😲 Indian States In Big Trouble?

😲 Indian States In Big Trouble?

Indian states' debt and fiscal deficit are growing at an alarming rate. Here's why.

For the longest time, we have been looking into the financial and economic status of India and other 'countries'.

But there’s one aspect we have ignored: the financial condition of the states.

However, the recent default by Sri Lanka (you can read more about it here and here) has forced the RBI to look into this aspect.

And what it has discovered doesn't exactly portray a rosy picture.

🔎 The State of the States

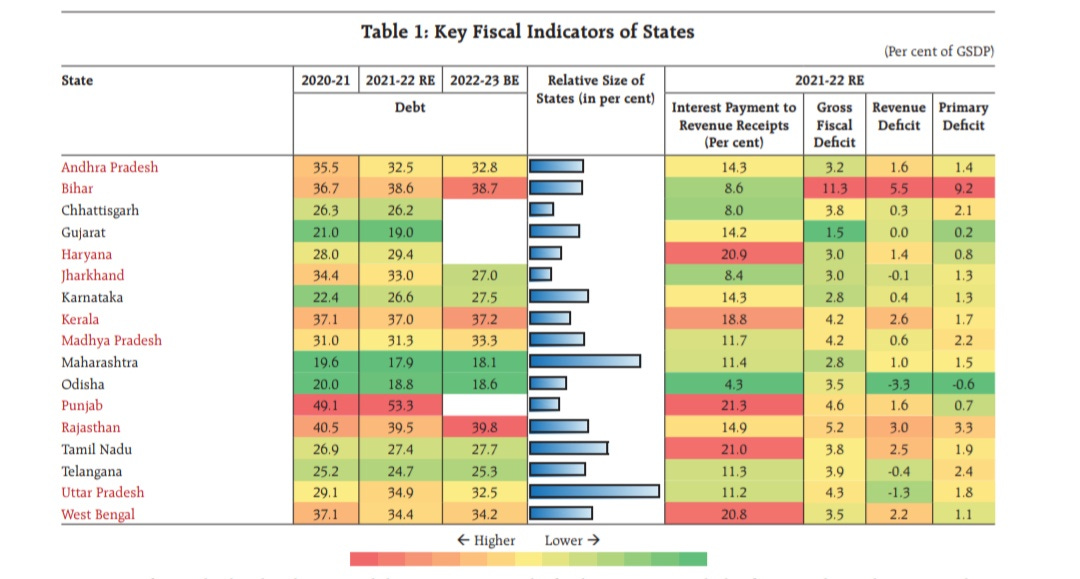

During 2011-2019, the states’ average gross fiscal deficit (the gap between the states' revenue and their expenditure) to gross state domestic product ratio (the total volume of all finished goods and services produced by a state in a particular period) was around 2.5%.

This was comfortably below the set risk limit of 3%.

However, things have changed since. Yes, once again, pandemic is the trigger event that has upset this ratio for many many states.

It not only reduced the states’ revenue but also increased the cost of their welfare schemes.

What’s more, many of these states already had a lot of freebie schemes going on. Schemes that offer subsidised electricity and water, farm loan waivers, and pensions.

Now, to you and I, this sounds great because who doesn’t like free stuff.

But this often comes at a heavy cost for the governments.

Like 35% of Telengana’s revenue receipts go towards these schemes.

And for other states this amount ranges from 5%-19% of the revenue.

To fund these policies, states have to borrow an extraordinary amount of money, which has raised their debts.

For instance, Punjab alone has a debt of Rs. 2.63 lakh crores.

And the state governments' expenditure on subsidies has grown by 12.9% and 11.2% in 2020-21 and 2021-22 respectively.

Now, the catch is that these states have a net borrowing ceiling: meaning they cannot borrow an endless amount of money.

The ceiling is fixed at Rs. 8.57 lakh crores or 3.5% of the GDP for 2022-2023.

But some states are mortgaging state assets like municipal parks, courts and so on to secure more loans.

States like Andhra Pradesh, Uttar Pradesh, Punjab, Himachal Pradesh, and Madhya Pradesh have raised up to Rs. 47,316 crores this way.

This could be dangerous, especially as most states already have a lot of financial risks.

💸 ‘Outstanding’ Financial Risks

Many of these states have a high amount of outstanding guarantees.

What’s that, you ask?

You see, often state public sector enterprises that aren’t doing that well need loans.

But precisely because they aren’t doing well, they don’t get loans.

In such cases, the government vouches for these enterprises.

But just a verbal guarantee isn’t enough. So, these governments have to guarantee that they will pay back the loan in case enterprises aren’t able to.

Now, some states have given lots of such guarantees, which is a risky move. If too many companies default, the state will have a heavy burden to bear.

Furthermore, these states give away free or subsidised electricity which helps the public a lot.

But this means power distribution companies or discoms don’t have enough money to pay companies and plants that generate power.

Currently, these discoms have dues worth Rs. 1.2 trillion and if they are eventually unable to pay them off, state governments will have to bail them out.

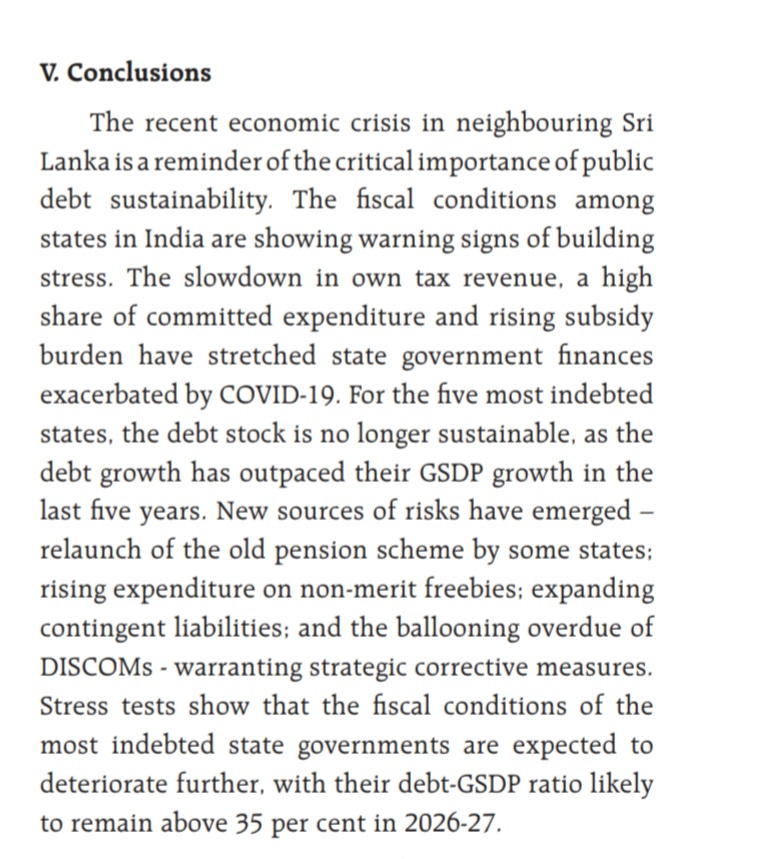

While some states will be able to bear this cost, it may drown out the 5 most indebted states: Punjab, Rajasthan, Kerala, Bihar, and West Bengal.

Especially because these states’ revenue has been growing very slowly.

Instead of investing their revenue in infrastructure and creating other assets, a move that would generate more money, they have been using this money to fund the freebie schemes that do not help generate revenue.

Wondering what happens when a state doesn’t have enough money to pay off debts?

Either the states will have to borrow more money from the RBI, potentially entering a debt trap, or the central government will have to rescue the state government.

Both these means are a drain on the country’s resources and will increase our overall fiscal deficit.

So, what’s the solution?

The Solution to the States’ Problems

According to the RBI and the SBI, the debts of Punjab, Rajasthan, Kerala, Bihar, and West Bengal, and their freebie schemes aren’t sustainable.

And some other states are also in trouble.

This can be fixed by either establishing a council that will oversee and evaluate the financial condition and debt of the states.

Or, the government could introduce tax-benefit models for states, which would give them an incentive to reduce debt and fiscal deficit.

Furthermore, states themselves need to realise that a lot of freebie schemes are unsustainable at the moment. They need to focus on building infrastructure, developing new revenue streams and all round development before they can introduce such welfare schemes.

However, with inflation rising right now, we wonder what the impact on the common man would be if these schemes were to stop.

⚡ In a line: The state governments are on the brink of major trouble as their debt and fiscal deficit is getting unsustainable, thanks to their freebie schemes.

💡 Quick question: Do you think ending the various freebie schemes will be a good idea?

Share this with your friends via WhatsApp or Twitter to help them declutter news from noise! See you tomorrow :)

You can also listen to our stories. Catch it on Spotify, Apple Podcast, Amazon Music, Google Podcasts, Gaana or Jio Saavn.

If you are coming here for the very first time: Don’t forget to join us on WhatsApp to get daily updates! 👇