China's Boba Bubble

China's Boba Tea is turning into a national phenomenon. How long before the bubble bursts?

At ReadOn, we don’t just report the markets. We help you understand what truly drives them, so your next decision isn’t just informed, it’s intelligent.

If someone told Indian mothers that their sabu dane ki kheer would be the centre of a $45 billion plus industry, they probably would not believe it. As it stands though, our sabu dana’s East Asian cousin Boba, has grown to be something of an international star! So far, this industry has created around 6 billionaires in China.

Clearly, the Chinese bubble tea or “Boba” is having a moment. As fast as it has grown though, this growth and its speed have become the industry’s problem.

Today, we take a look at Boba’s story. Its rise to fame and where it currently stands.

China’s Bubble Tea Boom

Bubble tea’s rise didn’t start in China. It began in Taiwan in the late 1980s, spread to Hong Kong, and by 2002 Singapore had about 5,000 bubble-tea stores. The drink caught on in mainland China first in the south, where tea drinking was already part of everyday life and tapioca desserts were common. From there it grew into a national market.

Today, the category is bigger than coffee in China. The number of brands rose from 1,60,000 in 2020 to more than 4,00,000 by 2025. China’s new-style tea market was valued at $48.5 billion in 2024 and is expected to reach nearly $51 billion, according to iiMedia Research.

To understand the scale, consider Mixue Ice Cream & Tea. What began as a street-stall ice-cream shop in Zhengzhou in 1997 has grown into what some call the world’s largest fast-food chain by store count. By the end of 2024, Mixue reported ~US$3.4 billion in revenue and $613 million in net profit. It completed a Hong Kong IPO in March 2025, raising around US$444 million and achieving a market valuation in excess of US$10 billion on day one.

You read that right. A tea chain that started selling ice cream on a street corner is now valued more than most established restaurant groups.

Its rivals saw similar investor interest. Chagee filed a US IPO for ~US$411 million, Goodme raised ~US$233 million in Hong Kong, and Auntea Jenny listed in May for ~$35 million. In terms of capital raised and market valuations, new-style tea has become one of China’s most active consumer IPO categories.

But there’s a twist. Back in 2023, China’s regulatory authorities had denied listing these brands. This was when the industry was actually booming.

But why did the regulatory authorities deny listing these companies? To answer this question, let’s start with what really made this boom possible in the first place.

What’s Driving this Boom?

The first and most important driver of China’s bubble-tea boom is what you might call the plug-and-play business model.

Bubble-tea chains didn’t grow because they invented a breakthrough product. They grew because they built a replicable system that thousands of franchisee owners could plug into almost instantly.

Most major brands run on a model where the franchisor controls the brand, recipes and supply chain, while the franchisee pays for everything else: the shop, the rent, the labour, the equipment and the daily operations.

A typical outlet needs low capital to set up, often in the range of ¥300,000 to ¥500,000 (~$70,000). For context, it costs more than $1 million to set up a McDonald’s franchisee. The ingredients come pre-measured and pre-mixed from central kitchens, equipment is standard across stores, and staff training takes only a few days.

On the brand side, the economics look even better. Since franchisees carry the biggest costs: rent, staff salaries, utilities, and equipment, the franchisor grows without taking on much risk. Most of their revenue comes from selling ingredients, collecting franchisee fees and supplying equipment.

That is why brands like Mixue can operate more than 50,000 stores while owning almost none of them directly. Compare it with Starbucks, which was founded in 1971. Starbucks took more than 50 years to reach around 40,000 stores globally. Mixue, which started as a small ice-cream stall in 1997, crossed 53,000 stores in less than 30 years. The difference comes down to the business model. Starbucks expands mainly through company-owned stores or tightly controlled partnerships. Mixue expands almost entirely through franchising.

Then there’s China’s manufacturing muscle. Supply-chain clusters stretching across Fujian, Guangdong, Zhejiang, Ningbo and Yiwu gave bubble-tea brands access to fast and cheap packaging and cold-chain equipment. When a flavour goes viral on Douyin (their Tiktok), factories can adjust recipes, tweak packaging and ship out materials to franchisees within days. Try doing that anywhere else in the world and the logistics just don’t work.

Digitisation pushed this even further. Chinese chains turned bubble tea into a real-time, data-led retail product. Mini-program ordering, automated loyalty systems, delivery-app integrations, and SKU-level performance dashboards allowed brands to spot trends instantly and launch new flavours nationwide in 10–14 days.

The Little Treats Economy

Another important driver of the boba tea boom is something behavioural economists call the “little treats” effect.

Have you ever caught yourself buying a small treat after a tiring day: something cheap, quick and comforting, even if you didn’t really need it? There’s psychology behind it. “Little treats” culture is rooted in positive reinforcement and self-care: small, enjoyable rewards that boost motivation, manage stress, and trigger dopamine release.

As growth slowed in China, youth unemployment climbed, and financial pressure increased for urban families, people began cutting back on big purchases but continued spending on small comforts. Economists often compare this to the classic “lipstick effect”.

A cup priced at ¥12–20 sits in a sweet spot: cheap enough to buy without thinking, comforting enough to feel like a reward, and frequent enough to turn into a habit. It’s the financial equivalent of a strategic retreat. Can’t afford that vacation? Here’s a ¥15 dopamine hit instead. And unlike the vacation, you can have it tomorrow. And the day after.

Delivery platforms made this emotional loop even tighter. Meituan and Ele.me, China’s Swiggy and Zomato, pushed constant discounts, turning bubble tea into high-frequency behaviour. People no longer needed to “go out for a treat.” A drink could be summoned to their desk or dorm within minutes.

But there’s a problem…

China’s bubble tea market grew “too fast”. The same drivers that powered the boom also pushed the industry into saturation much sooner than expected.

You can already see it on the streets. In Chengdu’s Taikoo Li, seven major chains sit within a five-minute walk. In Wuhan, some blocks now have a bubble-tea shop every two or three storefronts.

Even smaller cities like Luoyang and Yiwu, once considered high-potential markets, reached high store density in 2023–24 as franchisees rushed to open outlets before someone else grabbed the spot. New stores no longer grow the market; they split the same customers thinner. In some places, the same brand has different franchisees located 500 metres apart, each competing for the same customers.

A big reason is that the model is extremely easy to copy. Almost every chain offers a similar menu: fruit teas, milk teas, taro drinks, cheese-foam teas. When one brand launches a hit flavour, others replicate it within weeks. Grapefruit jasmine, taro milk, peach oolong, cheese-topped tea—these moved from signature drinks to industry-wide staples in a single product cycle.

Ask any 20 year old in Hangzhou to name their favorite bubble tea brand. Watch them struggle. They’ll tell you their favorite flavour, but the logo on the cup? Interchangeable.

This leads to what many Chinese analysts describe as “functional sameness”.

In economic terms, China’s bubble-tea market operates in a monopolistic competition: many players selling near-identical products under different branding.

In this kind of market, two things happen.

First, the number of competitors keeps rising because the entry barriers are low. Anyone with a few hundred thousand yuan can open a store. Ingredients are standardised. Staff don’t need specialised training. And suppliers will happily support new entrants because the supply chain makes money regardless of brand identity. This is why the number of bubble-tea outlets crossed 400,000 by 2025, everyone thinks they can open a shop.

Second, competition shifts to the only lever that’s easy to adjust: price. When every menu looks similar and every drink costs roughly the same to produce, chains fight on price because it’s the fastest way to attract footfall. Mixue, with its ¥6–10 drinks, pulled mid-tier players down. Those brands then cut prices further to avoid losing customers. In cities like Chongqing and Wuhan, entire neighbourhoods saw brands launch ¥9.9 daily menus, which triggered a downward spiral. Delivery platforms then added discounts of their own, pushing drink prices even lower while shrinking store margins.

This leads to what China calls neijuan or involution. It is unproductive competition in an overcrowded market where everyone works for the same outcome. It’s the treadmill problem. Everyone’s running faster, but nobody’s actually getting anywhere.

Brands now release new drinks every two or three weeks, sometimes hundreds of limited editions a year. Seasonal packaging, themed cups and social-media-friendly designs add constant operational load but don’t increase ticket sizes. Delivery apps reward paid visibility, so chains spend more on marketing without improving long-term demand. The industry is moving faster, producing more and spending more—but often earning the same or less.

Mixue shows how far this can go. Beyond drinks, it built a full IP universe around its mascot, Snow King. Since 2018, Snow King has become one of the most recognisable characters in China’s drinks market. The Snow King hashtag has passed 19.5 billion views, and the brand’s theme song has nearly 10 billion plays. Two animated series built around the character have earned hundreds of millions of views.

Offline, Mixue stages parades and in-store festivals that mirror the online buzz. Selling and Distribution expenses have been continuously increasing for the company. In just the first six months of 2025, Mixue spent 6.1% of revenue on Selling & Distribution Expenses.

But while the brand gains visibility, the pressure lands on franchise owners. Reaching a breakeven of 250–300 cups a day is becoming difficult in dense neighbourhoods. In cities like Hangzhou and Nanjing, franchisees report double-digit drops in footfall because new outlets open just blocks away and split the same customer pool. Many franchisees now have to spend extra on local marketing simply to stay visible in an overcrowded market.

Some Mixue outlets in Guangxi and Jiangsu closed within a year for this reason. In the first half of 2025 alone, 1,187 Mixue franchise stores shut down.

And remember: these are the winners. The chains that made it to IPO. Imagine what’s happening to the brands that didn’t.

This is exactly why Chinese regulators discouraged listing these companies back in 2023.

Using so-called window guidance, or non-binding requests, regulators discreetly advised that companies relying on explosive franchisee business models could not list locally, according to a person briefed on the matter. Food and beverage chains were reportedly among companies banned from listing in China’s main exchanges, according to Chanson & Co.’s Shen Meng, “especially projects that are burning money in order to surge in scale.”

“Unfortunately, almost all bubble tea makers adopt this business model,” the director at the Beijing-based boutique investment bank added. “Almost all bubble tea makers are in the red, so it becomes hard for them to meet standards of an IPO in the A share market.”

“Chinese food and beverage chains usually rely on quick expansion to achieve a large market share and pitch the story to investors as the exit strategy,” said Gary Ng, senior economist for Natixis in Hong Kong. “It also means that the corporate health of these firms may not be very sound with leverage, and the chains are usually highly replaceable if there are new, good competitors.”

The Bottom Line

China’s experience shows what happens when a category grows faster than its fundamentals. Saturation builds, competition intensifies, and store-level economics tighten.

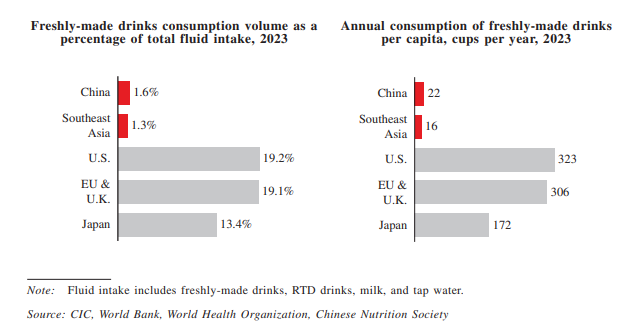

This doesn’t mean demand is weak. In fact, freshly made drinks still account for only 1.6% of total fluid intake in China, and annual per-capita consumption is just 22 cups, far below the US, EU or Japan. The market has plenty of room to grow.

The issue is not demand. It’s oversupply.

Mixue may have more stores than Starbucks, Dunkin or Tim Hortons, but captures only a small share (2.2%) of the market, while these global players command far higher shares with far fewer outlets. When too many brands chase the same opportunity, the pressure eventually shows, first in margins, then in franchisee returns, and finally in store closures. China has the demand to support long-term expansion. What it needs is market consolidation, sharper differentiation and rollout cycles that allow franchisees to recover their investments.

This context matters when looking at India. India is not facing China-level density. Clustering is visible: in chai chains, cafes, momo outlets and cloud kitchens, but the scale is still early. India’s food-services market is half the size, cities are more spread out, and the supply chain is slower. These structural factors naturally limit how quickly saturation can form.

Consumer behaviour adds another buffer. In China, bubble tea became a daily habit, helped by delivery discounts and dense retail. In India, purchasing is more value-driven, and daily repeat behaviour is much lower. That alone reduces the risk of a runaway bubble.

The real lesson from China is not that a bubble is guaranteed. It’s that early growth often hides structural weaknesses. Margins shrink, menus converge, and competition catches up faster than expected. The real test comes when categories reach density and the economics tighten.

Whether brands become long-term businesses or short-lived trends will depend on how they handle that moment. The China story shows what to watch: unit economics, store-level profitability, and how much risk sits with franchisee owners.