A World Without Central Banks?

Everyone knows how economies need central banks, but what if we didn't?

At ReadOn, we don’t just report the markets. We help you understand what truly drives them, so your next decision isn’t just informed, it’s intelligent.

Every six to eight weeks, a six-member committee at the Reserve Bank of India debates the state of the economy and makes a call on the repo rate. It’s the single most important number in Indian finance. In December 2025, the RBI’s Monetary Policy Committee cut that rate by 25 basis points to 5.25%, nudging down the cost of borrowing for over a billion people. It is a deliberate, conscious act of monetary management, pulling one lever here, watching the ripple there.

What if India’s central bank simply did not do that? What if, instead of the RBI deciding how much money flows through the economy, the market just... decided on its own?

That is not a hypothetical. It is, more or less, how Hong Kong works. Let’s find out about it.

The Machine That Runs Itself

Hong Kong’s central bank, the Hong Kong Monetary Authority (HKMA), does not set interest rates the way the RBI does. It does not decide how much money should exist in the economy. That function, in Hong Kong, belongs to the balance of payments. In other words, if money flows into Hong Kong, the money supply expands. If money flows out, it contracts. Automatically, without a committee vote.

The engine behind this is the Linked Exchange Rate System (LERS), introduced in October 1983 and still running today. The Hong Kong dollar has been pegged to the US dollar at a fixed rate of HK$7.80 to US$1 ever since. The HKMA commits to buying or selling US dollars at that rate unconditionally. When demand for HKD rises, and the exchange rate strengthens to HK$7.75, the HKMA sells HKD and buys USD, expanding the monetary base and pulling interest rates down automatically. When the HKD weakens to HK$7.85, it buys HKD back, shrinking the money supply and nudging rates up.

The adjustment happens through the Aggregate Balance. These are the clearing accounts that Hong Kong’s commercial banks hold with the HKMA. When it expands, rates fall. When it shrinks, rates rise. No committee. No vote. Just math.

This is what economists call a currency board, or a monetary system where every unit of local currency is fully backed by foreign exchange reserves, and the central bank’s hands are tied by rule rather than freed by discretion.

How the System Was Built

The LERS did not arrive fully formed. It evolved through three distinct phases, each one adding a layer of institutional muscle.

Phase One (1983) was born from a crisis. Political uncertainty over Hong Kong’s future sent the Hong Kong dollar spiralling — it hit a low of HK$9.60 to US$1 in September 1983, having depreciated sharply from HK$6.50 at the start of that year. The government re-established a currency board on October 17, 1983, pegging the dollar at 7.80. The crisis stopped almost immediately. But the architecture was loose. HSBC, as the dominant note-issuing bank, effectively controlled the clearing system, blurring public and private interests uncomfortably.

Phase Two (1988) addressed that. New Accounting Arrangements required HSBC to hold a balance directly with the Exchange Fund, giving the monetary authorities their first real tool to influence the money market without relying on HSBC’s cooperation. Exchange Fund Bills and Notes were introduced for open market operations. The system gained its first real institutional backbone. Later, in 1993, the HKMA itself was formally created, and by 1996, the Aggregate Balance reform required all banks (not just HSBC) to maintain clearing accounts with the HKMA, ending the anomaly of a single private bank holding de facto monetary authority.

Phase Three (1998) came after the Asian Financial Crisis. It was the system’s most severe stress test. Speculators attacked the HKD and the Hang Seng simultaneously, shorting both the currency and stock futures. The HKMA controversially intervened in the stock market, spending HK$118 billion (US$15 billion) to defend the peg. In September 1998, a package of seven technical measures transformed the system into its modern form, including an explicit convertibility undertaking at HK$7.75 and a “Convertibility Zone” (the band of HK$7.75–7.85) within which the exchange rate floats today.

How It Is Working Right Now

In 2025, the system faced a different kind of pressure. A weakening US dollar and heavy capital inflows caused the HKD to appreciate sharply, hitting the strong-side limit of 7.75. The HKMA responded by selling a historically large HK$129.4 billion in HKD to defend the band, causing the Aggregate Balance to expand fourfold, pushing local interest rates to near zero. This created a US-HK interest rate differential, incentivising traders to borrow cheap HKD and park it in US dollar assets. The HKD is now sitting near the weak side of the band.

None of this required a policy meeting. The machine adjusted itself.

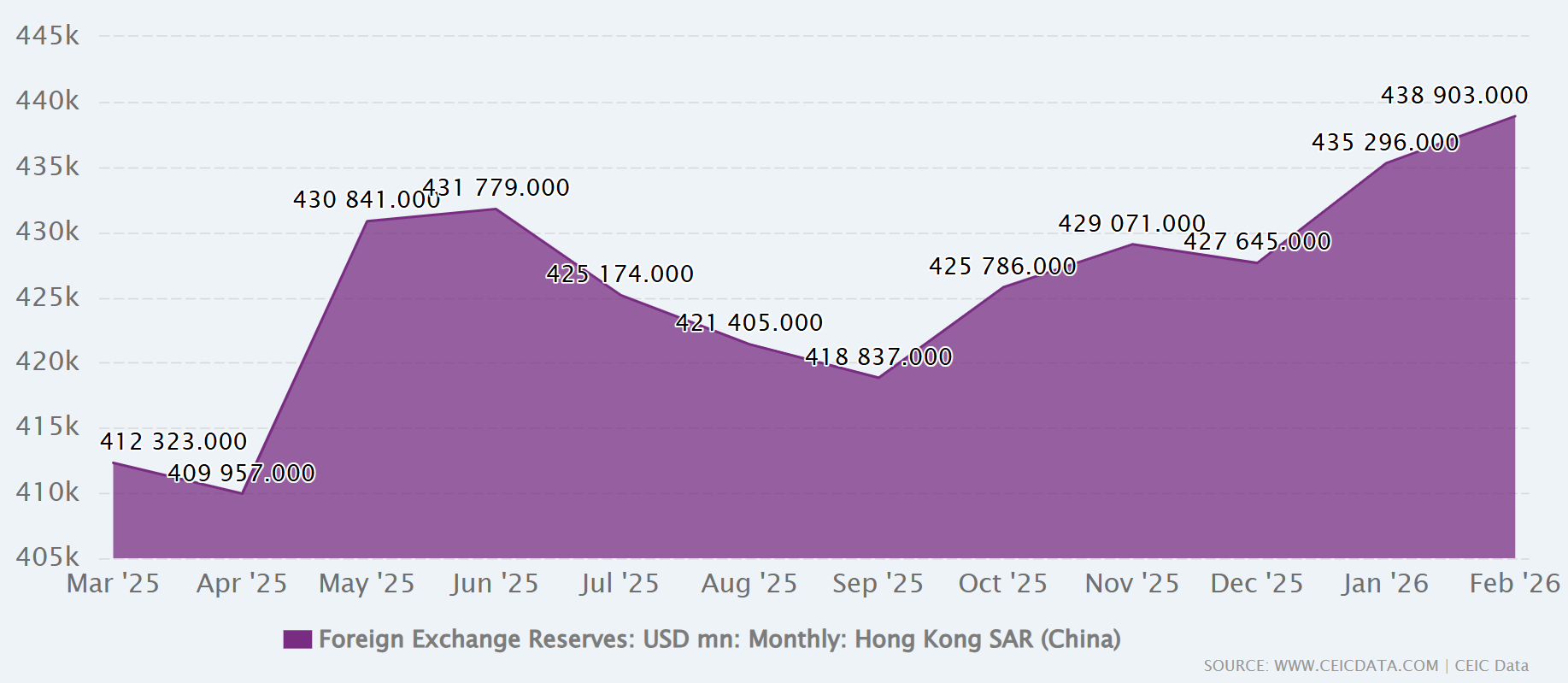

Backing all of this is Hong Kong’s formidable war chest. By December 2025, the territory held US$427.6 billion in foreign exchange reserves. That’s over five times the currency in circulation and about 37% of total HKD M3. The system’s credibility rests entirely on this buffer.

Source: Foreign Exchange Reserve 2000-2026

Could India Run Such a System?

The honest answer is: possibly, but the tradeoffs are brutal.

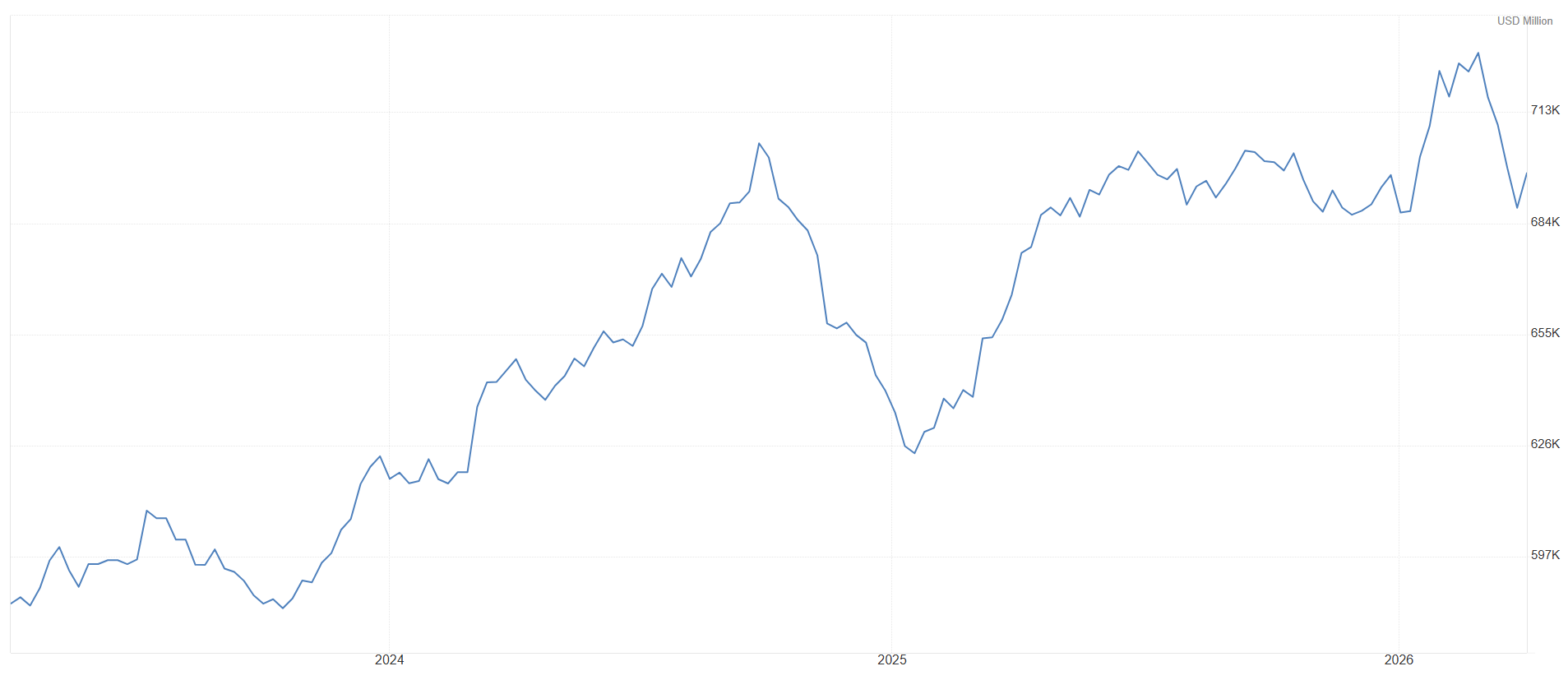

The arguments in favour are interesting. A currency board would eliminate the risk of politically motivated monetary policy. It would import credibility, pegging to a stable anchor currency forces fiscal discipline on the government, since the central bank cannot lend to the deficit. The IMF’s analysis of Argentina, Estonia, and Hong Kong suggests that in all three cases, the currency board arrangement played a meaningful role in stabilisation. India’s own forex reserves stood at over $680 billion in early 2025, which, on paper, could provide significant backing.

Source: Indian Foreign Exchange Reserve

But the costs are significant. Under a currency board, India would forfeit the RBI’s most powerful tool, which is the ability to set interest rates. The 25 bps cut in December 2025? Gone. The rate adjustments made during COVID-19, or the 2013 taper tantrum, or the 2008 financial crisis? All of those would have been off the table. The system’s stabilising mechanism of rising interest rates when money flows out can be punishingly sharp. During Hong Kong’s 1998 crisis, the overnight interbank rate spiked to the equivalent of 85% per annum for several days. India’s mortgage borrowers and MSMEs would find that excruciating.

Then there is the structural mismatch. Hong Kong is a small, extremely open, dollar-integrated economy with free capital movement and one of the world’s deepest financial markets. India is a large, diverse economy with a current account deficit, active capital controls, and hundreds of millions of citizens whose livelihoods are sensitive to credit costs. Hong Kong’s inflation has also remained consistently above US inflation since 1983, a structural feature of currency boards that squeezes competitiveness over time and would be particularly painful for a developing economy still building its manufacturing base.

The deeper issue is that a currency board does not eliminate monetary problems. It relocates them. Instead of interest rate volatility, you get exchange rate rigidity. Instead of central bank discretion, you get balance-of-payments vulnerability. The gain in credibility is real, but so is the loss of flexibility.

The Takeaway

Hong Kong’s currency board is a remarkable piece of institutional engineering. It’s a monetary system that has held for over four decades, survived a financial crisis, and maintained the territory’s status as a global financial hub. For India’s investors and policy-watchers, it is worth understanding not as a template, but as a lesson in the cost of commitment. Every monetary system involves a trade-off between control and credibility. Hong Kong chose credibility. The question for India, with its scale, its development needs, and its political complexity, is whether it could ever afford to make the same choice.

Until the answer is found, ReadOn!

Brilliant breakdown. HK’s LERS is basically the original 'Code is Law' for monetary policy. It’s the ultimate case study for anyone building stablecoin infrastructure today.

Always learning new stuff on here, great work!