A 795% Return in 10 Months: How?

Happiest Minds has been creating happy returns for its investors. What’s behind this bull run?

Happiest Minds, an IT consulting and services company, got listed on the Indian stock exchange just about 10 months ago, in September 2020. It gave a massive listing gain of 111% and is not showing signs of slowing down anytime soon.

To this date, the company has given a super-high return of 795% (at pre-listing price). What is it about Happiest Minds that people are going crazy about?

Read on.

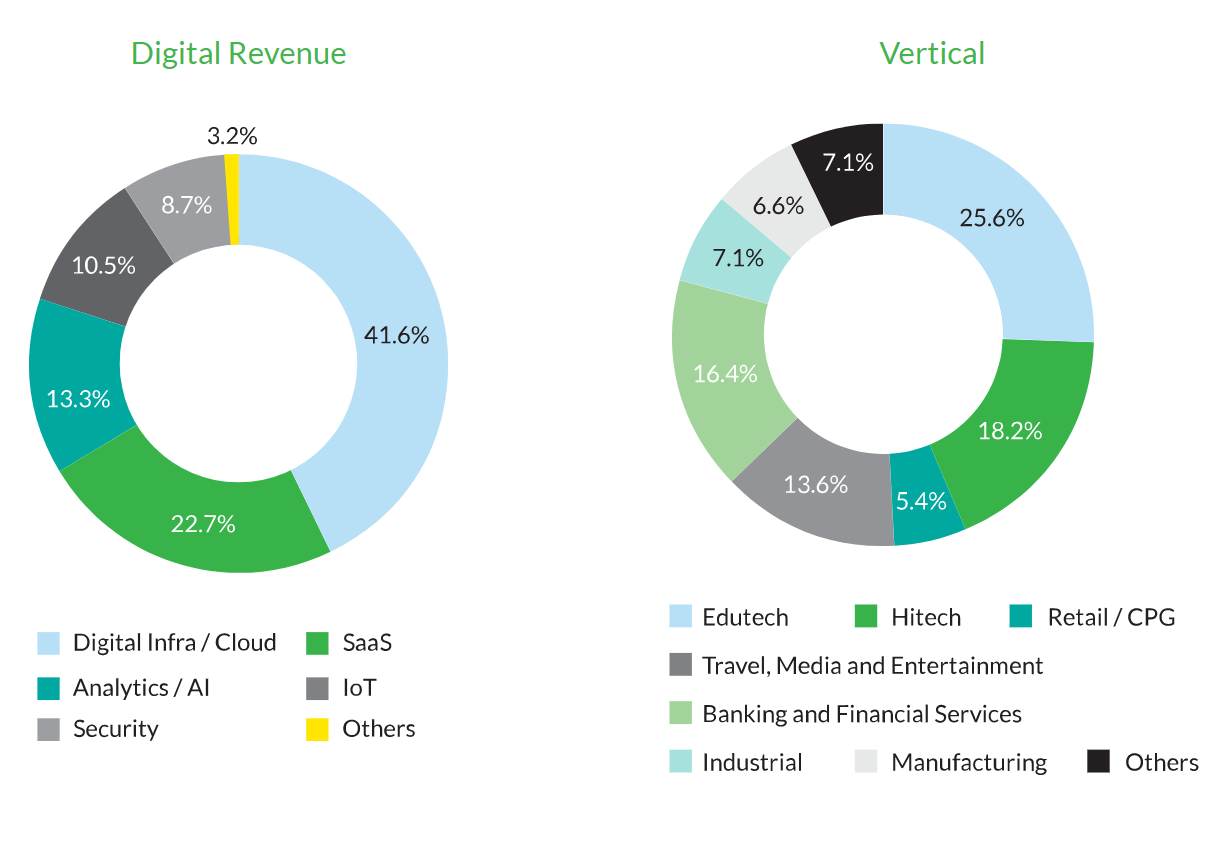

Happiest Minds provides services to companies from the most lucrative industries such as Edtech, Banking and Financial Services.

Tapping the gold mine, is it?

If its target audience is a gold mine, its array of services is its shovel. Everything that these modern-day gold mines need, Happiest Minds has to offer.

Data storage and security are basic needs. Building on that, companies also need analytical capabilities to churn the vast amount of data that they have gathered into valuable insights. And well, daily operations of apps and software need some form of servicing and tech-enablement all the time. Happiest Minds keep their customers happy by solving for all of these.

They have cloud hosting for data storage, Analytics/AI for making the data sing, and SaaS and IoT for the smooth working of a modern-day tech company.

Source: Happiest Minds Annual Report FY 2021

The competition is immense, and it all comes down to the quality of service that one offers. But it’s not a ‘winner takes it all’ kind of industry. Their collective growth depends on the industries that they are catering to. And these industries are just getting started, with an expected CAGR of 25%-30% this decade. This hope for future growth has led to happy stock market gains for Happiest Minds at the stock market as well.

Enough about the future now. Let’s come back to reality. Because the service industry is hinged on execution, how well has Happiest Minds executed its business so far?

It currently caters to 173 clients, 46 of which are valued at USD billions spread across the 7 geographies.

However, the mid-scale Indian companies are not completely open to experimenting with these services. And the big companies that are actually interested, prefer doing it in-house. Hence, India accounted for only 11.8% of Happiest Minds' total revenues.

But slowly and steadily, it is overcoming this challenge too, by partnering with some of the biggest tech companies of the world, such as Google, AWS, Salesforce and Microsoft.

The team of Happiest Minds is composed of highly experienced and respected executives. One of them being Ashok Soota, Executive Chairman of the company. He had previously led Wipro for 15 years, and later was among the founding members of Mindtree (no prizes for guessing that Mindtree’s IPO was a success as well!). Given his wonderful past records, there is no doubt that his presence lends credibility to Happiest Minds.

Good services: Check ✓

Good opportunities: Check ✓

What else?

Good Spirit!

Happiest Minds is recognised among the top 25 Best Examples of Digital Transformation over multiple years by the leading global technology research and advisory firm, ISG.

One of the reasons for its work getting recognised is its mindful approach towards work culture. Happiest Minds made it to the list of India's best companies to work for in 2021 ranking #21 announced on June 18. Since then, the stock price has been trading up by 70%.

But, with the breakthrough stock performance, came concerns for valuations. Are we being too optimistic about the company?

The stock price relative to its earnings per share (PE) is 133. This is well beyond the industry average if you compare it with the likes of Cyient Ltd and Zensar Technologies Ltd.

The company is also treading some risky grounds:

It has a very small portion of its revenue in Research & Development (R&D) expenses. It fell from 2.13% in FY20 to 1.82% in FY21. Doesn’t this mean stagnation from future growth? If its competitor makes an interesting tech-breakthrough, will Happiest Minds be able to tackle that?

Revenue concentration imposes another threat to the company. The top 20 clients contribute 64% to its total revenues. What if it were to lose any of them?

What if more and more companies become self-reliant and stop outsourcing these services to companies like Happiest Minds?

It faces severe competition from major global companies like Cognizant, IBM, Accenture etc. It is difficult for Happiest Minds to acquire the big clients as they prefer the traditionally established competitors of the company.

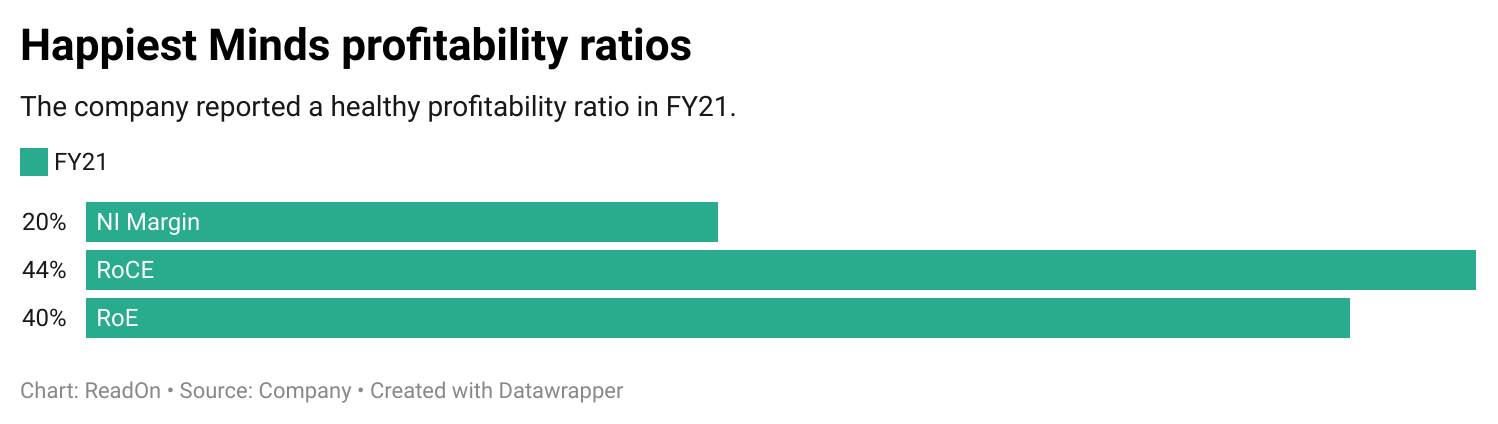

Well, the company has posted some really sound results and has been able to manage these risks pretty well.

The company has been more than doubling its net profits for the last 3 years. Its 2 years net profit CAGR is 238%. The company has recently been very successful with its profitability, but the revenues growth remains a concern with a CAGR of only 15%. The growth in profits was majorly met through cost-efficient operations. This is a positive factor for the company but without the growth in revenues, will the high profits even sustain? What’s in store for Happiest Minds?

Until next time…

Why just read? Come, and have a fun chat with the creators of the piece by joining us on WhatsApp (yes, it’s operated by humans and we love talking to you!)