Falling Off the Patent Cliff

At ReadOn, we don’t just report the markets. We help you understand what truly drives them, so your next decision isn’t just informed, it’s intelligent.

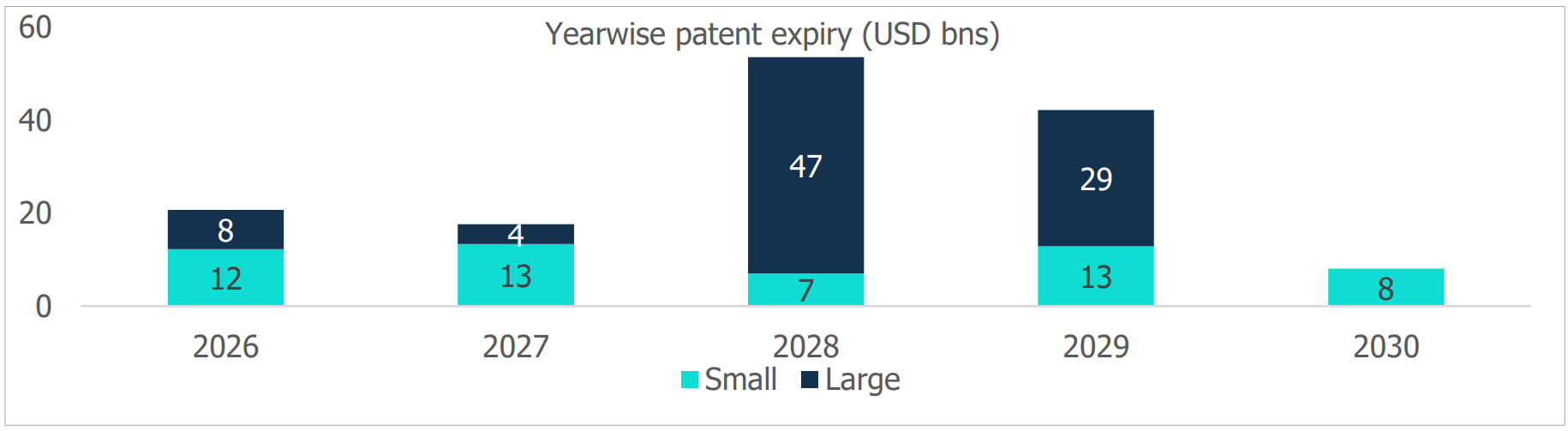

That’s the annual US sales value of drugs whose patents will lapse between 2026 and 2030. The list of drugs going off-patent includes everything from Keytruda, the world’s best-selling cancer drug, to Darzalex, a blood-cancer therapy that alone does billions a year.

Factor in the price collapse that follows every patent expiry, and you get a market opportunity north of $30-40 billion over five years. Of that, Indian pharmaceutical companies are expected to capture somewhere between $3-5 billion. It’s not exactly the lion’s share, but it’s enough to reshape a chunk of corporate India’s balance sheets over the next half-decade.

That gap between a $142 billion pool and a $3-5 billion catch tells you almost everything about where Indian pharma sits in the global drug chain. It’s a big number in absolute terms. It’s a rounding error in relative ones.

Let’s find out if India will free-fall off the patent cliff, or whether it will take a graceful swan dive.

What Exactly Is a Patent Cliff

A patent typically runs 20 years from the date of filing. For most of that time, the innovator enjoys a legal monopoly. Nobody else can make or sell the molecule. Once the patent lapses, the floodgates open: generic and biosimilar makers can launch copies, usually at 60–90% lower cost than the original, because they skip the decade-long, multi-billion-dollar discovery process entirely. When a cluster of blockbuster drugs loses protection around the same time, the resulting revenue cliff for innovators, and the resulting opportunity for everyone else, is what the industry calls a patent cliff.

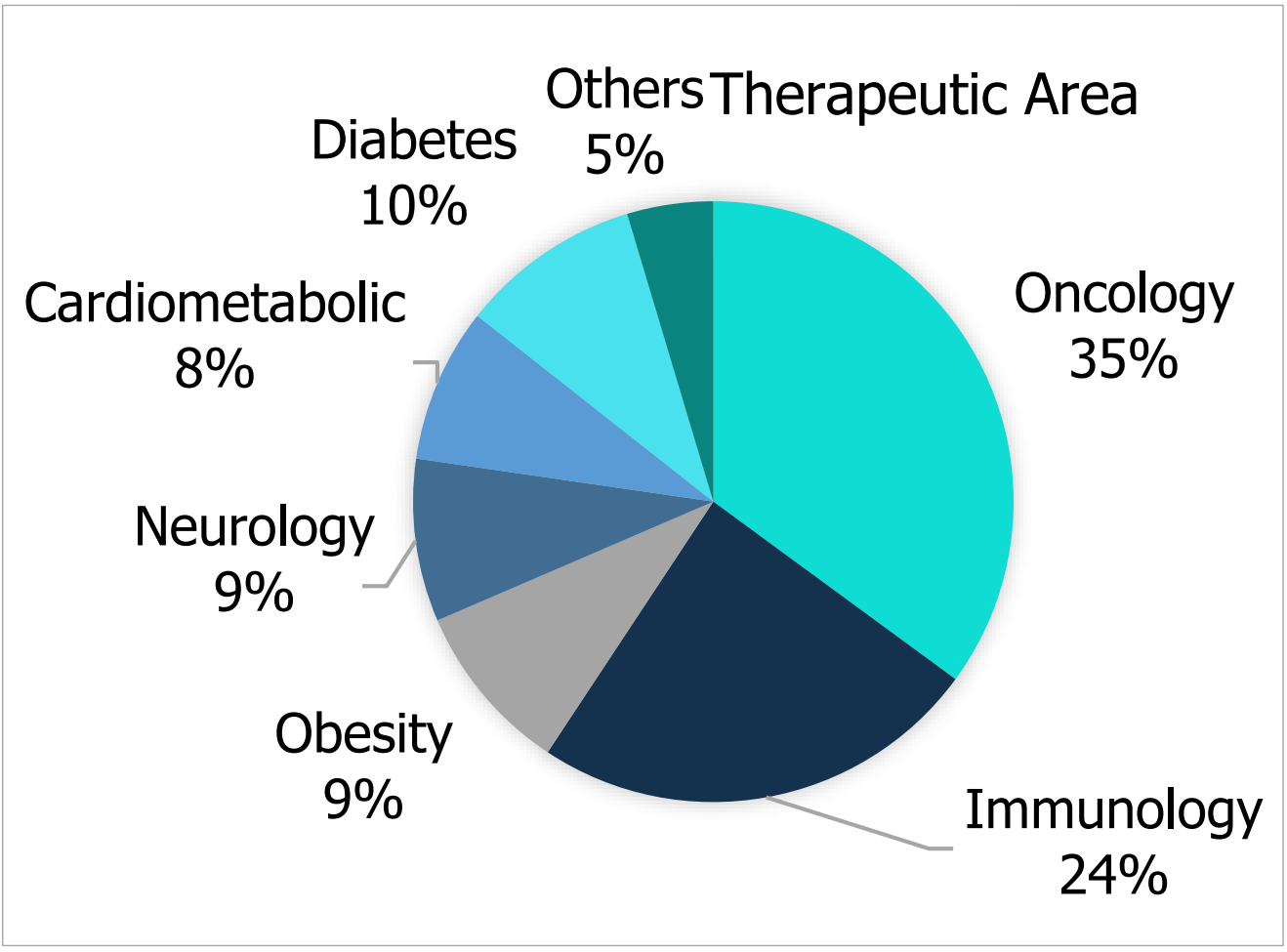

This one looks different from the last big one. More than 60% of the drugs expiring through 2030 are large-molecule biologics rather than simple chemical compounds. These are complex proteins grown in living cells that are genuinely hard to replicate, let alone manufacture at scale. And a large share of these molecules treat chronic, lifelong conditions, where the first credible generic to market tends to lock in prescribing habits and keep them. Speed, not just cost, decides who wins this round.

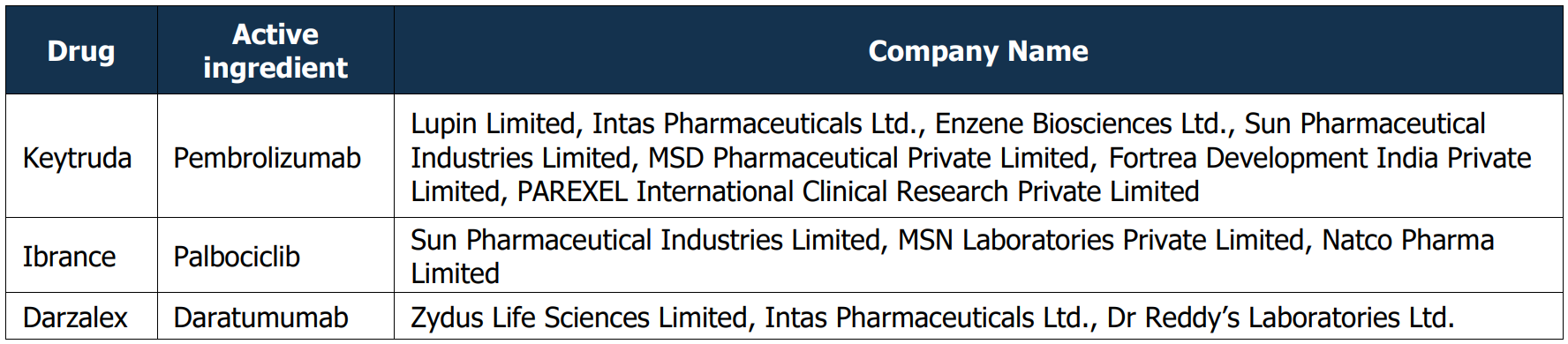

Indian companies have started positioning accordingly. CareEdge Ratings’ data shows firms like Lupin, Intas, Sun Pharma and Dr Reddy’s already lining up biosimilar versions of immunotherapy medication, while Zydus and Dr Reddy’s are doing the same for blood cancer medication. Biocon Biologics, arguably India’s biosimilar pioneer, has been steadily raising capital for exactly this fight, pulling in a fresh ₹555 crore from ADQ toward a roughly $330 million war chest for its biosimilar pipeline. Dr Reddy’s, facing its own patent-cliff problem as cancer medication exclusivity ends, is leaning on biosimilars for bone cancer and autoimmune medication to plug the gap, with HSBC projecting a $500 million semaglutide opportunity alone by 2027.

We’ve been here before, and the script is familiar. The last great cliff ran roughly during 2011–2015, when blockbusters like Lipitor (cholesterol control medication), Plavix (blood thinner) and Singulair (asthma medication) fell off patent in quick succession. Ranbaxy made the most of it, filing to challenge Lipitor’s patents seven years before official expiry and eventually securing 180-day exclusivity on generic atorvastatin from November 2011, a single product that briefly became one of the most profitable launches in Indian pharma history. Dr Reddy’s, Cipla, Aurobindo, Sun, Torrent and Zydus Cadila all piled into the same wave, grabbing more than 40% of all US ANDA approvals in early 2013. That cliff built the modern Indian generics giant. This one is being fought on harder terrain of biology instead of chemistry, and the companies know it.

The Evergreening Problem

If patent cliffs were purely a function of the calendar, Indian companies would have an easier job. They aren’t. Innovator companies have become extraordinarily skilled at a practice called evergreening, or filing waves of secondary patents on minor tweaks to an existing drug (a new salt form, an extended-release version, a slightly different delivery device) to push the real patent expiry date by years, sometimes decades, past the original one. The WHO has described it as prolonging exclusivity in the absence of any real additional therapeutic benefit.

AbbVie, an American pharmaceutical company’s Humira is the textbook case. Its core patent expired in 2016. AbbVie built a thicket of more than 130 secondary patents around formulations, dosing and delivery devices, and US biosimilars weren’t allowed to launch until 2023. That’s seven extra years of monopoly pricing on a drug that had already crossed $20 billion in annual sales. Europe, with a less permissive patent regime, got its Humira biosimilars in 2018. The price gap between American and European patients for the identical molecule, for years, was the cost of a well-run patent wall. Generic makers describe these tactics of patent thickets, pay-for-delay settlements with rivals, brand migration to newer formulations as a deliberate toolbox, and research by UC Hastings’ Robin Feldman found roughly 80% of the 100 best-selling US drugs had secured at least one patent extension beyond their original term.

India, notably, has built some immunity to this. Section 3(d) of the Indian Patents Act denies patents for new forms of known substances unless they show genuinely enhanced efficacy. This was the clause that sank Novartis’s attempt to re-patent Gleevec in 2013, and that blocked Johnson & Johnson’s attempt to extend exclusivity on the TB drug bedaquiline in 2023. It’s a genuinely effective domestic safeguard. But it does nothing to stop evergreening on the other side of the ocean, in the US market that Indian generics actually need to enter to make real money, which is exactly why time-to-market, not legal cleverness, is the deciding factor in this cliff.

A Mass Producer, Not a Maker

India’s domestic pharmaceutical market is massive, valued at $60 billion in 2026 and projected to hit $130 billion by 2030. As the world’s third-largest producer by volume, it manufactures 60,000 generic brands and supplies 20% of global generics, earning it the nickname “Pharmacy of the World.” A more accurate title, however, might be “Drug Sweatshop of the World,” because this scale relies entirely on copying existing molecules cheaper and faster, not inventing new ones.

Consequently, India ranks just 11th globally by value. Smaller markets like Germany and the UK heavily out-invest India in innovation, pouring €9.6 billion and £8.7 billion annually into pharmaceutical R&D respectively. By contrast, Indian firms historically spend low single digits of their revenue on R&D (a fraction of the 15–20% committed by global innovators). The industry is world-class at reverse-engineering off-patent molecules, but it is not a place where new drugs are born.

This is the tragedy beneath India’s multi-billion-dollar “patent cliff” opportunity. Every dollar captured over the next five years will be earned through imitation, not invention. Big Pharma uses tactics like “evergreening” because innovation pays far better than duplication. Despite its massive manufacturing muscle, Indian pharma remains structurally trapped on the wrong side of that equation..

The Takeaway

The 2026–2030 patent cliff will be good for Indian pharma’s revenue. It is unlikely to be good for Indian pharma’s standing in the global hierarchy. Every cliff India climbs reaffirms the same role: fast follower, low-cost producer, dependable but never indispensable. The companies betting big on biosimilars like Biocon, Dr Reddy’s, Sun Pharma deserve credit for building real scientific capability in a genuinely harder category than the small-molecule generics of a decade ago.

However, until a meaningfully larger share of Indian pharma revenue comes from drugs the world didn’t already know how to make, the industry will keep winning battles it didn’t start, against patents it didn’t write, for molecules it didn’t discover. For investors, that means real but capped upside. For policymakers, it’s a reminder that R&D incentives, not manufacturing incentives, are the lever that’s been left mostly unpulled.

Until the next formula, ReadOn!