📈 What's Behind Brightcom's 3,000% Returns?

Brightcom Group's shares gave over 3,000% returns in the last year. But does that mean you should buy its stocks?

One common warning that is given to investors is to stay wary of penny stocks (or small-cap stocks that are priced at around less than Rs. 100).

These stocks are often a risky bet (here's why). But they're also the dark horse of the investing world. If you can in fact find that needle in the haystack, you could become a millionaire overnight.

And one such penny stock that has made many investors millionaires is Brightcom Group.

If you had invested just Rs. 50,000 in the company a year back, you would now have Rs. 16,00,000. But what's driving this company's insane growth?

Analysing Brightcom Group's Rally

The company's shares have grown 3131.25% in just the last year. This is almost equivalent to the insane returns some cryptocurrencies give. What’s behind it?

Before we get into all that, let's take a look at what Brightcom Group does.

The company provides comprehensive digital marketing services to several companies across the world. It has two major divisions: digital marketing (which accounts for the majority of its revenue) and software services.

And before you scoff and think, "Oh, it's just another marketing company," here are some of Brightcom's clients: Coca-Cola, Airtel, LIC, ICICI Bank, British Airways, Hyundai, Sony and Unilever.

Not just that, it is now also entering the audio advertising industry.

Things started adding up yet?

The company has been in the business since 2000. But the recent rise in digital media and marketing, especially amid Covid has given it a major boost!

And the recent interest in the metaverse, which will basically take our lives online, is expected to further increase the company's sales.

But well, we'll let the numbers do the talking.

The company's net profit grew by 168%, from Rs. 139 crores in the December 2020 quarter to Rs. 371 crores in the December 2021 quarter and its net revenue grew 130% from Rs. 878 crores to Rs. 2,021 crores.

What’s more? The company is debt-free!

Plus, it has been raising funds lately. It issued 33,18,45,000 share warrants at Rs.7.70/warrant during the June 2021 quarter. This meant that the company was looking to aggressively deploy its funds and grow.

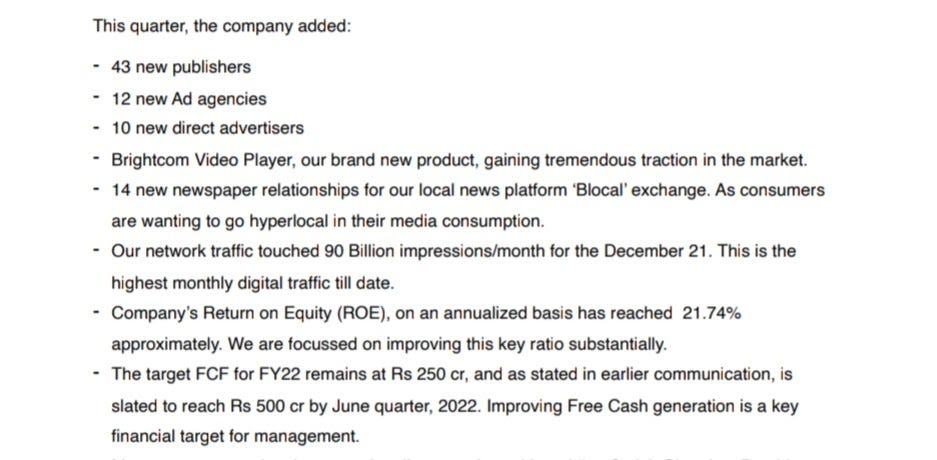

Take a look at all it has achieved this quarter (a snip from the quarterly report of the company):

Impressive, huh?

But that's not all. You see, one of the company's main aims is increasing value for shareholders.

The company has been consistently paying dividends since 2011. Not just that, to celebrate its great earnings report it recently announced that it will issue bonus shares in the ratio 2:3.

That means for every three shares of Brightcom you own, you will get two extra shares.

A great deal, right? The company had also issued such bonus shares last year.

This has brought down the company's stock price from its all-time high of Rs. 191. However, that was inevitable. Because any time you issue extra shares, you increase the supply of shares in the market, which decreases the value.

This could be good news for many retail investors who can now buy the stock for cheaper.

But before you rush to press the buy button, take a look at the other side of the story.

The Other Side of the Story

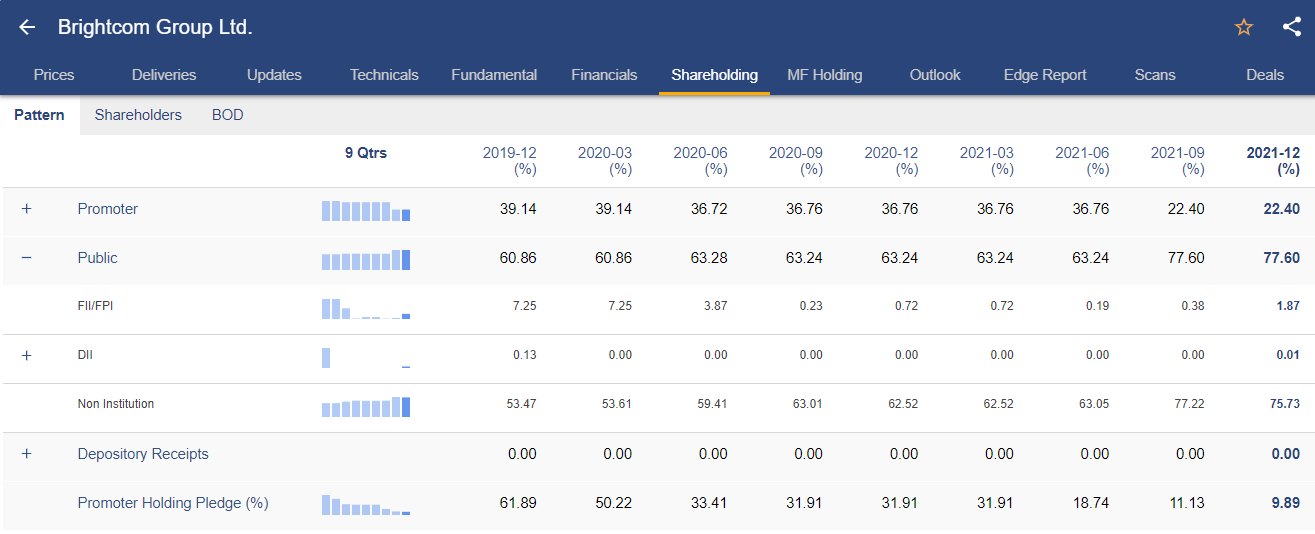

While the company looks to be promising from all aspects, promoters holding has fallen from 39.14% in March 2020 to 22.40% now. And holdings of Foreign Institutional Investors have fallen from 7.25% to 1.87%. What has made the promoters book profits?

Also with increased retail participation, the stocks have the potential of being more volatile, hence susceptible to a fall.

And the massive increase in sales and revenue that the company has seen could just be a result of the holiday season in the October-December quarter. The company may not be able to replicate this anytime soon.

Moreover, the company's employee benefit costs have almost doubled from Rs. 6,543.42 lakhs in Q2 to Rs. 11,330.92 lakhs in Q3. This means the company has massively increased its workforce to drive more sales.

Now, this is a permanent expense which was somewhat negated by the crazy sales the company saw in the December quarter. But if it is not able to generate sales on the same scale next quarter, this massive expense could drive down profits.

This could very well end the investor optimism that is currently boosting the company's share price, causing it to fall. Last January Brightcom was trading at Rs. 5/share as not many had invested in it then. But now it is trading at Rs. 180.95/share (as of 3:30 pm on January 28), thanks to news about its amazing returns. Hence, some analysts are calling the stock overvalued.

So is Brightcom’s future bright or is its share price headed for a fall?

Let us know what you think on Twitter (we’re trying to grow our handle, need your support 🙏🏻)

Disclaimer: This is not investment advice. Only meant to educate.

Update (March 1, 2022)- Update: Looks like we weren't the only ones who thought something was fishy about Brightcom's crazy growth. Last September, the SEBI had ordered a forensic audit of the company's books. Why are we telling you this now? Because the company itself just made this information public. But why the audit? SEBI has found discrepancies in the public disclosures that the firm has made, which could be bad for investors. So, it has now appointed an auditor to look through the company's books from FY15-FY20 and check for any manipulation or siphoning off of funds. Brightcom had claimed the audit was not necessary but SEBI has stuck to its guns.

You can also listen to our stories because the Revolution ReadOn podcast is live!! Here: you can catch it on Spotify, Apple Podcast or Amazon Music, Google Podcasts, Gaana and Jio Saavn.

If you are coming here for the very first time: Don’t forget to join us on WhatsApp to get daily updates! 👇