🤨 Should You be Excited About Digital Rupee?

🤨 Should You be Excited About Digital Rupee?

India is finally launching a CBDC but how will that impact our current payments system?

The number one talking point of this year’s budget was the introduction of the Digital Rupee.

Yes, after a long-drawn love-hate relationship with cryptocurrencies, India is finally accepting that they may have some merit.

But, it is still not ready to trust just any cryptocurrency.

So, it is launching its very own central bank digital currency (CBDC) in 2023.

Wondering how this will impact you and me?

ReadOn!

The CBDC Fever

An outdated payments system has increased the adoption of cryptocurrencies.

While many are drawn to crypto because they are a faster, more efficient and more private payment method, others are into it from an investment perspective.

But since cryptos are not yet widely accepted and still relatively new, they are very volatile.

Plus, they can easily be used for money laundering as transactions are untraceable.

Also, many cryptos leave people vulnerable to scams, where you can lose your entire life savings.

So, for governments across the world, the massive adoption of cryptocurrencies became a pain point.

Not just that, they were worried that if everyone started using these private cryptocurrencies, the government-owned currencies would decline in popularity and value.

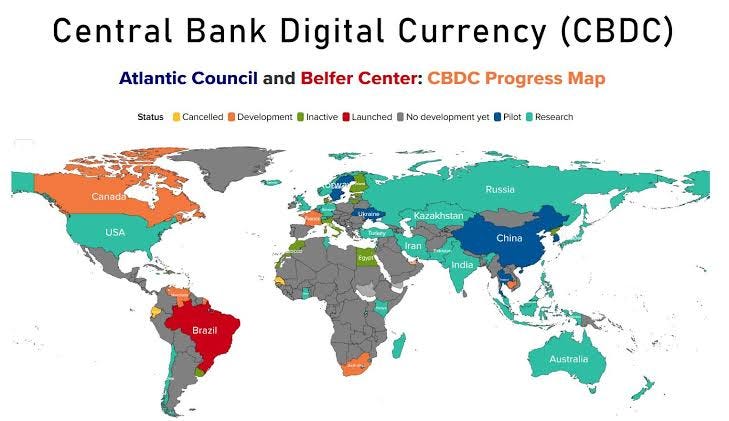

So, they came up with CBDCs. 87 countries are currently exploring CBDCs, and 9 have already launched some version of a digital currency. And now India is one of them.

The idea of a CBDC is a sweet rip off of the cryptocurrency model – both rely strongly on encryption.

They will be built on a blockchain just like normal crypto and will work exactly like the present-day cash, only... digital. Imagine apes turning into humans. That’s it. Digital currency is the natural evolution of money.

But unlike normal cryptos, they won't be volatile. The price of one Bitcoin differs from day to day, but the price of one Digital Rupee will largely remain the same. This is because the Digital Rupee (and other CBDCs) derives value from our physical currency, which is pegged to the US dollar.

So, the Digital Rupee and CBDCs, in general, will sort of function like stablecoins.

The Pros of a Digital Rupee

If you're thinking that the Digital Rupee is just like digital payments and won't make much of a difference, you're mistaken.

The Digital Rupee has the potential to completely transform our payments systems and solve their existing problems.

For one, it'll make things much easier for the government. It won't have to waste time, effort, and money in printing so many currency notes.

Secondly, it will eliminate the need for bank accounts. The current digital payments are linked to the money you have stored in your bank. But the Digital Rupee will be stored in an app on your phone.

So, even those without a bank account will be able to use digital payments easily. And this is a big deal for India where over 190 million adults don't have a bank account. We are the world's second-largest unbanked nation.

This will also protect people from bank fraud and help them keep their money safe.

Plus, cross-border payments and remittances are still a major hassle as banks depend on intermediaries like VISA cards, settlement institutions, and clearinghouses to transfer and redirect funds amongst each other.

But CBDC transactions can take place easily and quickly through the blockchain without any intermediaries. This will make remittance transactions much more affordable for us.

Also, CBDCs could be a great tool to eliminate corruption. Every step and node of CBDC is traceable and unhackable, so with CBDC, we won’t need a demonetisation. The government will legally be able to track and monitor every transaction and our politicians with black pockets will resign immediately (but let’s not daydream of utopia yet).

With easy tracking of digital footprints, there’d be a significant increase in tax collection with a swift leeway into new, innovative ways of providing financial services. The governments would (finally) know how to better their monetary and fiscal policies. In fact, they could tweak them on a day-to-day, hour-to-hour basis, bringing an unprecedented level of precision to monetary management.

All this sounds great, right? But well, every coin has two sides. So, let's flip the coin and see what it holds.

The Cons of a Digital Rupee

The first and the foremost concern that people have with the Digital Rupee is that it will infringe on their privacy. The government will be able to track and record every payment you make. This is literally the opposite of what people want from a cryptocurrency.

Okay, ReadOn but I don't have anything to hide. So, how will this impact me?

Well, you see the government could build this CBDC on a permissioned blockchain just like China. Through this permissioned blockchain, it could dictate where and how you spend your money.

In fact, it could rule that you have to spend a certain part of your income to ensure enough liquidity in the economy at all times.

Scary, right?

Plus, this model could be disruptive. Too disruptive. It could cause a lot of companies, especially fintech firms, to either go out of business or change their business models.

The biggest disruption will be in the banking system.

Just imagine, if a majority of the people stop depositing money in the banks, how will they extend loans? They would have to increase interest rates. Some banks could even have to completely shut down. This could end the banking industry as we know it.

And we're not making these reasons up. The UK government conducted research on CBDCs and these are some of the cons the report mentioned.

Plus bringing all the money onto a blockchain will be a mammoth task. And if the entire money in circulation is not on the block, issues such as corruption, income escaping taxes, terror funding will persist.

But before you start dreaming of a CBDC utopia or a CBDC dystopia, let us tell you that a lot of decisions still need to be taken, like whether CBDCs will give interest or not. We will need to find a fine balance and several countries may just need to, for once, come together instead of racing ahead to formulate a working CBDC system.

Let us know your thoughts about CBDCs on our Twitter handle.

Share this with your friends via WhatsApp or Twitter and help them become financially smarter! See you tomorrow :)

You can also listen to our stories because the Revolution ReadOn podcast is live!! Here: you can catch it on Spotify, Apple Podcast or Amazon Music, Google Podcasts, Gaana and Jio Saavn.

If you are coming here for the very first time: Don’t forget to join us on WhatsApp to get daily updates! 👇