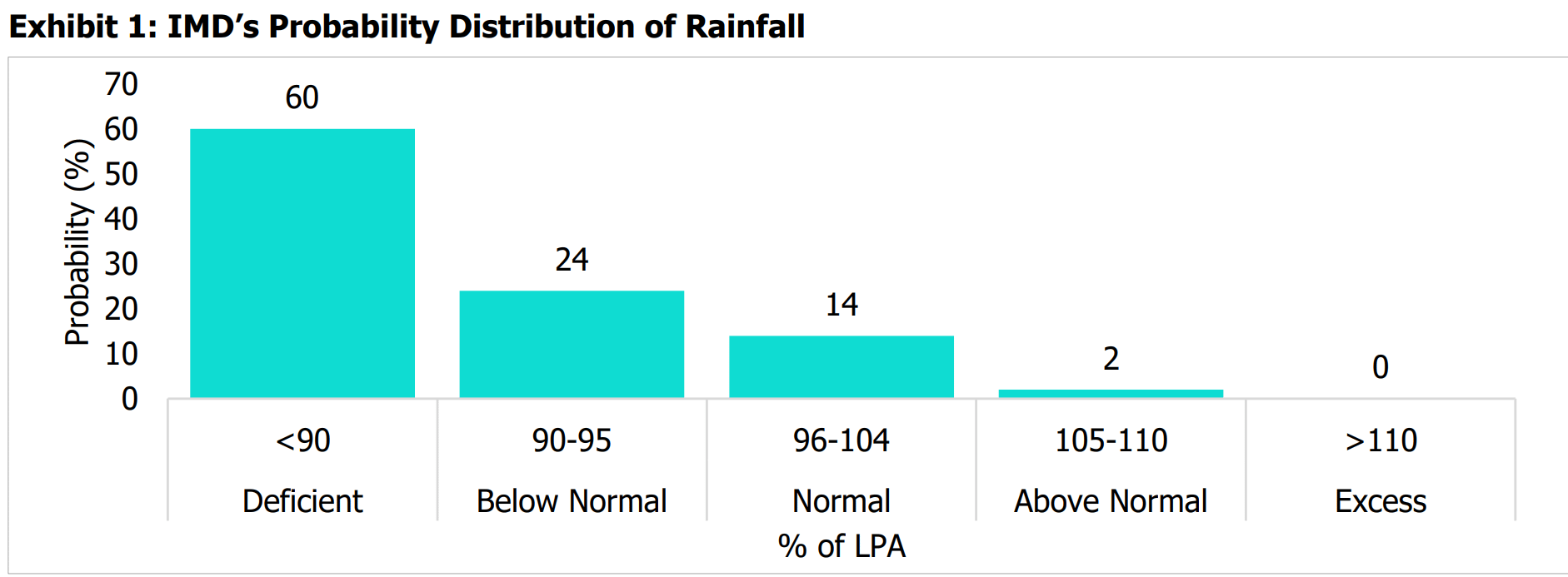

Now rewind that tape for 2026. A recent CareEdge report shows the India Meteorological Department has trimmed its monsoon forecast to 90% of the long-period average, down from 92% just a month earlier, with an 84% probability of sub-normal rainfall, sharply up from 66% in April. The US weather agency NOAA reckons there’s a real chance of at least a moderate El Niño settling in through the season. Translation: less rain, and meaningfully higher odds of it.

So what does a stingier monsoon mean for an economy that, until very recently, was riding a rather generous one?

The rain’s longer shadow

Agriculture is the obvious casualty, but monsoons move money well beyond the farm. Auto and tractor makers track rainfall like a stock ticker. Mahindra’s tractor sales jumped to roughly 39,000 units last year purely on sowing optimism. In fact, due to pessimism around the incoming deficient monsoons, the Indian tractor industry is forecasting growth to fall to 1-4% in FY27. Even FMCG giants from HUL to Dabur build entire quarterly forecasts around July rainfall. Fertiliser, seed, and pesticide companies live by the same calendar, and so, increasingly, does crop insurance, where a bad season means a flood of claims rather than premiums.

Microfinance and rural lending follow a similar script: a good kharif means farmers repay on time and rural loan books stay clean, while a poor one shows up months later as stressed assets at lenders with heavy rural exposure. Paint companies time their biggest marketing pushes for the weeks right after the rains stop, betting on a fresh round of repainting, while sugar mills and cotton ginners watch the same four months just as closely, since cane and cotton yields swing with exactly the rainfall windows the monsoon delivers or withholds.

Then there’s the side of the economy that monsoons hurt rather than help. Cement and construction are the clearest example. The rainy quarter is structurally the weakest stretch for cement makers every single year, because heavy rain stalls building sites regardless of whether the season is “good” for crops. Logistics and road freight slow down too, hydropower output swings with reservoir inflows, and even retail footfall dips when streets flood. The same four months that make a farmer’s year can dent a builder’s quarter. Which is why “good monsoon, good economy” is a far messier equation than it sounds.

A dry year doesn’t mean a dead one

Here’s where it gets interesting: El Niño doesn’t guarantee a bad monsoon. It just loads the dice. CareEdge’s own analysis of 25 El Niño episodes since 1951 found that 16 of them were moderate-or-stronger, and only 12 of those actually produced below-normal or deficient rainfall. So crops don’t simply “fail” in an El Niño year. What typically happens is messier. Yields and sown area come under uneven pressure, with some crops and regions hurting badly while others sail through largely unaffected.

The split between kharif and rabi crops matters here. Kharif crops, like rice, maize, pulses, and oilseeds sit directly in the monsoon’s path, sown the moment the rains arrive. Rabi crops like wheat lean more on groundwater, canals, and the reservoirs the monsoon refills, so a weak season hits them with a lag, through lower water tables and tighter irrigation come winter, rather than immediately.

Pulses are the classic casualty. A NITI Aayog assessment found 15 of the last 25 El Niño episodes coincided with declines in pulse acreage and yields, largely because pulses are grown mostly without irrigation. Layer the fertiliser story on top, and it gets stranger still. India’s DAP sales actually fell 12.8% between April and July 2025. Not because farmers didn’t want fertiliser, but because demand surging off the good 2025 monsoon outran stagnant domestic output and squeezed imports. Now, with the 2026 outlook weaker, the government has scaled down its kharif fertiliser requirement with urea demand cut by roughly 2%, DAP by nearly 5%, even as DAP and NPK stocks run well above last year’s levels, with urea holding steady. A worse monsoon outlook, oddly enough, is easing the very shortage a good one created.

Food prices don’t move in lockstep with rainfall either. CareEdge’s own data on past deficient-rainfall years shows a mixed relationship with food inflation. Even the very strong El Niño of 2015-16 barely dented prices, cushioned by buffer stocks and stable global commodity costs. The categories worth actually watching are the volatile ones: tomatoes, onions, and potatoes, which spike on weather shocks almost on cue, plus palm oil, where India’s reliance on Malaysia and Indonesia means a poor monsoon overseas can show up as costlier cooking oil at home.

The Takeaway

The good news, per CareEdge, is that India isn’t walking into this blind. Reservoirs stood at 30.4% of capacity in May, against a 25.1% average in past El Niño years, and foodgrain buffer stocks sit at record levels. The Centre has flagged 197 vulnerable districts for contingency planning, and states like Maharashtra have rolled out their own playbooks on water conservation, fodder security, and restoring local water bodies, while the International Crops Research Institute for the Semi-Arid Tropics is pushing district-level plans built around drought-tolerant crops and water-saving practices.

Structurally, too, this isn’t the India that El Niño used to ambush. Irrigation now covers 60% of gross sown area, up from just 17% in 1951, and the agriculture ministry’s research network has released nearly 3,000 climate-resilient crop varieties since 2014. That matters because agriculture still employs 43% of India’s workforce even as its share of GDP has shrunk from 56% in 1951 to around 18% today. That’s a gap that explains why a bad monsoon can dent millions of incomes without necessarily denting the headline growth number. Crop insurance under the Pradhan Mantri Fasal Bima Yojana exists precisely for years like this one. Though a recent evaluation in Haryana found it offers real but partial protection, undercut by payout delays and patchy awareness rather than the safety net it’s sold as.

None of this is evenly spread. CareEdge’s resilience index ranks Odisha and Chhattisgarh as the most exposed states, thanks to weak irrigation and a heavy tilt toward water-guzzling crops, while better-irrigated, more diversified Rajasthan and Haryana sit at the other end of the table. Punjab is the odd one out. Its near-total irrigation and comfortable reservoirs still aren’t enough to offset a kharif acreage so heavily tilted toward thirsty rice.

So, back to that opening question: what does a stingier monsoon mean for India in 2026? Probably not a crisis. We have buffers, and the days when a weak monsoon alone could tip the whole economy are mostly behind it. But it does mean a bumpier ride for whoever’s still tied closely to the sky: a farmer in Bundelkhand watching the clouds more anxiously than one in irrigated Punjab, a fertiliser importer recalculating shipments, a cement company hoping the rain behaves. The monsoon may matter less to India’s GDP than it once did. It still matters enormously to who, within that GDP, ends up paying for it.

Until the next rain, ReadOn!