Big Steps for Micro Finance Institutions!

Big Steps for Micro Finance Institutions!

A recent RBI proposal can drastically change the landscape of microfinance in India. Here’s everything that you need to know.

As per Oxfam, about 10% of the Indian population holds 77% of the national wealth. If a minimum wage worker were to amass wealth equivalent to one year's salary of a top company executive, they would have to work for 941 years!

Yes. 941 years vs 1 year. That’s the gap between the poor and the rich in India.

One of the ways to reduce this gap is by enabling financial inclusion: by providing financial services and enabling small loans to the poor. They are trapped in a vicious cycle and the cycle needs to break. They are poor and so, they are denied loans. They are denied loans and so, they are poor.

And they don’t even need big loans. They just need “micro” loans to make their dreams come true! This impetus, therefore, becomes the tool for the poor to climb out of the well of poverty and narrow the gap of wealth distribution.

To this end, microfinance activities gained momentum in the early 2000s.

Anyone even vaguely aware of this sector will know that the government regulates this industry like nothing else! But, back in the day, this wasn’t the case.

In 2005, the then Governor of RBI, Dr. YV Reddy stated that:

Microfinance movement across the country involving common people has benefited immensely by its informality and flexibility. Hence, their organisation, structure, and methods of working should be simple, and any regulation will be inconsistent with the core-spirit of the movement.

But, its good intentions were marred by certain miscreants in the system. In 2010, 57 borrowers in Andhra Pradesh jumped to their deaths because of constant pressure from recovery agents of MFIs. Who was to blame?

Blinded by the greed to grow faster and faster, some MFIs overexposed themselves to risks. Proper due diligence was not conducted. Higher loans were given out. Ultimately, it was the borrower who suffered.

Now, RBI could not keep quiet anymore. The Non-Banking Finance Companies (NBFCs) that operated as MFIs were designated as NBFC-MFI and a regulatory framework was introduced for them in 2011.

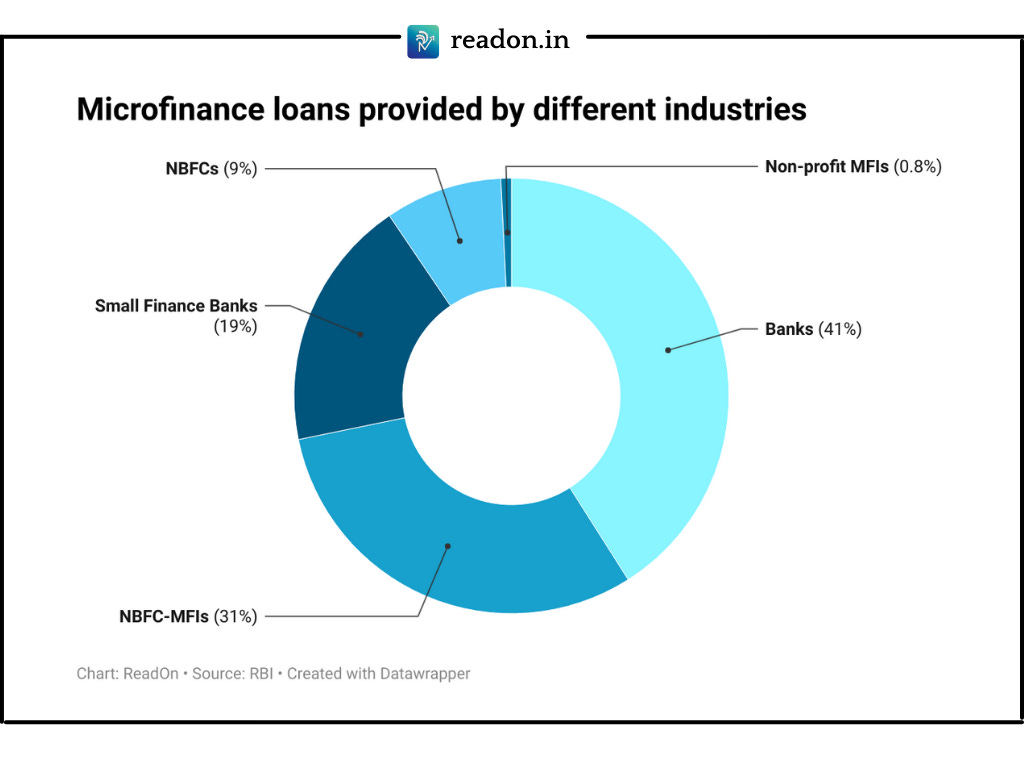

Well, regulations often lead to something unexpected. Now, a decade later, the NBFC-MFIs account for only 30% of the entire MFI loans outstanding. What about the rest? Take a look:

Yes, the remaining 70% don't fall under the framework. And the framework too has certain gaps. For instance, one borrower can only take loans from 2 NBFC-MFIs. So if you were a borrower, what would you do?

Go to other bodies and take loans, right?

But, this could overexpose you to loans that you might not be able to repay. And so is the case for all the small borrowers out there.

This led RBI to reimagine the system that will now be applicable to all Regulated Entities (RE) and not just NBFC-MFIs. The new regulation will not just focus on indebtedness by itself or indebtedness from only NBFC-MFIs. It has been designed to focus on the total indebtedness of these borrowers keeping their repayment capacity in mind.

First things first: What is a micro-finance loan?

Collateral-free loans (nothing will be kept Girvi) to households with an annual household income of:

> ₹1,25,000 for rural and

> ₹2,00,000 for urban/semi-urban areas.

Now, even the REs will need to earn income, right? What is the best way to safeguard the interest of borrowers while ensuring income for REs?

Earlier, the RBI had a maximum interest rate cap (ceiling) that the NBFC-MFI could charge. If the MFI’s cost of funds was say 12%, the maximum interest rate you could charge was 22% (cost of funds + 10% margin cap).

The margin cap (10%) was arrived at by considering the various costs that these institutions had to incur. Now, this law was also designed keeping the best interest of all parties at heart. But it led to an unintentional consequence. As per RBI’s report:

Lending rates of banks also hover around this ceiling despite comparatively lower cost of funds. Even among NBFC-MFIs, increasing size of the operations leading to greater economy of scale has not resulted in any perceptible decline in their lending rates. As a result, it is the borrowers who are getting deprived of the benefits from enhanced competition as well as economy of scale.

So, the RBI has decided to remove this ceiling altogether. They expect the market forces and competition to work in such a way that interest will spiral down and be a relief for the borrowers.

Also, to protect the borrower, RBI has introduced a cap. No borrower will be made to repay loan installments and interest amount more than 50% of their household income. This one move will keep many things under check. The amount of loan that REs give, and the interest they charge will be reasonable to maximize profitability while reducing risk for borrowers.

And, you know how complex it gets when you go to take loans. The interest rates are difficult to comprehend and the really important points are sometimes hidden from plain sight.

To prevent the borrowers from falling prey to such practices, a simplified fact sheet has been mandated by RBI to be provided by all REs-

Yeah. No beating around the bush. No playing around with rates. Everything has to be given in rupee terms so that the borrowers can make informed decisions.

The new proposed law looks strong. Watertight. It is being hailed as the watershed moment for the microfinance industry. But, that's the thing about laws. No matter how many situations you account for, the implementation surprises us in unimaginable ways.

Anyway, see you tomorrow. Until then, ReadOn.

Get a chance to interact with the creators of this piece by joining our WhatsApp list! 👇

❤

kuch na kuch to chootega hi