Covered Bonds: A Safe Investment Option?

Covered Bonds: A Safe Investment Option?

An explainer on why NBFCs are going gaga over Covered Bonds

When Covid struck us out of the blue, the last thing we wanted was a financial crisis. Of course, this responsibility fell on RBI’s shoulders. And to keep the economy running, RBI had to ensure that money was available for cheap. So, using its superpowers, RBI kept the interest rates low.

While low interest has boosted economic activities, it has also created trouble for Non-Banking Financial Companies (NBFCs).

When IL&FS (a big NBFC) collapsed a couple of years ago, the sentiments towards NBFCs turned negative. The trust in the quality of assets of NBFCs (the loans that they give, such as gold loans, vehicle loans, microfinance loans) also went down. Thus, it became difficult for NBFCs to borrow.

Then came ‘covered bonds’ to their rescue.

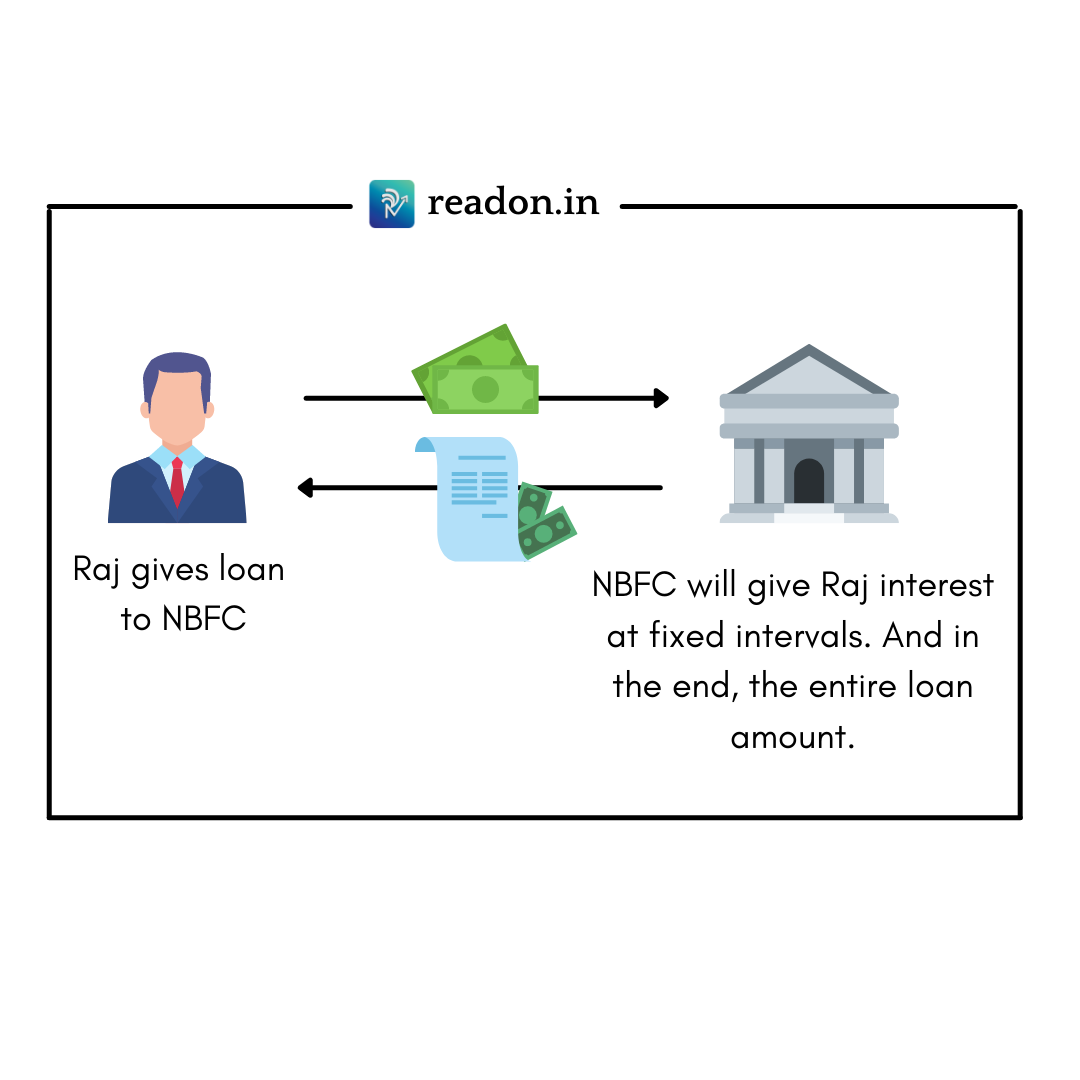

What are Covered Bonds?

Let’s say you have a lifetime savings of Rs. 20 crores and you want to loan out this amount to earn interest income. Now you go to an NBFC.

They will give you bond (loan) papers along with some coupons. At fixed intervals, you will be able to redeem interest with these coupons. And at the expiry of the agreed term, you will get the entire amount that you loaned to them.

Everything looks fine, right?

But what if the NBFC goes bust? What then?

You will have to queue up with the other lenders and pray that you get some bread crumbs.

On the other hand, if you put your money in covered bonds, the NBFC will create a pool of its assets and will keep this pool with a separate trust (sort of a mortgage). Now if the NBFC goes bust, you will have the first right to recover money from this pool of assets.

Sounds secure. But, here’s the twist: An NBFC's “pool of assets” also includes secured loans that it has given to someone else. This is also used as a “cover” for covered loans.

Now, this looks just like any other mortgage-backed securities. What’s so special about covered bonds?

In mortgaged-backed security, if the NBFC fails to repay, and you are unable to recover the amount from the asset that the NBFC had kept in the asset pool then you will have to bear the loss. But in covered bonds, the NBFC will have to ensure that the value of the asset pool should be sufficient at all times to meet the amount that it has borrowed from you. It will have to keep adding more assets if the value fluctuates. Now, even if the NBFC goes bankrupt, your asset value remains sufficiently guarded and you have the first right to recovery.

And because these instruments are so secure, they are given a higher credit rating than probably the credit rating of NBFC itself!

Now, so much security comes at a cost. Hence, the interest rates are lower for covered bonds, which also reduces the cost of borrowing for NBFCs. They get to overcome their liquidity problems and reduce their costs in one shot.

Sounds lucrative, right?

They are. And thus, Indian issuers have sold covered bonds worth Rs. 2,218 crores in FY2021 vs Rs. 25 crores in FY2019.

Looks like the perfect instrument, no?

Join us on WhatsApp to never miss an update! 👇

Well nice article but I was curious about some cases will the bonds NDFC buyer also come under pool of assets if so wouldn't it be problematic if the company by which bond is issued goes bankrupt or won't the value of tangible assets change with time and if loans are issued to normal people who are credit worthy but due to some unforeseen events like covid they can't return loans and their mortgage objects won't be enough to cover up that money what happens in these cases.

Thanks in advance.