India's Biofuel Bet

With global oil on fire (literally, and not in a nice way), India's trying to make the best out of waste.

At ReadOn, we don’t just report the markets. We help you understand what truly drives them, so your next decision isn’t just informed, it’s intelligent.

US-Iran war this, fuel prices rising that. Fuel sources hit. LPG and cylinder shortages.

Like we said in the previous piece, India has a gas problem. With all this doom and gloom news around it though, one is sure to lose their appetites to anxiety. So here’s a little appetizer for your thought. India’s energy problems do have a little domestic solution. It’s biofuel.

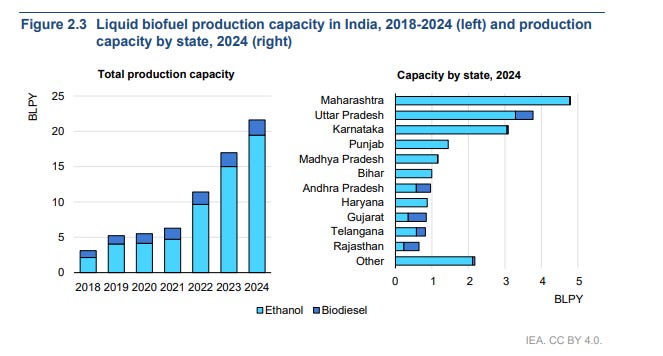

India’s biofuel production has more than doubled from 101 petajoules in 2018 to 210 petajoules in 2024. That’s enough energy to power all of Mumbai’s electricity needs for an entire year.

But not all biofuels are created equal, and not all are growing at the same pace.

Ethanol has gone from less than 2 billion litres in 2018 to 11 billion litres today, displacing 8% of India’s crude oil imports for petrol. Compressed biogas (CBG), extracted from cow dung, crop residues, and municipal waste, has grown eight times over since 2020, with 173 plants now operational and another 288 under construction.

Then there’s biodiesel, stuck at just 200 million litres a year because nobody’s solved the used cooking oil collection problem. And sustainable aviation fuel’s still just warming up, with India targeting 5% blending by 2030. Production, however, has barely taken off.

The International Energy Agency has released a detailed report on where India’s bioenergy market stands, and the numbers tell what’s working, what’s stuck, and where the real money and challenges lie.

Let’s break it down.

The Ethanol Success Nobody’s Talking About

Remember when the government said they’d blend 20% ethanol into petrol by 2025-26? Most people assumed it was one of those ambitious targets that would disappear. Except it didn’t.

India actually hit that target. And the machinery behind this success is worth understanding.

First, the government fixed ethanol prices based on feedstock costs. If you’re a sugar mill or distillery producing ethanol from sugarcane juice or damaged rice, you know exactly what oil marketing companies will pay you. No haggling, no market volatility. Just guaranteed prices updated regularly to keep you profitable.

Second, they threw money at the problem. The government offered interest subsidies of 6% per year (or half the bank’s interest rate, whichever is lower) to build new ethanol plants or upgrade existing ones. Result? India’s ethanol production capacity jumped from just over 2 billion litres in 2018 to more than 19 billion litres today.

Third, they expanded what you could use to make ethanol. Started with molasses, then added sugarcane juice, damaged food grains, maize, and surplus rice from government stocks.

The impact? In 2024 alone, this displaced 8% of what India would have otherwise imported as crude oil for making petrol. Rough estimates of the cost saved would be $10 billion (based on the 2024 crude import bill).

The CBG Story: Fast Growth, Real Challenges

Now let’s talk about compressed biogas, or CBG. This is essentially methane extracted from organic waste like cow dung, crop residues, municipal garbage, industrial waste, and more. This waste is then purified and compressed to run vehicles or flow through gas pipelines.

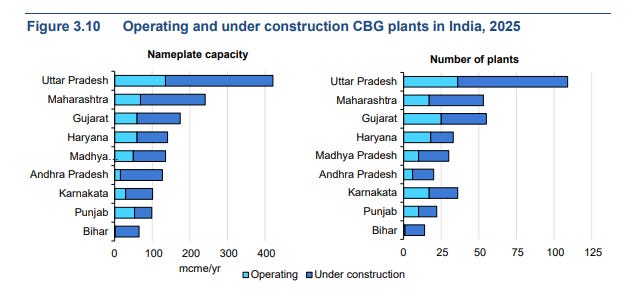

In 2020, India had 34 CBG plants. By the end of 2025, that number jumped to 173, with another 288 under construction.

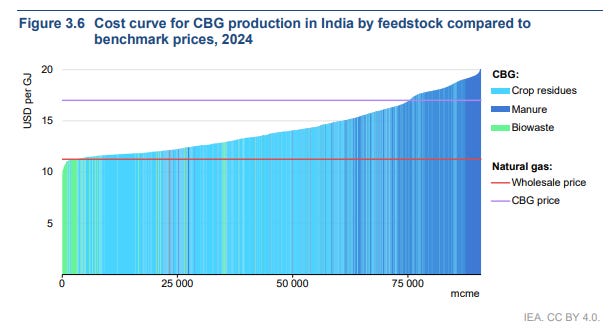

The IEA estimates India could sustainably produce up to 90 billion cubic metres equivalent of CBG every year. For context, that’s about 120% of India’s entire natural gas demand in 2024.

But here’s where it gets interesting. Of that 90 bcme potential, roughly 75 bcme can be produced for under $17 per gigajoule. The feedstock is there (45% from crop residues, 30% from animal manure, 24% from biowaste). The technology is mature. The policies are in place with the SATAT initiative, and rising blending mandates of upto 5% by FY 2028-29.

So why aren’t we seeing faster adoption?

The answer lies in feedstock aggregation.

Think about it. Paddy straw is available for collection for less than two months a year. It’s spread across millions of small landholdings. Farmers don’t have the infrastructure to gather and store it. And when they do collect it, many still burn it in fields because that’s simpler than transporting bales of low-density biomass to a CBG plant 50 kilometers away.

Municipal waste needs pre-segregation, where the organic fraction is separated from plastics and other junk. And most Indian cities still haven’t figured that out.

Animal manure from cattle farms sounds promising until you realize collection and storage costs can make or break the economics.

The government gets this. They’ve launched schemes like Biomass Aggregation Machinery to subsidize equipment for crop residue collection. They’re funding pipeline connections (50% subsidy) so CBG plants can inject directly into city gas networks instead of trucking it in expensive cascades. They’re offering ₹1,500 per tonne for selling the digestate byproduct as organic fertilizer.

But many existing plants are running at 20-60% capacity, way below the 80%+ rates you see in Europe. Seasonal feedstock, maintenance downtime, and limited local capacity to absorb the fermented organic manure byproduct are all dragging down utilization.

So India doesn’t even need more plants, just better operations can hit the blending targets.

The Biodiesel Puzzle: Stuck at the Starting Line

Biodiesel has a 5% blending target for 2030. But in the main case forecast, production is expected to stay flat at just 200 million litres per year.

Why?

Feedstock is the problem, again. Specifically, fats, oils, and greases.

Biodiesel is typically made from used cooking oil or vegetable oils. But India’s biodiesel producers can’t get enough of it. Used cooking oil collection remains fragmented. Thousands of restaurants and food processing units produce varying quantities. The supply chain hasn’t matured.

The IEA’s accelerated case shows biodiesel could hit 4 billion litres by 2030 (a twentyfold jump) if feedstock supply improves dramatically. That’s a big “if.”

A few states are trying. Uttar Pradesh offers production incentives. Maharashtra provides 70% capital subsidies for biodiesel plant machinery. But without solving the upstream feedstock problem, those subsidies won’t move the needle much.

The SAF Wildcard: Big Potential, High Costs

Sustainable aviation fuel is the newest frontier. India has set a target of 1% blending by 2027, rising to 5% by 2030, for international flights.

Air travel in India is booming with over 228 million domestic passengers and 64.5 million international passengers in 2024, with growth expected to continue. That creates both opportunity and urgency.

The problem? SAF can cost two to five times more than conventional jet fuel. And India’s SAF production is just getting started.

Indian Oil is building capacity. A 38 million litre plant at Panipat using used cooking oil, and another 109 million litre plant using alcohol-to-jet technology with LanzaJet. But meeting a 5% blending target by 2030 will require rapid scale-up, more feedstock (competing with biodiesel), and continued policy support.

The IEA forecasts SAF could hit 500-700 million litres by 2030, depending on how aggressively feedstock, technology, and infrastructure develop. That’s ambitious, but not impossible. If India replicates for SAF the policy intensity it brought to ethanol.

What’s Really Holding Things Back

Three challenges aren’t letting biofuel burn hot:

Feedstock logistics are hard. Biomass is bulky, seasonal, and dispersed. Collection, transport, and storage eat into margins. Until India builds robust aggregation systems, maybe through farmer-producer organisations, maybe through third-party aggregators with government support, this remains a choke point.

Co-product markets aren’t ready. When you make CBG, you get fermented organic manure as a byproduct. Roughly 23,000 tonnes per day by 2030, per the IEA’s forecast. That needs buyers, or farmers willing to use it instead of subsidized chemical fertilizers. The market is nascent. Without offtake, CBG plants can’t run at full capacity.

Infrastructure takes time. CBG needs pipelines or cascades to reach consumers. SAF needs distribution networks to reach airports. Biodiesel needs collection systems for used cooking oil. These don’t appear overnight, even with subsidies.

The Takeaway

India’s biofuel story is a tale of two speeds.

Ethanol is sprinting. CBG is jogging. Biodiesel is walking.

By 2030, liquid and gaseous biofuels could grow 50% in the main case (from 293 to 429 petajoules), or more than double in an accelerated case (609 petajoules) if biodiesel and CBG hit their stride.

India has the feedstock or the technology. But can policies evolve beyond setting targets to actually solving the messy, unglamorous problems of logistics, supply chains, and market creation?

Until the answer to that question arrives, ReadOn!