India’s Gas Dreams

Natural gas can either be a stepping stone, or a hurdle, and India needs to decide.

At ReadOn, we don’t just report the markets. We help you understand what truly drives them, so your next decision isn’t just informed, it’s intelligent.

India’s greenhouse gas emissions, now at roughly 4.3 billion tonnes of CO2-equivalent a year, have climbed by close to a third over the last decade. In 2024 alone, the country logged the largest absolute year-on-year emissions increase of any nation on the UN’s books. Our dependence on coal and other oil based fossil fuels also exposes us to a lot of forex shocks. We’ve all seen how much our import bill and current account deficit blows up when bombs drop near the strait of Hormuz (we won’t bore you with repeated numbers here).

Without a faster pivot away from coal and oil, which together still meet over 80% of the country’s primary energy needs, we’ll keep heating the planet, and hurting the national wallet.

The trouble is, economies don’t leapfrog from coal to solar overnight; grids, factories and trucking fleets switch fuels in steps, not jumps.

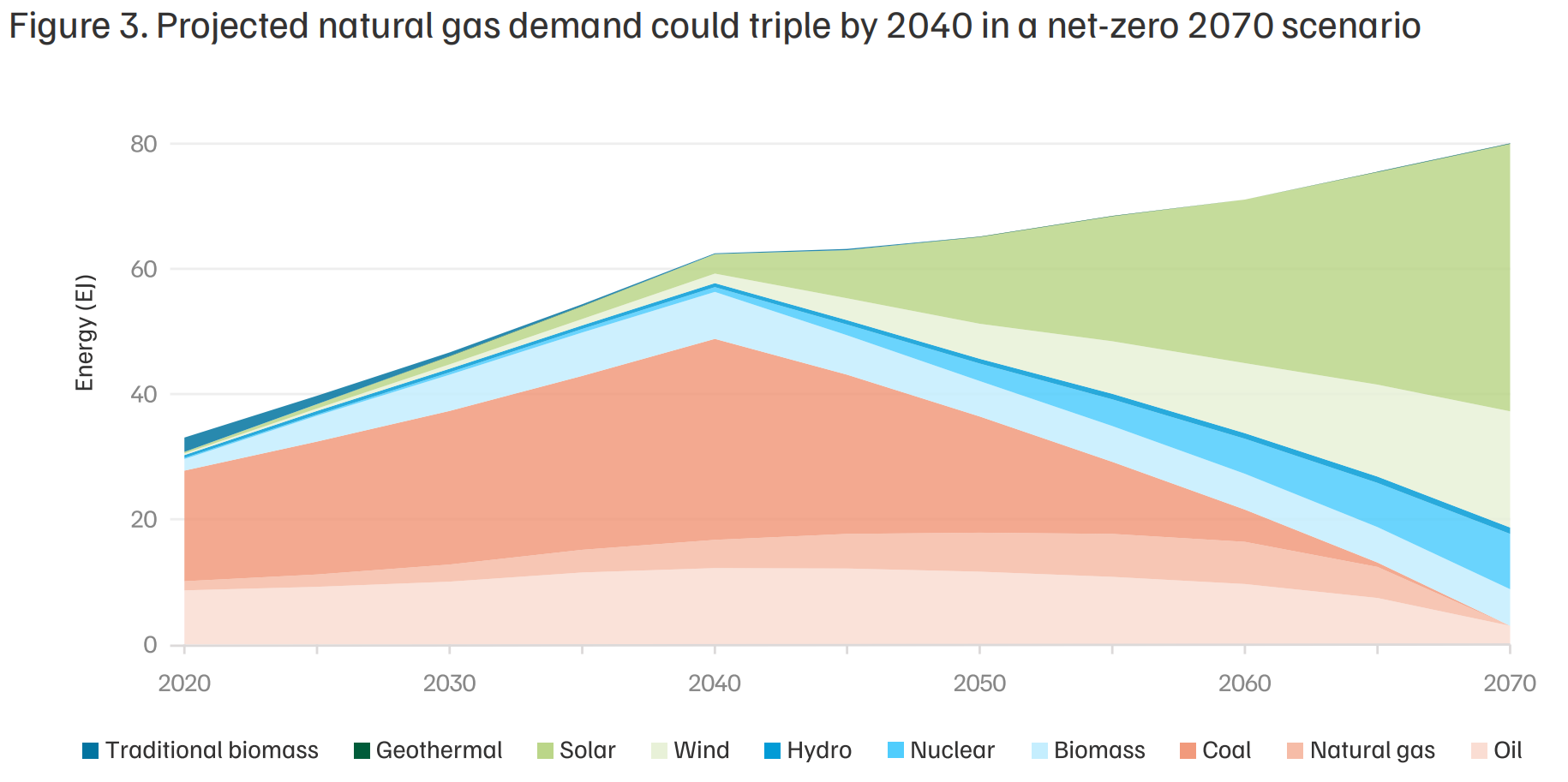

According to a recent CEEW policy brief, the next rung on that ladder is natural gas. Consumption could nearly triple from 53 bcm in 2025 to 180 bcm by 2040, even within a pathway consistent with net-zero by 2070, before the fuel itself gets phased down. Gas isn’t India’s destination, it’s a bridge.

So graduating to natural gas has its advantages, but it has its own challenges. Let’s find out what these challenges are, and what it would take to move on.

Why gas, though?

Because when you burn it, natural gas releases roughly half the CO2 of coal, and about a third less than oil-derived fuels, for the same unit of energy, since methane’s extra hydrogen burns into water rather than CO2. That shows up in CEEW’s own sector math. Gas-based steelmaking can cut emissions by 30 to 60% against the coal-fired blast furnaces that make nine-tenths of India’s steel today, and LNG-fuelled trucks already on Indian highways offer better range and a lower running cost than diesel rigs. The catch is that gas’s clean reputation depends on plugging leaks. Methane escaping during production and transport traps roughly 80 times more heat than CO2 over 20 years, and the US EPA puts 60% of that leakage at the production stage alone. Gas is cleaner than what it replaces. It isn’t clean.

Beyond Power

Power, oddly, is the smallest reason India wants more of it. Gas-fired power plants ran at just 14.9% utilisation in FY24 because gas costs more than coal or solar per unit. The real demand sits elsewhere, starting with fertiliser, which alone consumes nearly a third of India’s gas since almost every urea plant runs on it as feedstock, propping up a subsidy bill north of $20 billion a year. That dependence also puts gas prices on the dinner table directly. It makes up nearly four-fifths of what it costs to manufacture a bag of urea, so when the Strait effectively shut in early 2026, India’s urea output fell by an estimated 30,000–35,000 tonnes a day and domestic urea prices climbed 20% year-on-year by March, right through the kharif season that decides how much rice and wheat India grows.

Then there’s the road. City gas distribution, mostly CNG for vehicles, is the second-biggest gas consumer, fuelling 4.5 million CNG vehicles as three-wheelers, taxis and buses defect from costlier petrol and diesel. Smaller industries like glass, ceramics, plastics are switching too, sometimes by choice, sometimes by court order, as in Morbi and the Delhi NCR. In fact, the switch even cost Morbi around a month of productivity as the Iran-US war choked natural gas supply to the ceramic hub. The gas shock moved through the fertiliser industry too, causing shortages and potential food crisis scares.

The Catch

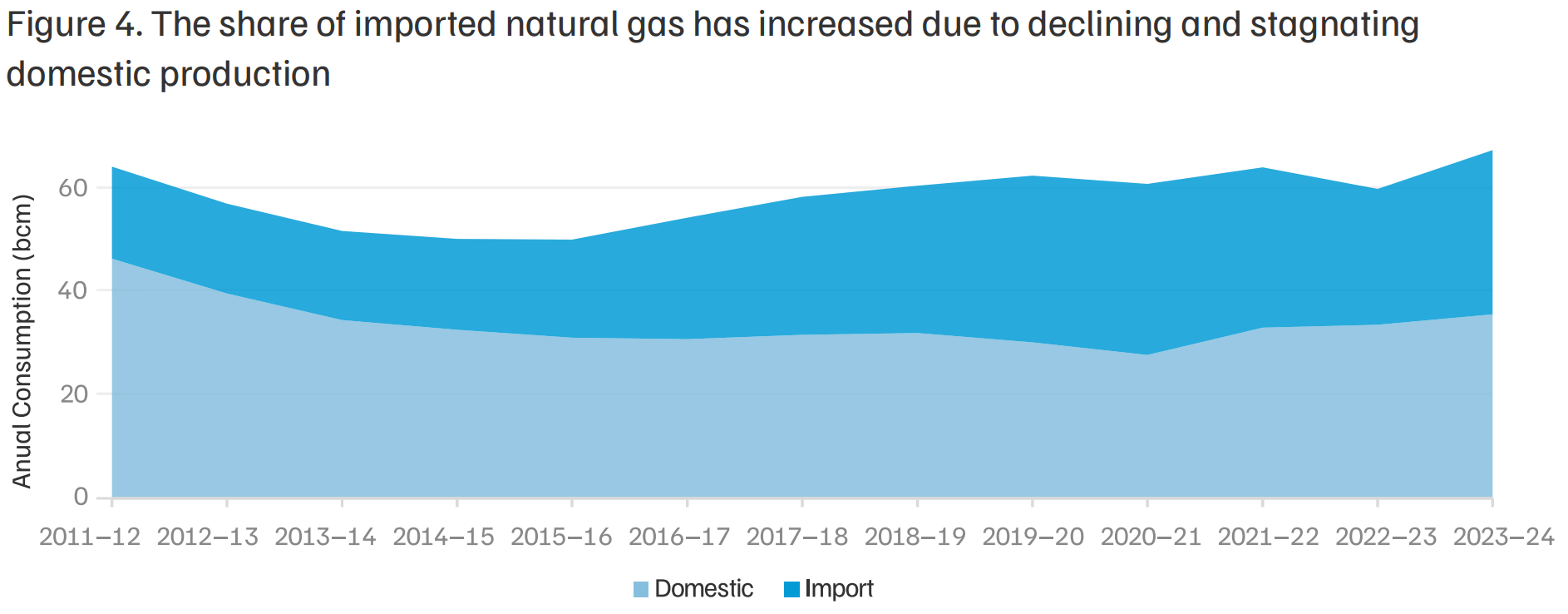

India doesn’t have nearly enough gas of its own. In FY24, the country consumed 68 bcm of gas but produced only 36 bcm domestically, leaving a $13.4 billion import bill and an import share that’s crept up from a third of supply in the early 2010s to roughly half today.

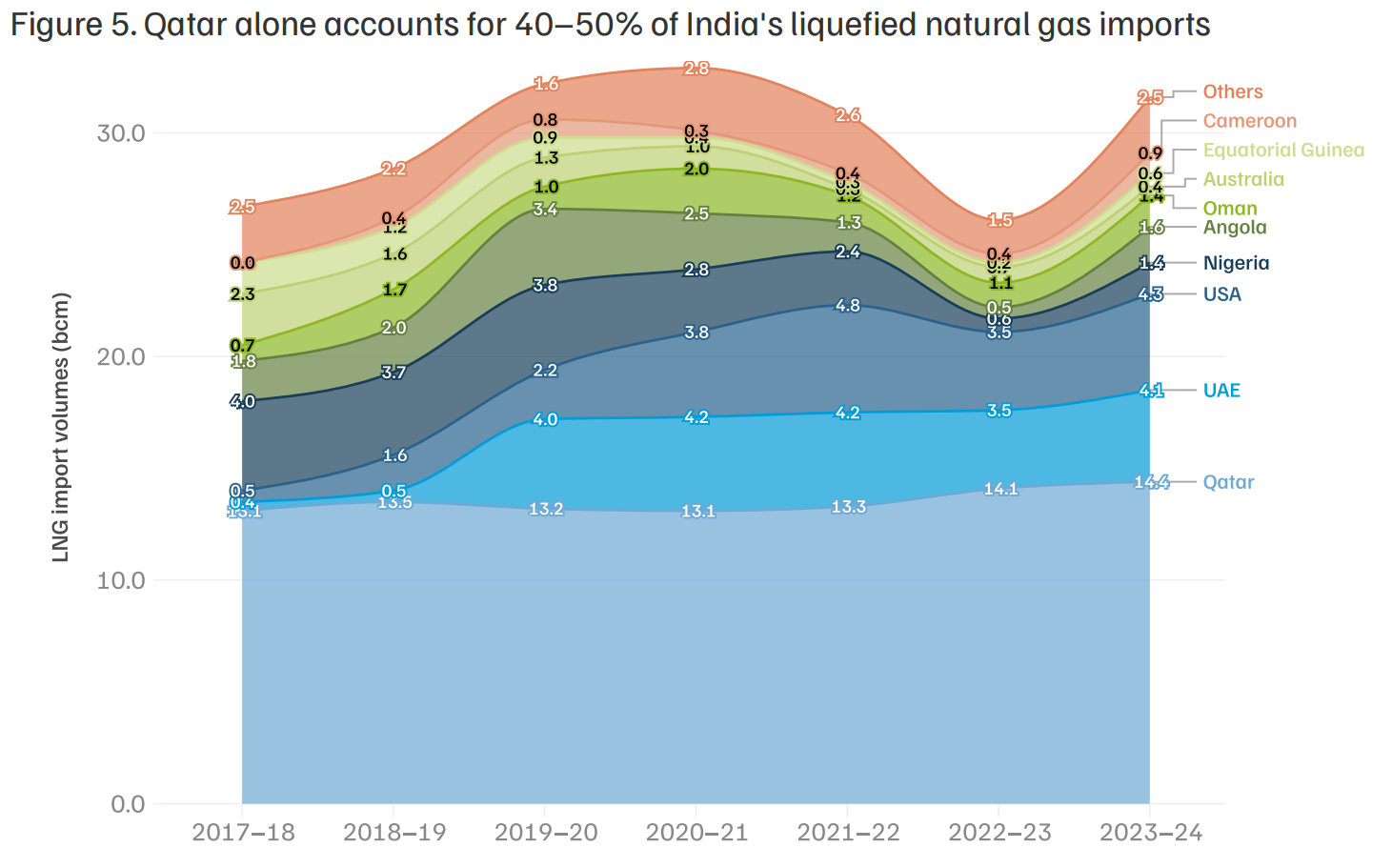

Qatar alone supplies 40–50% of that, and when the West Asia conflict briefly knocked out the Strait of Hormuz in 2026, it disrupted close to 60% of India’s LNG imports overnight.

Into that gap walks a promising find. In October 2025, Oil India confirmed gas (nearly 87% methane) flowing from its Sri Vijayapuram-2 well, the basin’s first confirmed hydrocarbon find after decades of patchy exploration. A 2017 government resource study pegs the wider basin’s potential at 371 million tonnes of oil equivalent, and more appraisal wells are drilling through 2026. But a discovery is not a supply contract: the reserves aren’t yet proven commercially viable, no production timeline exists, and even a generous outcome would take years to register against India’s 68 bcm annual appetite.

But that find won’t amount to much, because there’s a second friction here, separate from price: switching is mechanical, not just financial. A coal-fired boiler can’t simply be fed gas instead. Converting one means replacing the boiler or burner system outright, plus new piping and safety equipment, much like industrial furnaces. Plants and SMEs with capital sunk into coal rarely rush that switch.

The Domestic Gas Problems

Even the gas India does land costs more than it should, mostly because of how it’s taxed and moved once it’s onshore. Natural gas missed the 2017 GST rollout and still sits under the old VAT regime, where state rates range from 0% in Delhi to 25% in Chhattisgarh. Since VAT carries no input-tax credit, those levies cascade onto the final price at every stage. States barely gain from holding out, either: crude oil and gas together accounted for just ₹15,633 crore of the ₹2.5 lakh crore in sales tax that central PSUs paid all states combined in FY24.

Infrastructure compounds the tax mess. Pipeline capacity is booked point-to-point rather than through a flexible entry-exit system, so gas can’t easily flow to wherever a buyer happens to be; city gas operators get six to eight years of marketing exclusivity in their licensed areas, which limits competition; and only about 2% of India’s gas trades through the Indian Gas Exchange, which is the one mechanism actually built for transparent pricing. None of this is glamorous, but it’s exactly why those 25-plus gigawatts of gas power capacity sat idling at 14.9% utilisation even during summer heatwaves, when flexible generation should have been most valuable.

The Takeaway

The path forward, per CEEW, is duller than discovering a new gas field, but probably more consequential. On targets: drop the unrealistic 15%-by-2030 gas target. Its own modelling suggests it plateaus closer to 10% around 2055, and replace it with sector-specific goals for steel and heavy trucking, where gas has a genuine decarbonisation case.

On imports: use the wave of new LNG capacity arriving from the US, Canada, Mozambique, Argentina and the UAE through 2030 to sign fresh long-term contracts and dilute Qatar’s grip, ideally via a single demand-aggregating body. Something like the Solar Energy Corporation of India, but for gas, so industries like steel negotiate as one buyer instead of dozens.

On plumbing: bring gas under GST, move pipelines to entry-exit tariffs, and let the Gas Exchange trade more than a token 2% of supply.

None of that makes for a dramatic headline. But for a country whose import bill swings by tens of billions of dollars depending on what happens near the Strait of Hormuz, and whose farmers feel gas prices in their next bag of urea, the unglamorous plumbing of taxes, tariffs, and trading exchanges probably matters more right now than where the next gas field turns out to be.

Until next time, ReadOn!