GameOn: The Indian Online Gaming Saga

The online gaming saga has begun! Stay tuned.

Feels like this year has been a never-ending loop of damaging news and breakdown of morale, no?

Mounting cases, contracting GDP, unemployment at all time highs!

Let’s stop there.

A beacon of light (if there ever was one) in these difficult times is the booming growth of the gaming industry. The lockdown has been hard. To overcome the glut, we’ve turned to OTT platforms and games to make our lives less monotonous.

Since we’ve already done a deep dive into the OTT industry (catch up here in case you missed out) – it's about time we put out a piece on the gaming industry.

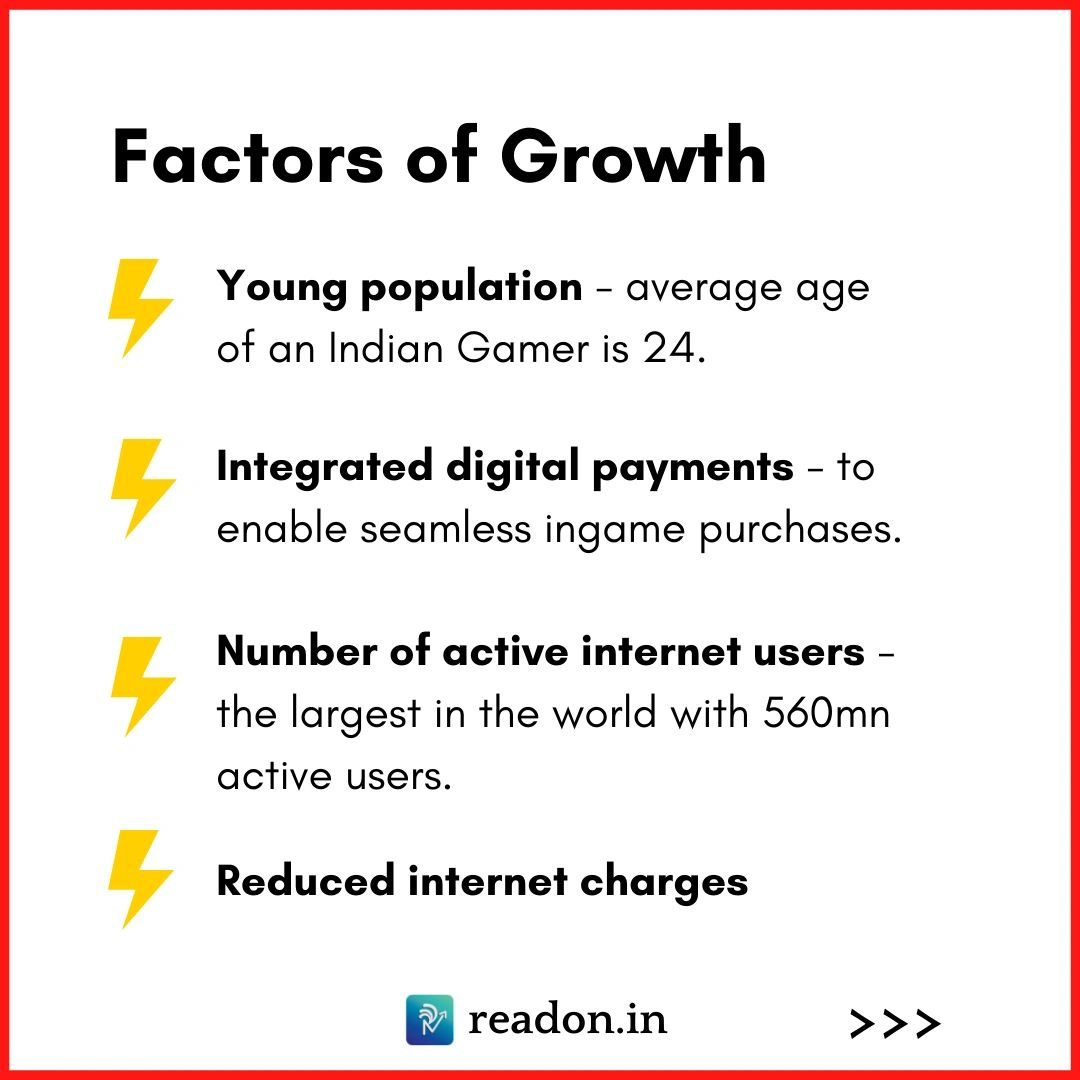

The flooding of cheap data and internet connectivity ushered in the era of online gaming in India. This created a massive demand for entertainment through videos, games and other audio-visual mediums.

A wave of gaming apps fed into this demand, as evidenced by the 400 odd gaming startups currently serving over 500 million smartphone users (as of December 2019).

Interestingly, mobile gaming has taken the lead, capturing 85% share of online gaming in India.

Thus, it became pretty evident that gaming developers are looking to capitalise on the increasing number of smartphone users.

Recently in a one on one conversation with the CEO of Microsoft Inc. Satya Nadella, Mukesh Ambani stressed on the importance of the gaming industry, and said “Gaming will be bigger than music, movies and TV shows put together”.

Quite an admission!

As per a report by Maple Capital Advisors titled ‘Gaming – India Story’, the online gaming industry is growing at a CAGR of 22% and is expected to grow 41% annually due to the growth of digital infrastructure and substantial rise in quality and engaging gaming content.

By 2024, the gaming industry in India is set to be valued at $3.75 billion (which is an underestimation, TBH).

How did the gaming industry achieve such traction in such a short span?

First let's understand why gaming as a sector has been so popular in India.

There are three key segments of online gaming:

Real Money Games (like Teenpatti Poker),

Mobile-centric/casual games (Candycrush), and

e-Sports (PUBG, COD).

A combination of the below factors have accelerated the growth of these key segments:

All these coupled with the extended lockdown has seen a jump in traffic in online gaming by 24% from March.

Fantasy sports (like Dream11) in the Indian market is expected to reach over $5 billion in the upcoming two years. This is attracting the eyeballs of opportunity starved Venture Capitalists and Private Equity Investors.

It is evident that foreign companies have taken note of the growth within the Indian gaming market and its user base and seek to invest in these new opportunities such as:

Tencent, Steadview Capital, Kalaari Capital, Think Investments and Multiples Equity have all invested in the unicorn company Dream11.

PayTM and Alibaba Group’s Hong Kong (based AGTech Holdings) invested in Gamepind, which is a localized platform hosting popular casual and sports games.

Baazi Games plans to invest $5 million in 2020, by focusing on gaming start-ups to nurture the latest gaming technology.

However, it’s not the user base that caught our attention.

Rather it is in understanding the money-making formula applied by these Gen Z gaming companies. According to Sensor Tower, PuBG made a revenue of $250Mn in May alone ($3 Bn when annualized).

To put it into context, that’s lower than what IPL made in 2019 (~$2Bn).

So, HOW do these games make money? WHAT is their success mantra?

Well, well. The Game has just begun!

Stay tuned.

Thousands of readers get daily updates on WhatsApp! 👇 Join now!