Borrowers, Beware

Borrowers, Beware

Are you often tempted to take loans and live your life the way you want? Watch your step, and read on.

“Hello, Sir. I am calling from a bank; would you be interested in a personal loan?”

How many times have you received such irritating calls? And how many times have you messed around with these call centre people just to kill time?

I sure have. Quite a few times.

Every time they call me, I wonder how good it would be to take that Rs. 10,00,000 loan and buy a cool car. And, impress that girl I always wanted to impress.

You think on the same lines too, sometimes, don’t you?

Before you get too excited, let me tell you a little more about loans.

A personal loan is money that you borrow and pay back with interest over multiple years. With the advent of credit cards, it has become all the more simple.

Had a bad day at the office? Just go to a bar and swipe away on that costly booze.

Had a fight with your significant other? Go to a hotel, swipe that card, and have the most lavish meal of your lifetime.

Had a fallout with your BFF? Just go shopping and swipe away!

Anyway, you live only once, right?

Wrong.

As the days go by, you forget the momentary pleasure of your spending spree, and are reminded of it the next month when the credit card bill stares at you. You realise that you spent a month’s salary on stupidity.

Huh.

Whether borrowing is a wise decision or not depends on what your financial need is. You don’t want to borrow money for something you don’t need, and then later sell off things that you do need to repay that loan.

Now that we have given you some context, let us look at the other side of the equation.

Why would someone “offer” you a loan in the first place?

Sometimes, when we are short of money, our friends come to the rescue, and ‘loan’ us some money. Without interest, obviously (keep them around, they are the good ones).

Note that your friends know you, and hence, the ‘risk’ that you won’t pay them back is almost negligible.

But, what’s in it for a bank / other bank-like companies (collectively known as financial institutions) to offer loans to you?

Banks are nothing but match-makers. They are the shaadi.com of the financial world.

The need for banks arose because of the existence of two types of people:

ones who had money, but no clue about what to do with it

ones who needed money, but did not have enough

Now, since the person giving you the money (indirectly) doesn’t know you, they take a risk, right? You may not pay back. That’s where the banks come into picture.

They act as middle-men; they do a quick assessment of your ‘credit-worthiness’ and rank you against other needy folks based on how easily they can get money back from you, and offer loans accordingly. The ones with lower risk of not paying back get money easily.

Note: The banks look at the ranking, but they don’t give the credit scores. That’s done by independent credit rating agencies.

Naturally, banks are not charitable. They expect you to pay back the amount loaned with interest.

Hang On. What’s a Credit Score and How Do I Improve Mine?

Think of your report card in school. I know, it may not be a very happy memory for some, but bear with me for a moment.

Now, what did that report card reflect? Your subject wise scores and overall class rank, right? And what do we understand from our subject scores? How we performed in which subject, and where we need to put more efforts going forward.

That’s essentially what a credit score is. It tells a lender, a loan giver, how well you have performed on certain parameters (credit history). These parameters include:

how much you have borrowed till date

how much have you repaid

whether you make your payments on time

Lenders use credit scores to assure themselves that they are not taking too much risk when they are loaning the money to you.

But, how to keep this credit score in check?

Just make sure you:

Borrow only as much as you need

Repay all the money that you have borrowed

And, repay them on time

One effective way to improve your credit score is to use your credit card for regular expenses, and keep the exact amount of money spent in your savings account. I am talking about smaller expenses here.

There are multiple benefits of doing this.

One, you get a lot of cashback offers on spending through credit cards.

Two, you earn one month’s interest on the amount you kept aside in your savings account against the purchases you made using that credit card.

Three, you have enough money to pay off your credit card bills at the end of the month (on time), and thereby, improve your credit score.

Beware!

Interest rates on these credit cards could be as high as 36% p.a.

“Oh, please. I was offered 3% as interest charges by that call centre guy.”

Well, you know nothing, Jon Snow.

The sad truth is that most of us get duped by such marketing gimmicks. It’s best to read your credit card documents at least ten times to understand whether it’s 3% per month (36% per annum) or 3% per annum. Don’t let incomplete information fool you.

Look at the graph above carefully. As your credit score increases, the interest that banks charge from you decreases. Why so?

Since a person with a good credit score is likely to repay the money back on time, banks trust them more, and the risk that the banks take is lesser. They are sure that you won’t run away.

On the other hand, when we look at the group of people with bad credit scores, there is a chance that some of them would run away. Therefore, in order to cover that loss that the banks may incur in case someone runs away, they charge more interest from this group of people.

Believe me, a bad credit score can haunt you for a lifetime.

It is like that stain which cannot be removed from your financial history. Take absolute care. Please.

Now that you understand loans, lets see how we can use it to our advantage.

It is always better to save upfront for whatever large expenditures you want to make, rather than relying on loans.

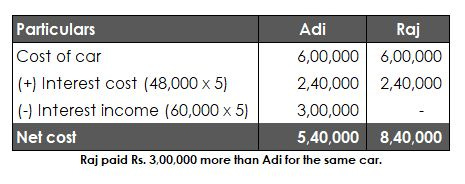

Let me tell you the story of two friends, Adi and Raj.

Adi and Raj got placed at the same company, and were getting a salary of Rs. 1,00,000 per month.

Both wanted to buy a car that would cost Rs. 6,00,000. Adi suggested that they save Rs. 50,000 per month and invest it at 10% per annum. Raj, being the spendthrift and carefree person that he was, ignored Adi, saying, “We will see when the day comes, buddy. Worry not. Just chill.”

One year later, they both went to the car dealer to buy that dream car. The car dealer said, “You can purchase this car using a loan of Rs. 6,00,000. Interest on the same would be 8% per annum. That is, Rs. 48,000 per year. You have to repay Rs. 6,00,000 at the end of 5 years.”

Both of them took the loan. But, Adi was financially way better off than Raj.

How?

Adi was getting Rs. 60,000 (10% of Rs. 6,00,000 saved) as interest from his savings, and was paying only Rs. 48,000 as interest. He was getting richer by Rs. 12,000 per year.

Raj had to pay the entire interest amount from his salary. He had no income from his savings to pay for his purchase.

This is what happened.

Adi created an asset (the savings in his bank account), a cash-generating one, and used the cash coming from this asset to pay off the loan on the car. As long as the cash coming in was greater than the cash going out, Adi was getting richer.

Raj, on the other hand, was losing wealth every year.

The net cost of the same car for each was:

Here, to keep the math simple, we have ignored the additional interest Adi could earn on the extra Rs. 12,000 that he was saving (wondering how compounding works? Here).

Adi let money make more money for him. He made money his slave.

Poor Raj had to work extra hard to ensure he gets a promotion, and more salary, to be able to pay off that interest burden that he had now.

Lesson: Always try to create assets, and spend from the income generated by that asset. The asset generates income for you in silence, day in and day out, and you don’t have to worry about how to meet that next interest installment.

Also, it makes sense to check that the income that your asset generates is higher than the expenses that you make. In our example, Adi is making 10% income, while he has to pay 8% interest. Hence, he could increase his wealth by net 2%.

Had the interest on loan been > 10%, say 12%, it would make sense for Adi to not take the loan, and buy the car by paying the full amount upfront (else, he would have lost 2% every year).

To summarise, when

Income from asset > Interest on loan => take the loan

Income from asset < Interest on loan => do not take that loan, unless it is an emergency

At the end of the day, the decision is in your hands - whether you want to be like Raj, and work for money, or be like Adi, and make money work for you.

True financial independence comes when the income that your assets generate covers all your expenses, regular or irregular.

A Word of Caution

Some people spend a lifetime trying to pay off their debts. Add to that the stigma associated with not being able to return borrowed money. Families fall apart; wealth accumulated over generations is destroyed by a single stroke of that pen. Dreams of that child are shattered, who labours away at a job she hates, just to pay off the debts of her father.

Beware, borrower, for you and your kin shall be bound to economic slavery, if you are quick to borrow and spend.

Think before taking a loan. Long and hard. Think again.

Financial freedom is what you aim for. Financial freedom is what you will achieve. And we promise to be your silent, watchful protector. But that's all we can do. The ultimate decision is yours. Isn't it?

Thousands of readers get our daily updates directly on WhatsApp! 👇 Join now!